Forecasting the upcoming week: US CPI and Warsh testimony to test the Dollar’s recovery

The upcoming week will bring a major test for the US Dollar (USD), with investors focusing on the United States Consumer Price Index (CPI), Federal Reserve (Fed) Chair Kevin Warsh’s congressional testimony and a broad set of activity indicators. China’s second-quarter Gross Domestic Product (GDP) and the Bank of Canada’s (BoC) interest-rate decision will also attract significant attention.

The US Dollar Index (DXY) trades near 101.00, recovering from a one-week low hit earlier on Friday as investors balance softer recent labor market data against renewed geopolitical uncertainty and persistent inflation concerns. Tuesday’s US CPI report will be the central event for the Greenback.

Headline CPI is expected to decline 0.1% MoM in June, following a 0.5% increase in May, while annual inflation previously stood at 4.2%. Core CPI is forecast to rise 0.3% MoM, up from 0.2%, while the annual core rate is expected to remain unchanged at 2.9%.

On another note, Fed Chair Warsh will testify on Tuesday and Wednesday, giving markets an opportunity to assess how policymakers balance elevated inflation against signs of weaker hiring. Comments from several Fed officials and the release of the Beige Book will provide additional guidance.

US Dollar Price Today

The table below shows the percentage change of US Dollar (USD) against listed major currencies today. US Dollar was the strongest against the Swiss Franc.

| USD | EUR | GBP | JPY | CAD | AUD | NZD | CHF | |

|---|---|---|---|---|---|---|---|---|

| USD | 0.12% | 0.07% | -0.42% | -0.08% | -0.17% | -0.14% | 0.21% | |

| EUR | -0.12% | -0.05% | -0.54% | -0.19% | -0.30% | -0.27% | 0.09% | |

| GBP | -0.07% | 0.05% | -0.50% | -0.13% | -0.25% | -0.23% | 0.13% | |

| JPY | 0.42% | 0.54% | 0.50% | 0.34% | 0.25% | 0.25% | 0.60% | |

| CAD | 0.08% | 0.19% | 0.13% | -0.34% | -0.10% | -0.08% | 0.27% | |

| AUD | 0.17% | 0.30% | 0.25% | -0.25% | 0.10% | 0.02% | 0.35% | |

| NZD | 0.14% | 0.27% | 0.23% | -0.25% | 0.08% | -0.02% | 0.34% | |

| CHF | -0.21% | -0.09% | -0.13% | -0.60% | -0.27% | -0.35% | -0.34% |

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the US Dollar from the left column and move along the horizontal line to the Japanese Yen, the percentage change displayed in the box will represent USD (base)/JPY (quote).

EUR/USD trades lower near 1.1420, retreating as the US Dollar recovers from its weekly low, and is set to finish the week with a 0.19% loss. The pair will remain highly sensitive to US CPI and Warsh’s testimony, while the European calendar includes industrial production and final inflation figures.

GBP/USD trades near 1.3400, with a weekly gain of around 0.34% after reaching a three-week high. The Pound Sterling (GBP) faces an important domestic calendar, with United Kingdom (UK) GDP, industrial production, and manufacturing output due on Thursday. UK GDP is expected to grow 0.1% MoM in May, following a 0.1% contraction. Industrial production is forecast to rise 0.1%, while manufacturing production is expected to decline 0.1% after increasing 0.4% previously.

USD/JPY trades lower near 161.70 on Friday but is set to close the week with a 0.24% gain. The pair will remain driven by US Treasury yields, Fed expectations, and concerns over possible intervention by Japanese authorities. A hotter-than-expected US CPI report could lift yields and revive upward pressure on USD/JPY. Softer inflation could extend the pair’s decline and offer further support to the Japanese Yen.

AUD/USD trades slightly higher near 0.6950, supported by a softer broader US Dollar backdrop and recent strength in the Chinese Yuan. However, the Aussie’s direction next week will depend heavily on Chinese economic data and US inflation. Wednesday’s Chinese GDP report is expected to show the economy expanding 4.4% YoY in the second quarter, slowing from 5%. Quarterly growth is forecast at 0.9%. Industrial production is expected to rise 4.7%, while retail sales are projected to decline 0.1% YoY.

