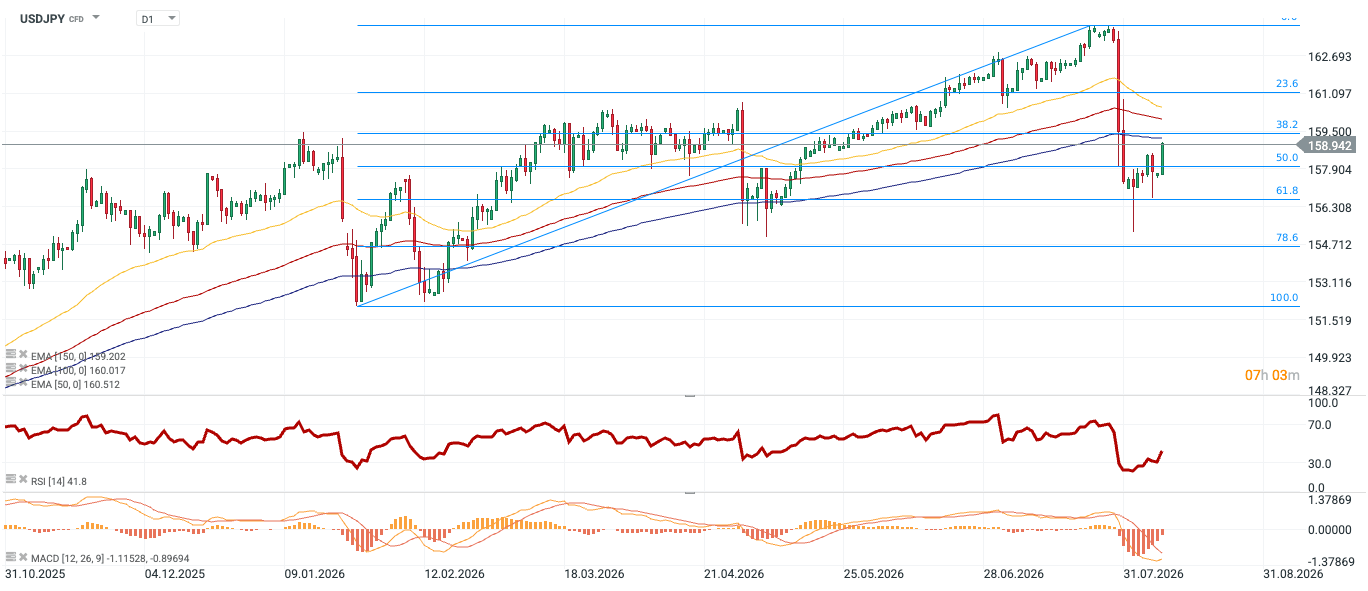

Following a record intervention by the Japanese Ministry of Finance and the US Department of the Treasury, the yen strengthened by over 5%, recovering losses incurred over the last 5 months, since the outbreak of the war in Iran. After reaching a local low below the 156 level, the USDJPY pair has returned to growth.

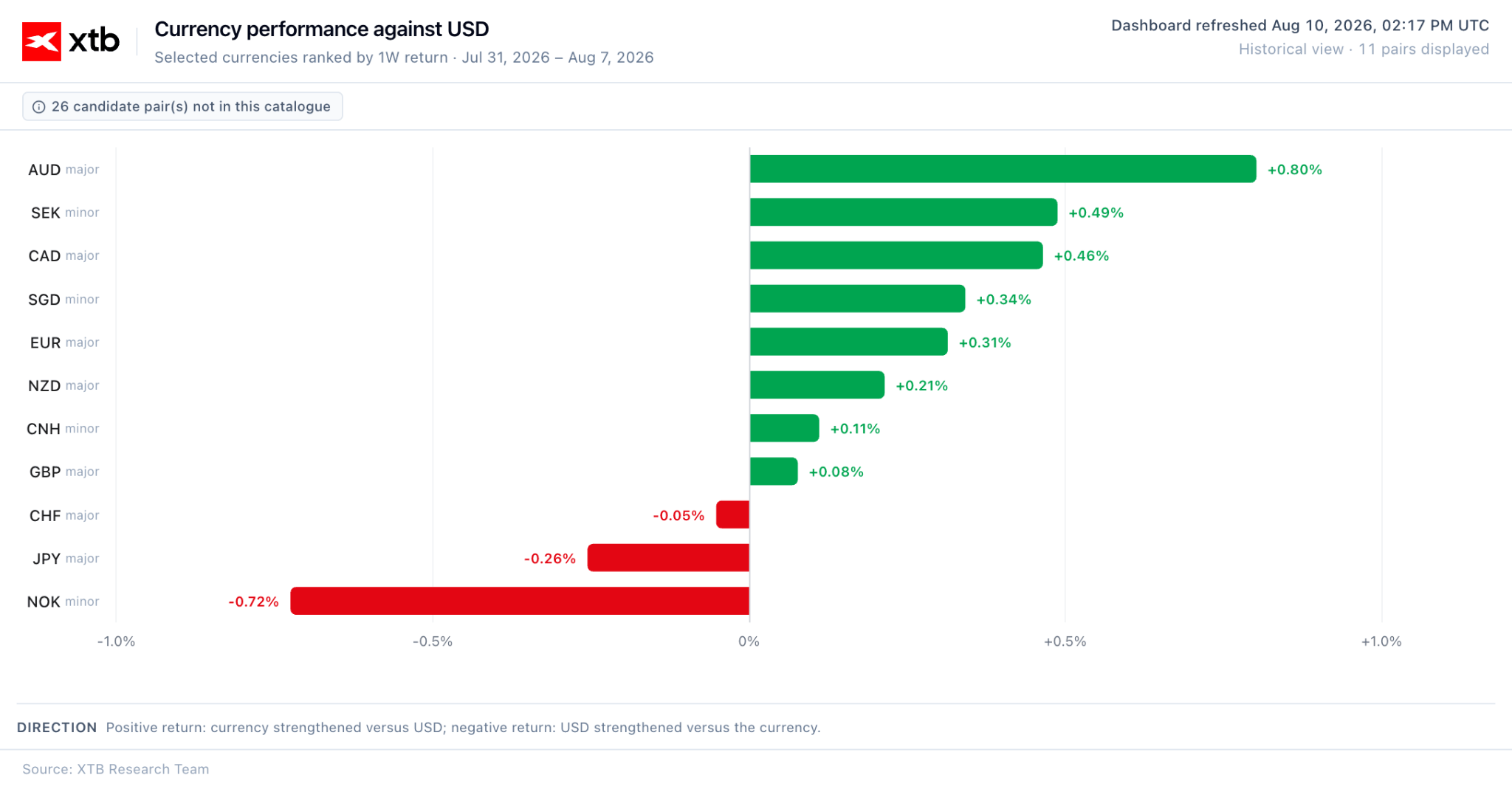

Figure 1: Weekly Performance of Selected Currencies [vs. USD] (31.07 – 07.08)

Source: XTB Research, 10.08.2026

Japanese Yen (JPY)