USD/CAD trades lower near 1.4150 ahead of Wednesday’s Bank of Canada policy decision. The BoC is expected to leave its benchmark rate unchanged at 2.25%. The accompanying Monetary Policy Report, policy statement and press conference will be closely examined for guidance on inflation, domestic demand and future rate moves. A hawkish message could extend USD/CAD’s decline, while a cautious stance may limit the Canadian Dollar’s strength.

West Texas Intermediate (WTI) Oil trades muted near $71.60 per barrel as investors assess the risk of renewed supply disruptions linked to tensions between the United States and Iran. Oil prices could become more volatile if diplomatic efforts deteriorate further or concerns surrounding Middle Eastern supply routes intensify. However, signs of weaker global demand, particularly from China, may limit gains.

Gold trades lower near $4,102, losing ground as the US Dollar recovers and investors prepare for the US inflation report. The precious metal remains supported by geopolitical uncertainty, although higher Treasury yields could create additional pressure.

Anticipating economic perspectives: Voices on the horizon

Monday, July 13:

- Fed’s Bowman

- Fed’s Waller

- ECB’s Schnabel

- BoE’s Pill

Tuesday, July 14:

- Fed’s Warsh

- Fed’s Barr

- Fed’s Goolsbee

- Fed’s Cook

- Fed’s Bowman

- BoE’s Bailey

Wednesday, July 15:

- Fed’s Williams

- Fed’s Chair Warsh

- ECB’s Nagel

- Fed’s Cook

- Fed’s Musalem

Thursday, July 16:

- Fed’s Logan

- Fed’s Schmid

- Fed’s Jefferson

Friday, July 17:

- ECB’s Cipollone

Central banks’ meetings and upcoming data releases to shape

The main monetary-policy event will be the Bank of Canada interest-rate decision on Wednesday, July 15. The central bank is expected to leave its policy rate unchanged at 2.25%.

The BoC will also publish its Monetary Policy Report and policy statement, followed by a press conference. No interest-rate decisions are scheduled from the Fed, ECB, BoE, BoJ, RBA or RBNZ.

Fed’s Kashkari says AI will force a rate hike; EURUSD and USD reverse early moves

s now losing buying momentum. In the second half of the session, the momentum has clearly shifted to the sellers. The US100, on the other hand, reflects relative strength—the index has gradually lost its downward momentum and is stabilizing in the second half of the day, ignoring some of the negative market signals.

The main topic of the day in the tech world is the potential delay of OpenAI’s IPO — reports in the NYT about the debut being pushed back to next year (in part due to SpaceX’s poor performance following its IPO) have hit the entire semiconductor sector hard. Micron, AMD, and Intel are down about 2% each, while Oracle is down more than 1%. The ripple effect was particularly evident in Asia: SoftBank, a key investor in OpenAI, plummeted by more than 12% , the Nikkei 225 lost 4.15% , and South Korea’s Kospi plunged by 5.81% .

JPMorgan warns outright that the IPO delay “could slow the pace of spending on AI infrastructure.” On the other hand, however, postponing the launch date will keep market expectations alive, which, paradoxically, could have a positive effect on market returns given the narrative being built and the promises of increasingly advanced AI development.

The main risk factor on the geopolitical front, however, is the U.S.-Iran situation. Trump reported on Truth Social that Iran had launched at least four kamikaze drones at ships in the Strait of Hormuz. One struck the deck of a large container ship—the vessel sustained damage but continued its voyage. The other three drones were shot down. Trump called the incident a “stupid violation of the ceasefire agreement.” The Strait of Hormuz is a key route for about 20% of global oil supplies—any escalation in this region immediately catches the attention of commodity markets.

At the same time, Fed’s Kashkari spoke out on inflation—according to him, the labor market is not currently a source of inflation. Price pressures are being driven by the supply side, and one of the factors he mentioned is… the expansion of AI infrastructure. Kashkari of the Fed said that the development of artificial intelligence likely means the Fed will have to raise interest rates.

Source: xStation

Intraday USD correction, but UBS sees the greenback regaining a new trend — what’s next for EUR/USD?