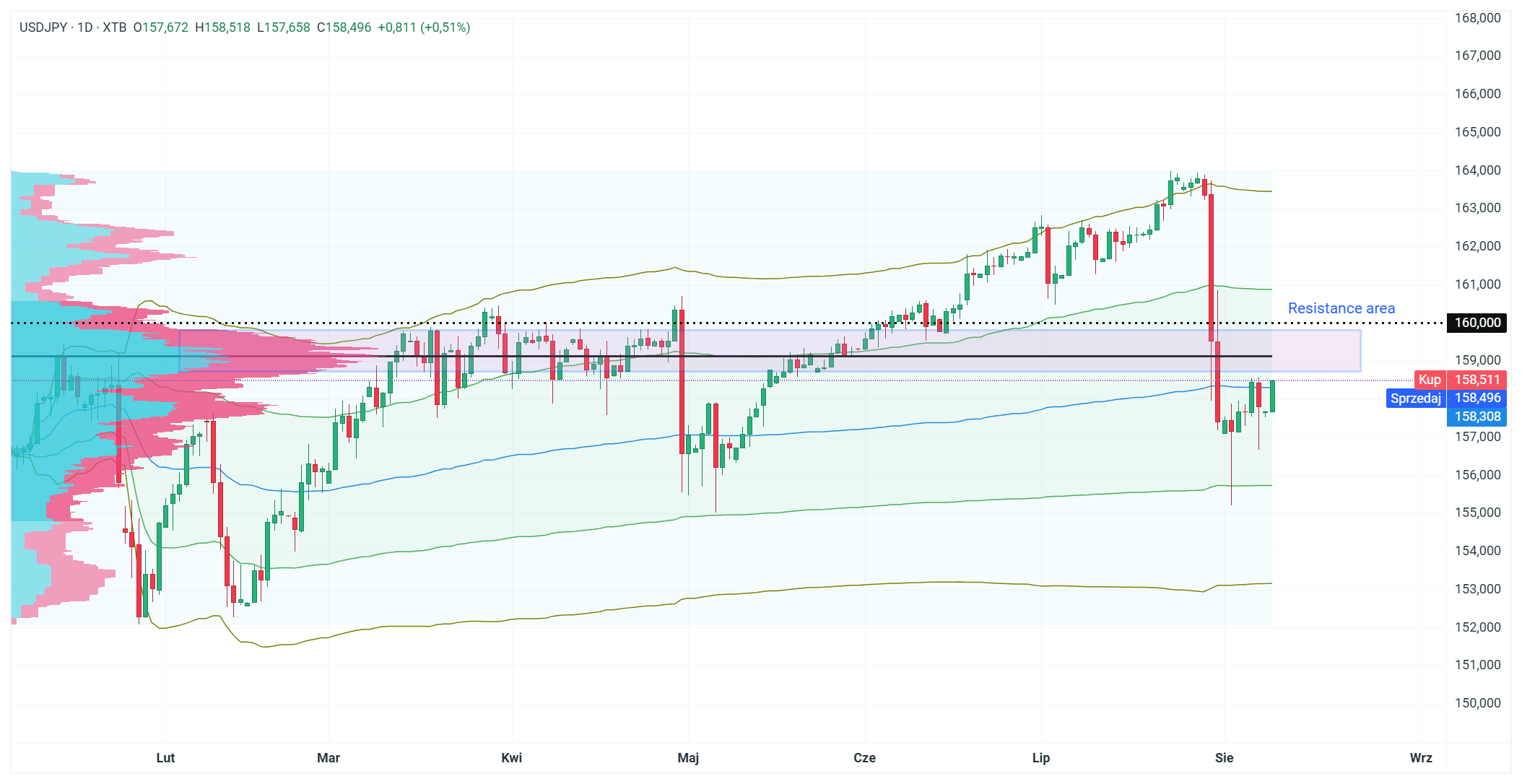

The fundamentals have not changed significantly and continue to exert pressure on the Japanese currency. The key issue remains the carry trade, or trading on the interest rate differential. As long as the discrepancy between the projected interest rate levels in the United States and Japan remains significant, even interventions amounting to nearly 90 billion dollars may prove insufficient to permanently reverse the trend. Figure 2: USDJPY (31.10.2025 – 10.08.2026)