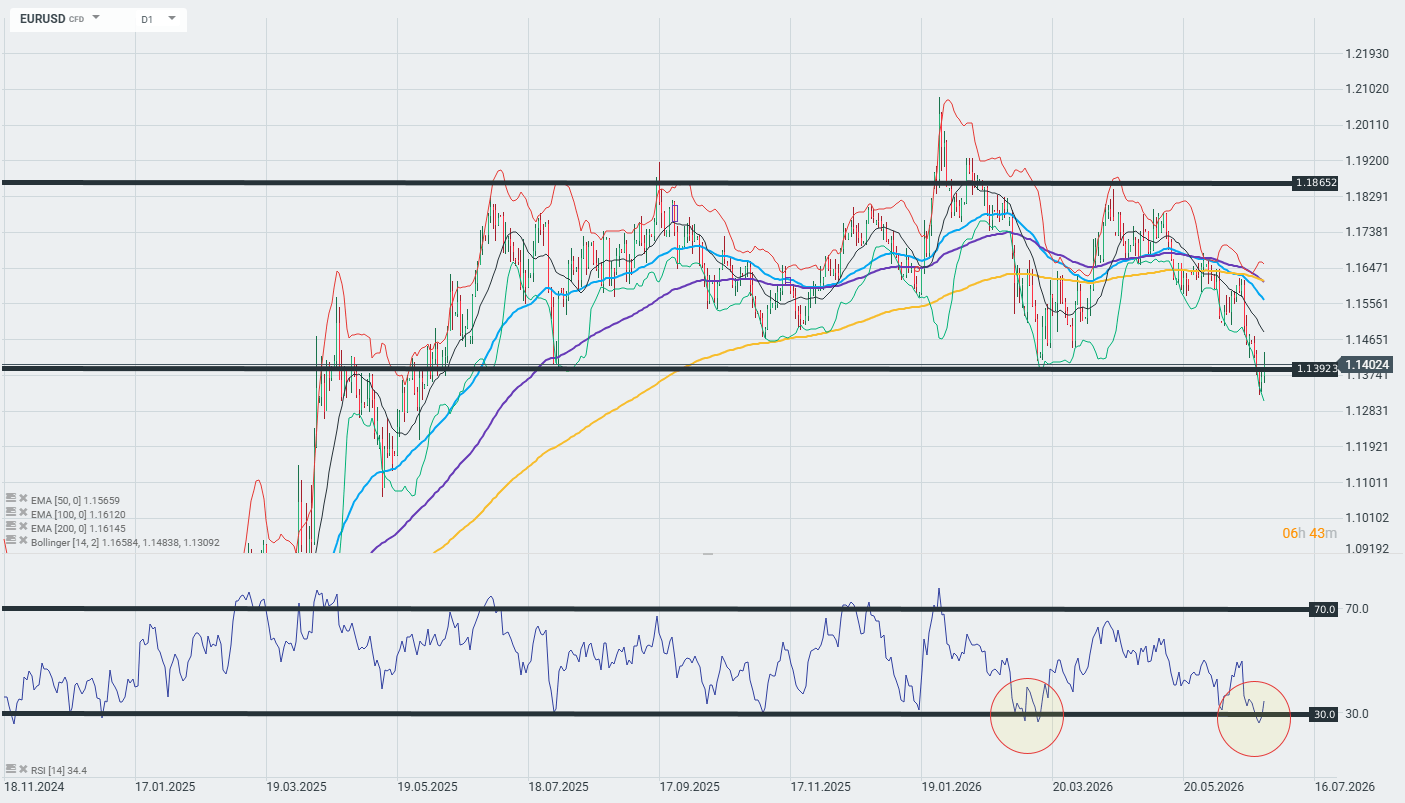

hursday’s and Friday’s trading sessions saw a sharp rebound in the EUR/USD pair, which is now attempting to consolidate above 1.14 after a series of strong bullish daily candles in recent weeks pushed the dollar to levels not seen since May 2025. Meanwhile, UBS analysts take the opposite view—arguing that the current weakness of the USD is a temporary phenomenon, not a structural one.

UBS vs. the Market — A Discrepancy in Narratives

UBS lowered its forecast for the EUR/USD exchange rate at the end of 2026 to 1.12 from the previous 1.14 , signaling that the bank expects the current trend to reverse. This view is based on a reassessment of U.S. interest rate expectations—the market is beginning to price in the possibility that the Fed may maintain a restrictive monetary policy for longer than previously anticipated. UBS notes that the DXY index has the potential to test the 102 level, which was last seen in May 2025. Although long positions in the dollar have increased, the bank assesses that they are far from the extreme levels seen in 2024—which means there is still room for further USD buying.

Fed vs. ECB — The Divergence Persists

The key driver for the EUR/USD pair remains the divergence in monetary policy on both sides of the Atlantic.

The Fed —despite some market expectations of rate cuts—maintains a hawkish stance, emphasizing the resilience of the U.S. economy and labor market.

The ECB , in turn, is continuing its easing cycle, and further rate cuts are almost fully priced in by the market for the second half of the year. This asymmetry naturally favors the dollar over the euro in the medium term. Today’s rebound in EUR/USD can therefore be interpreted as a technical correction following an extremely rapid move, rather than a change in the pair’s fundamental outlook.

Technical Context and Carry Trade

It is worth noting that, in the same analysis, UBS points to the Swiss franc as a currency that may weaken in the short term due to its growing role as a carry trade funding currency—which indirectly supports risk appetite and may temporarily curb the dollar’s strength. The Australian dollar’s target was lowered to 0.68 from 0.74 , reflecting the global context: weaker macroeconomic data outside the U.S. and narrowing interest rate differentials are boosting the greenback against commodity and emerging-market currencies.

Technical Analysis: EURUSD D1

The pair is currently testing a key level at 1.1392—a break below or above this level could determine the pair’s trajectory for the coming sessions. On the upside, resistance comes from the 50/100/200 EMAs clustered around 1.1560–1.1615. The RSI, at 34.4, is approaching the oversold zone (30)—similar to February 2026—which could trigger a short-term technical rebound. Nevertheless, as long as the pair does not close the day clearly above 1.1392, technical analysis favors a continuation of the downtrend. It is worth noting, however, that the pair has been highly volatile in recent days, so price movements may remain chaotic in the near term.

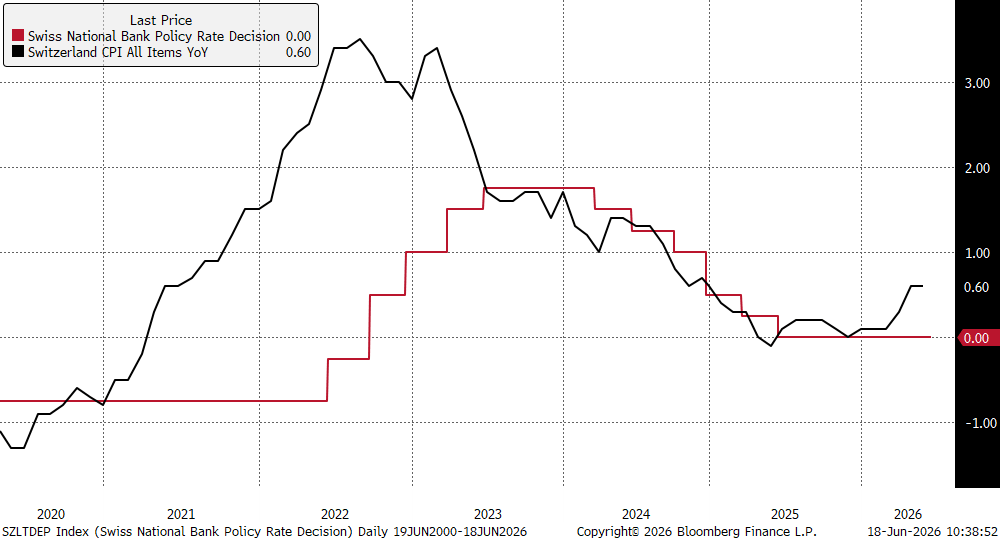

Swiss franc weakens after SNB keeps rates unchanged

The Swiss National Bank (SNB) decided to keep its main interest rate unchanged during its June meeting. The interest rate has remained unchanged exactly since June last year. It is worth emphasizing that interest rate decisions in Switzerland are made quarterly. The interest rate remains at 0% and currently, due to slightly elevated inflation, we should not expect any pressure for cuts, but at the same time, it is still far from the upper limit of the inflation target.