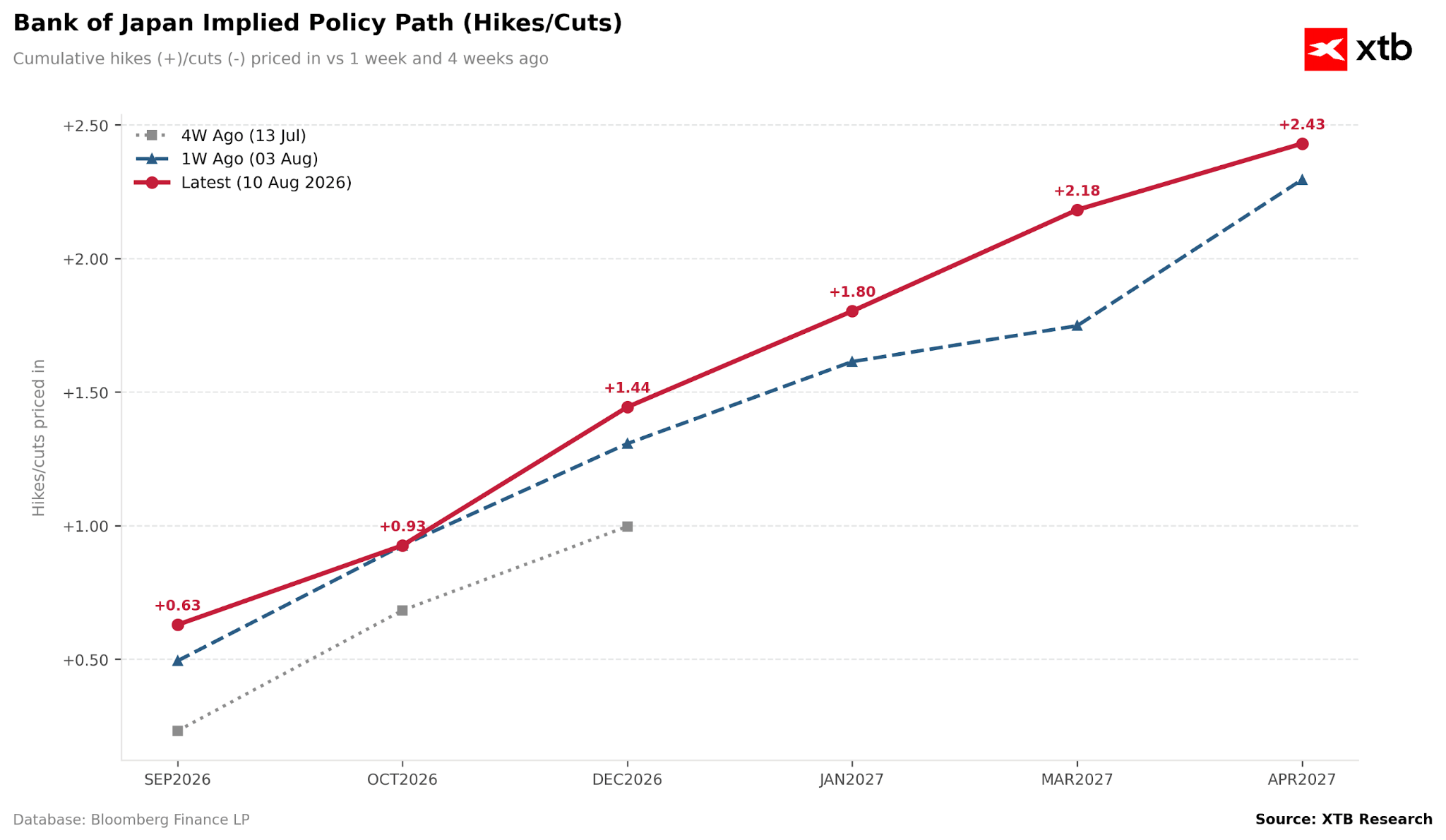

Source: xStation, 10.08.2026 Currently, the interest rate differential between both sides of the ocean stands at 2.675%. Market valuations suggest that it will narrow slightly in the coming months, reaching approximately 2.35% in July 2027. However, it seems that investors expect more decisive action from the Bank of Japan, with the next opportunity appearing only on 18 September. A decision to raise interest rates then could serve as a significant declaration for the market, leading to increased bets on subsequent hikes in the following months. Currently, such a move is priced at approximately 60%.

Figure 3: Bank of Japan Implied Policy Path (Hikes/Cuts) (2026-2027)

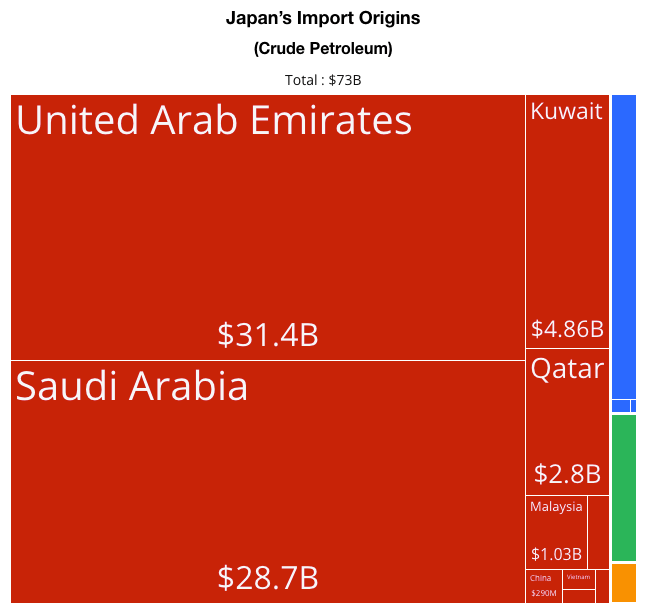

Source: XTB Research, 10.08.2026 In the meantime, the market’s attention will focus on the United States and the developing situation in the Middle East. Japan is almost entirely dependent on imports for its energy needs, and under standard conditions, nearly 90% of its crude oil comes from the Middle East. Figure 4: Japan’s Crude Oil Import Structure (2024)

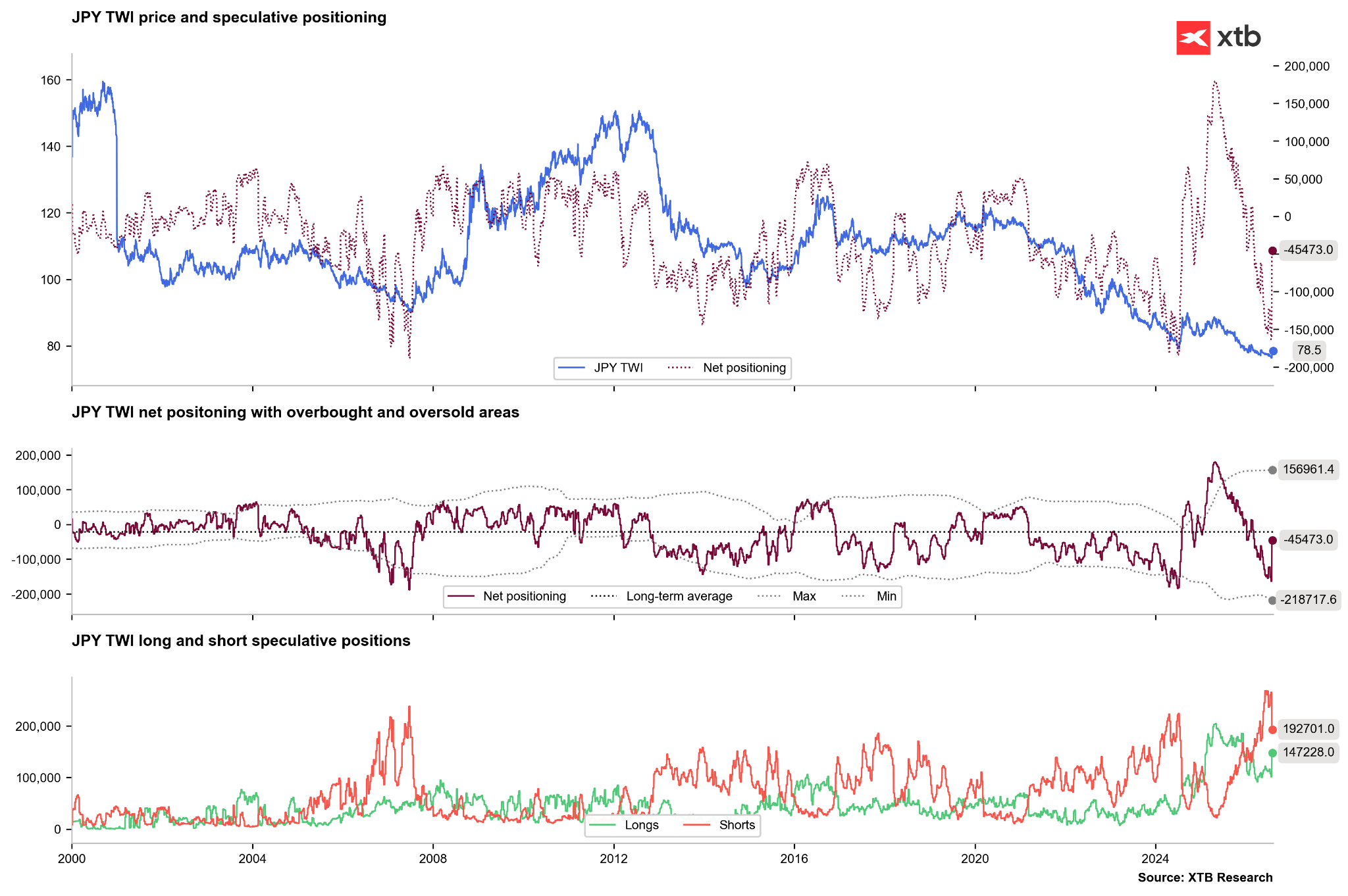

Source: OEC, 10.08.2026 However, further interventions cannot be ruled out, which the markets seem to fear. Positioning on the yen has changed significantly after many investors withdrew speculative short positions for fear of further actions aimed at defending the exchange rate. Figure 5: Yen Positioning (2000 – 2026)

Source: XTB Research, 10.08.2026

US Dollar (USD)