Despite the fact that the war in Iran caused a temporary increase in imported energy prices and pushed the May inflation reading to 0.6%, the Swiss CPI index still sits comfortably in the lower range of the 0-2% inflation target. Switzerland shows significantly less dependence on energy commodities from the Middle East thanks to developed hydropower and nuclear energy, which protects the local economy from global price shocks more strongly than the Eurozone. The main focus for policymakers remains the exchange rate of the Swiss franc and the risk of its excessive appreciation in the face of geopolitical uncertainty.

Macroeconomic forecasts The SNB made a slight upward revision to its inflation forecasts in the short and medium term:

- Inflation: The Bank now forecasts average inflation at 0.6% in 2026 (up from 0.5% in the March forecast) and 0.6% in 2027 (also up from 0.5%). In 2028, inflation is expected to be 0.7% (compared to 0.6% previously), and a reading of 0.8% is expected in the first quarter of 2029.

- GDP Growth: Economic forecasts remained unchanged. The SNB expects the Swiss economy to grow by about 1.0% in 2026 and 1.5% in 2027.

Statements from bankers at the SNB conference

Key members of the SNB Governing Board sent clear signals during today’s conference:

- Martin Schlegel (Chairman of the SNB):”If necessary, we show an increased readiness to intervene in the foreign exchange market. In this way, we counteract a rapid and excessive strengthening of the Swiss franc, which would threaten price stability in Switzerland”.”Inflation has risen in recent months as a result of higher energy prices. However, medium-term inflationary pressure is virtually unchanged compared to the last monetary policy assessment”.”Everything between 0 and 2% is fine regarding inflation” and “no preference as to where in the range inflation is located”.He also indicated that monetary conditions are weaker than in March, and the bank does not currently see second-round effects in Switzerland.

- “If necessary, we show an increased readiness to intervene in the foreign exchange market. In this way, we counteract a rapid and excessive strengthening of the Swiss franc, which would threaten price stability in Switzerland”.

- “Inflation has risen in recent months as a result of higher energy prices. However, medium-term inflationary pressure is virtually unchanged compared to the last monetary policy assessment”.

- “Everything between 0 and 2% is fine regarding inflation” and “no preference as to where in the range inflation is located”.

- He also indicated that monetary conditions are weaker than in March, and the bank does not currently see second-round effects in Switzerland.

- Antoine Martin (Member of the SNB Governing Board):He pointed out that the situation in the Middle East remains fragile, adding that global inflation should be expected to remain at an elevated level.

- He pointed out that the situation in the Middle East remains fragile, adding that global inflation should be expected to remain at an elevated level.

- Attilio Tschudin (Member of the SNB Governing Board):He noted that domestic indicators show a solid economic recovery, but the main risk for Swiss prospects is the condition of the global economy.

- He noted that domestic indicators show a solid economic recovery, but the main risk for Swiss prospects is the condition of the global economy.