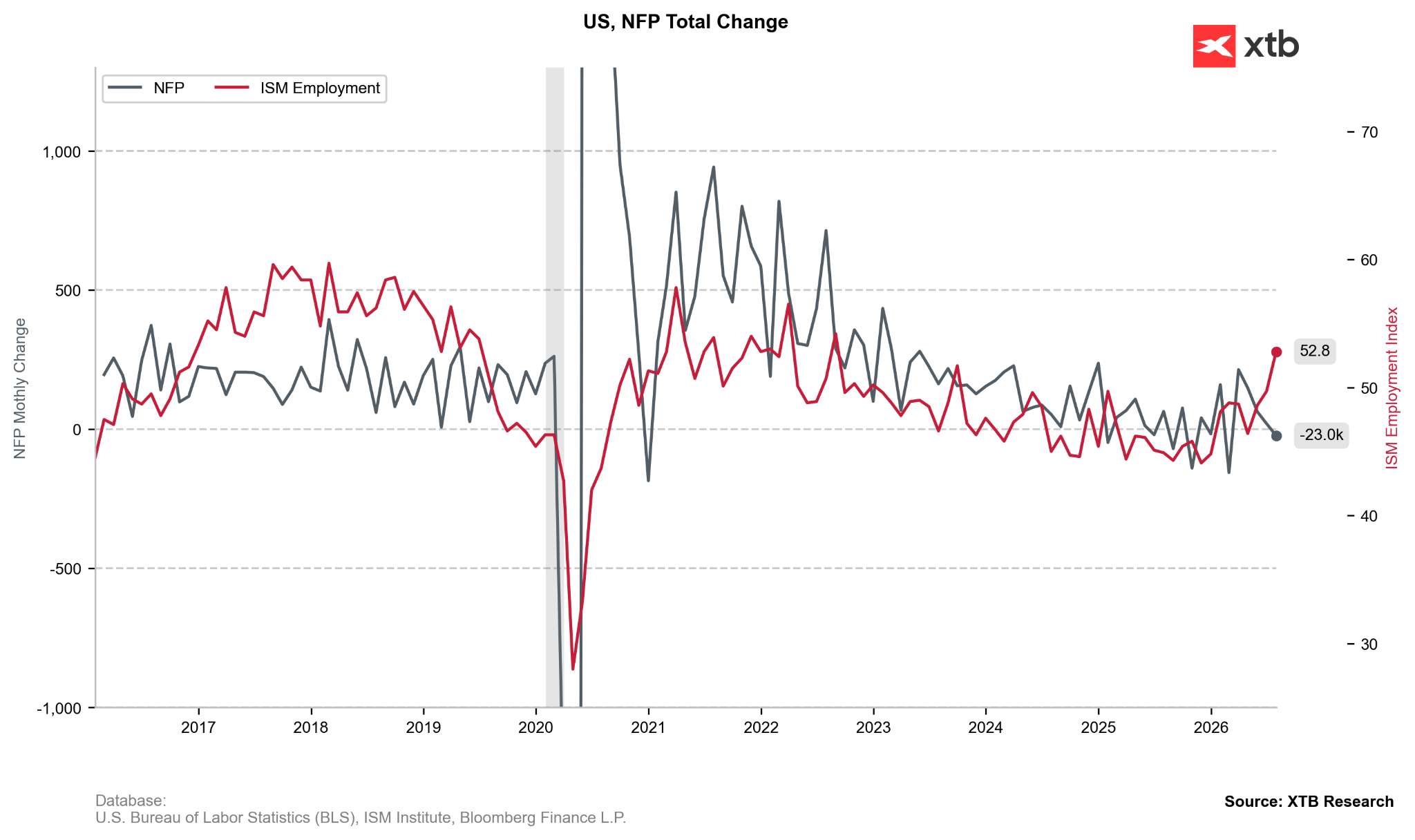

The July NFP report has been published. The number of new jobs in the US economy fell by 23 thousand, missing expectations by 5 standard deviations. Although extreme phenomena occur much more frequently in the world of macroeconomics (the so-called fat tails), assuming the data follows a normal distribution, we would have to wait 290,000 years for another such reading. Figure 6: NFP and Employment Component in ISM PMI (2016 – 2026)

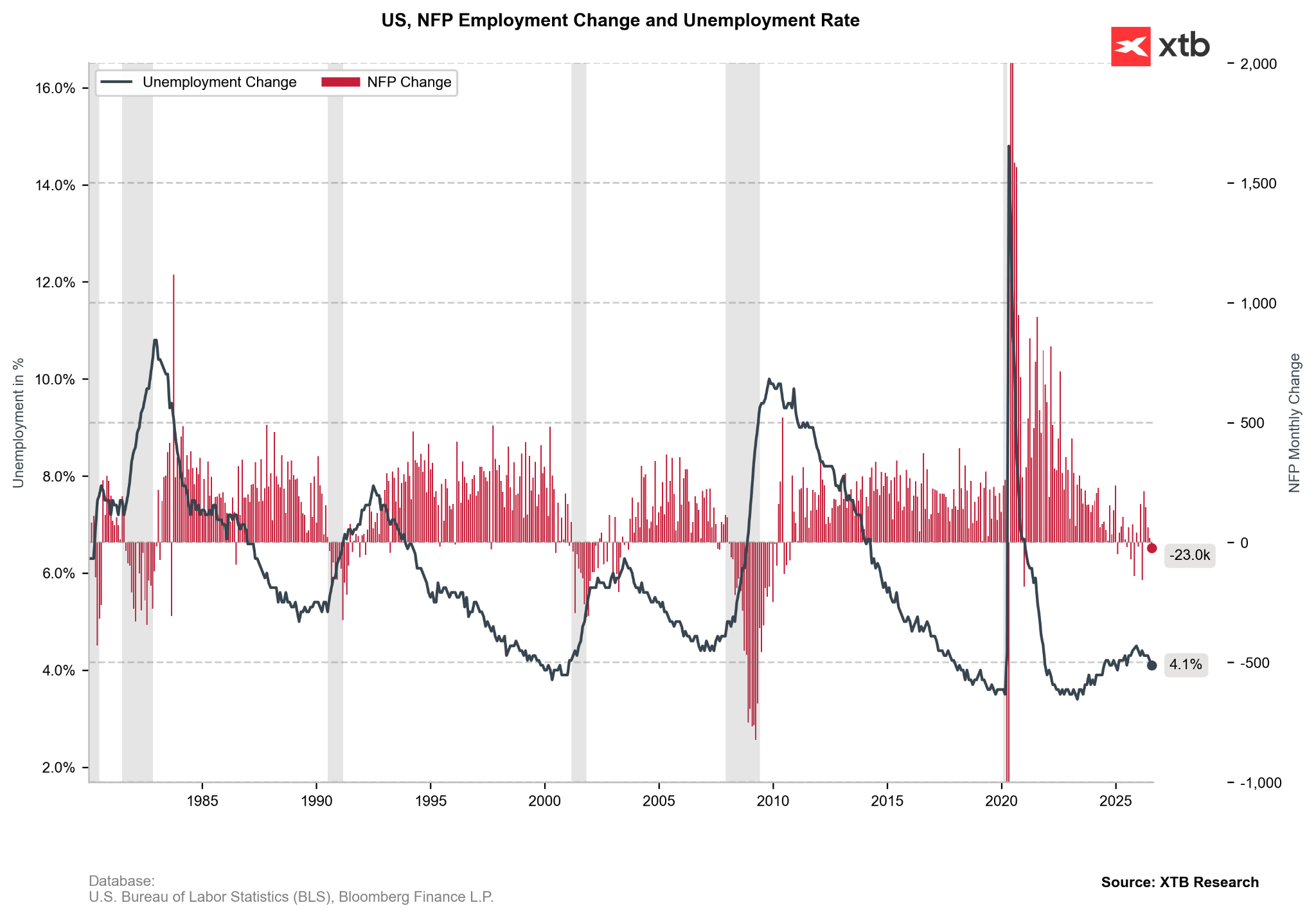

Source: XTB Research, 10.08.2026 The market reaction was certainly noticeable, though not as strong as many might have expected. The dollar’s losses were limited by, among other things, a decline in the unemployment rate (to 4.1%) and problems with seasonal adjustment of the data (the decline resulted mainly from a lower number of jobs in the public education sector). Figure 7: NFP and Unemployment Rate (1980 – 2026)