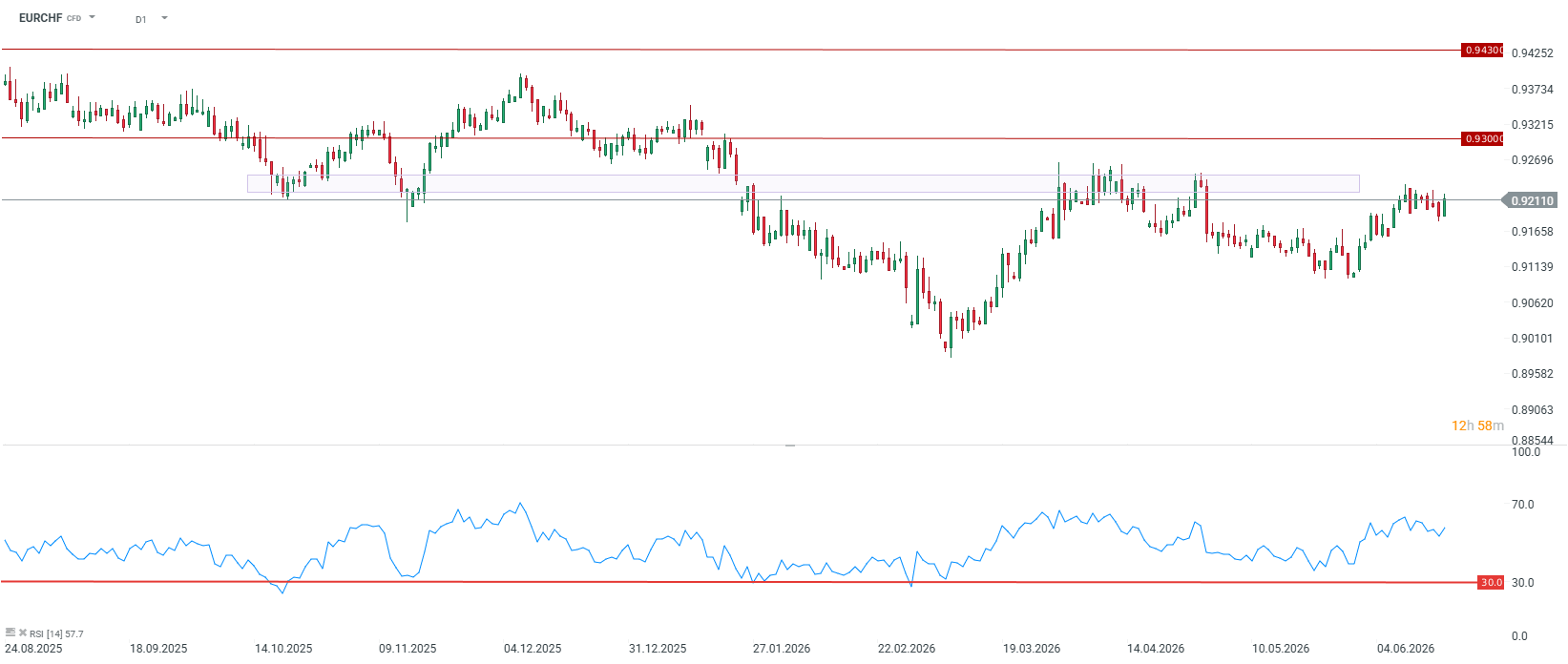

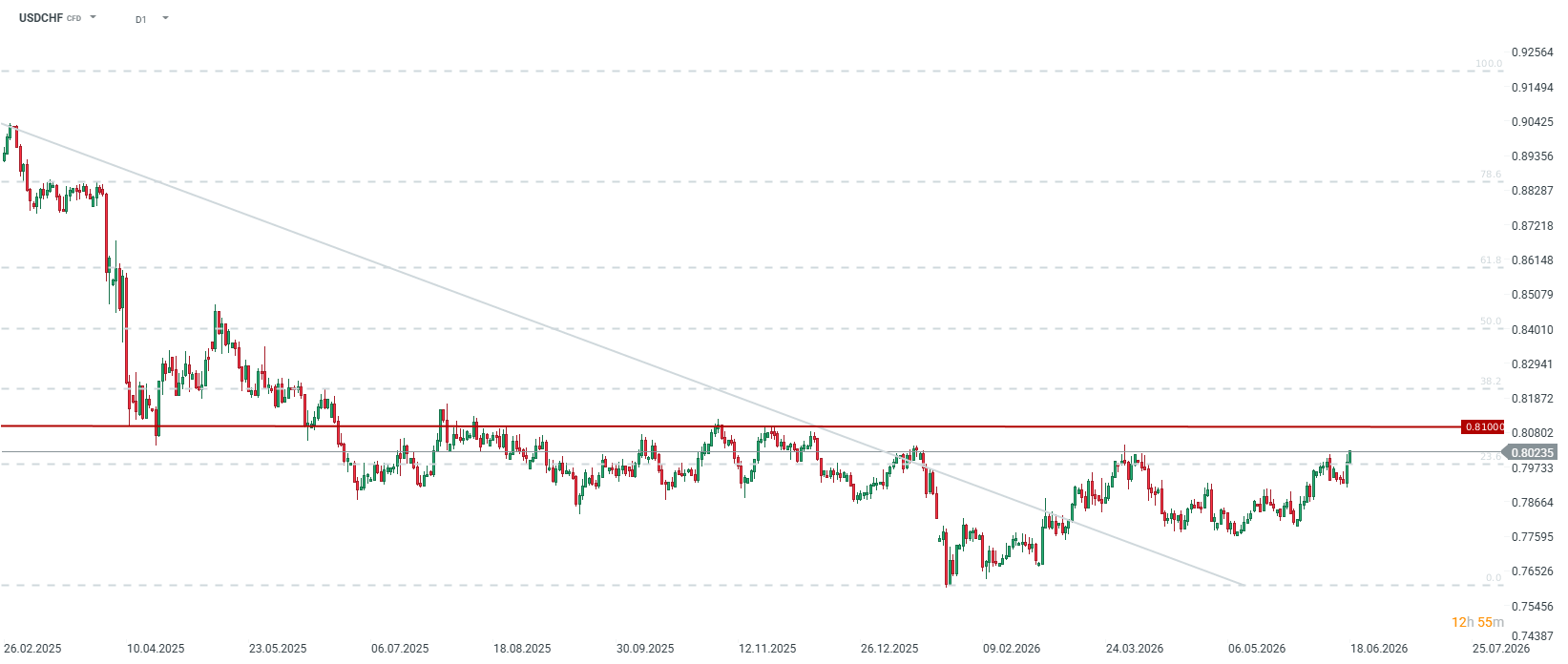

What to expect for EURCHF and USDCHF? EURCHF

Immediately after the decision was announced, the franc weakened slightly against the euro, falling by 0.2%-0.3% to a level of around 0.9215 per euro. Since the sudden strengthening of the franc at the turn of February and March (outbreak of war in Iran), clear communication from the SNB about its readiness to intervene has systematically pushed the CHF rate down. A strong supply zone for the pair is around 0.9220 to 0.9250.

USDCHF

Wednesday’s signing of a peace agreement in Versailles between the US and Iran by President Trump and the Iranian President is a strong factor mitigating tensions in energy commodity markets. This means a drop in demand for the franc as a “safe haven,” which should favor a rebound and stabilization of EURCHF and USDCHF rates. Nevertheless, due to Martin Schlegel’s declared “increased readiness to intervene” in the event of any turmoil, investors must take into account that the SNB is artificially limiting the franc’s potential for further strengthening. Any sudden attempts at CHF appreciation will likely be met with a decisive sell-off of the currency by the Swiss central bank, which sets a solid long-term floor for EURCHF and USDCHF quotes.

BoE: June hike seen as one and done – ING

ING’s James Smith notes that the Bank of England (BoE) kept rates at 3.75% in April but is moving closer to tightening as the Middle East crisis persists. ING now expects a single June rate hike, with UK inflation seen peaking slightly above 4% this year. ING remains sceptical about a persistent inflation surge.

ING shifts to a June hike call

“One month ago, Bank of England Governor Andrew Bailey told us markets were getting ahead of themselves on rate hike pricing. That feels like the underlying message from the April decision, which keeps interest rates at 3.75%. But it’s also clear the Bank is inching closer to a rate hike in June.”