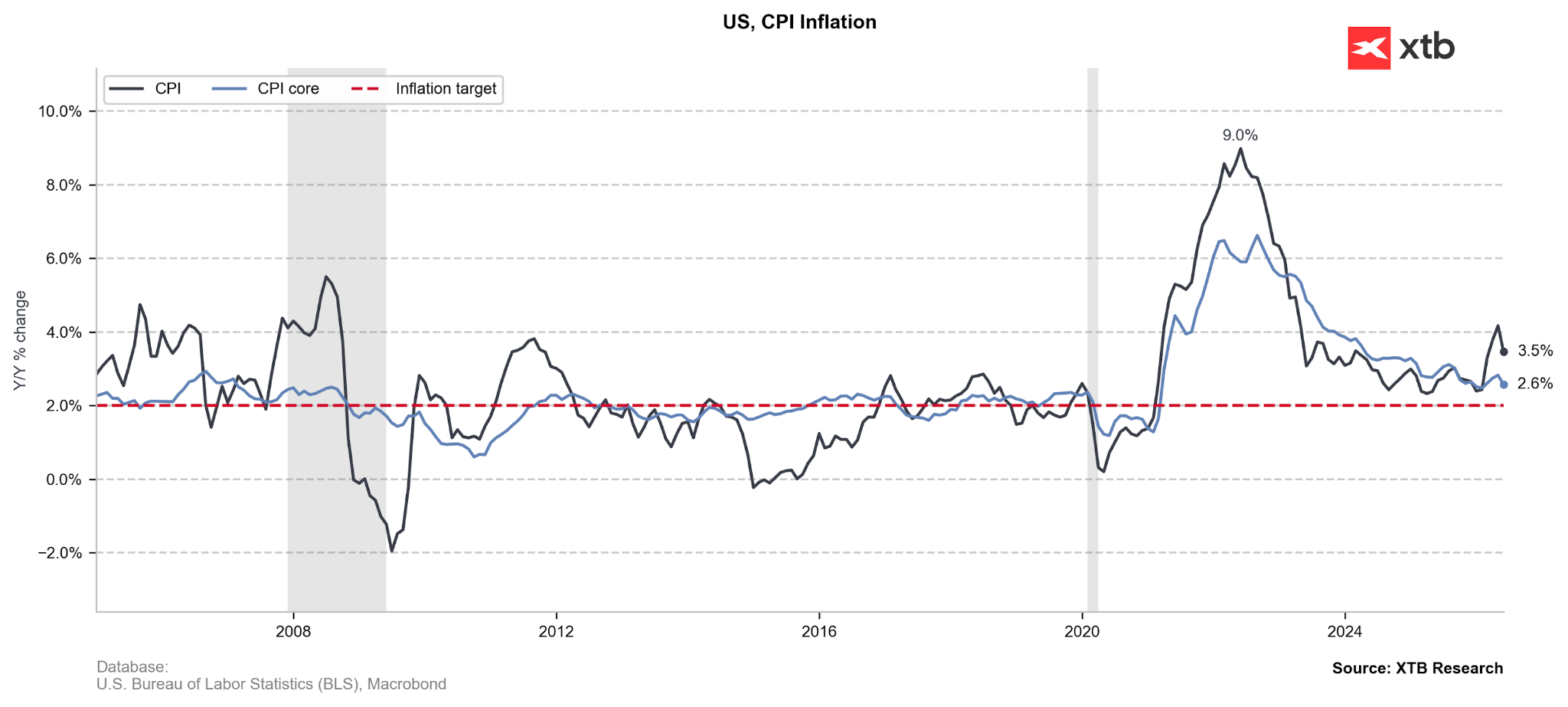

Source: XTB Research, 10.08.2026 It is worth noting, however, that higher energy prices have affected companies in the retail, leisure, and hospitality sectors (this despite the World Cup ending in July). Investors are currently unsure which direction the Fed will take in September; looking at market valuations, the chances of a hike can be compared to a coin toss. All eyes are on the July inflation reading scheduled for Wednesday. If, despite rising oil and gas prices, it shows similar values to June, we expect the committee led by Kevin Warsh to refrain from a hike until the next meeting. Figure 8: US CPI Inflation (2004 – 2026)

Source: XTB Research, 10.08.2026 For Warsh himself, this would be an exceptionally comfortable situation. In the event of intensifying inflation concerns, the committee would be almost forced to raise rates, especially in the face of revived discussions regarding the Fed’s independence. The topic returned to the table after further threats from Donald Trump directed at Lisa Cook, one of the FOMC decision-makers. These appeared more than a month after the Supreme Court deemed the president’s recent actions in this area unlawful.