“Governor Bailey characterised the decision not to cut, which is what the Bank was likely to have done pre-war, as in effect a decision to tighten policy.”

“That’s why, after today’s decision, we’re now edging towards a hike in June. It’s certainly not guaranteed, but that’s now narrowly our base case, having previously felt rates would stay on hold through this year.”

“Whether that’s followed by one or even two extra hikes, as markets are currently pricing, we’re less convinced right now. It’s clear the majority of the committee are still sceptical about this turning into a persistent bout of inflation, akin to what we saw in 2022. We strongly agree.”

Lagarde speaks on policy outlook after leaving key rates unchanged

Christine Lagarde, President of the European Central Bank (ECB), explains the ECB’s decision to leave key rates unchanged at the April policy meeting and responds to questions from the press.

ECB press conference key quotes

“Economy was showing momentum before current turbulence.”

“Domestic demand remains main driver of growth.”

“Outlook highly uncertain.”

“Incoming info suggests that conflict is weighing on activity.”

“Business less confident about future.”

“Supply chains coming under pressure.”

“High energy to weigh on incomes.”

“High energy costs to make firms, households reluctant to invest.”

“Labour demand has cooled further.”

“Households in solid financial position.”

“Favourable starting point provides some cushioning.”

“Fiscal responses should be temporary, targeted, tailored.”

“Indicators of underlying inflation have changed little in recent months.”

“Wage tracker indicates easing labour costs.”

“Surveys indicate rise in other costs.”

“Most measures of longer term inflation expectations stand around 2%.”

“Increase in energy prices will keep inflation well above 2% in near term.”

“Will closely monitor size and impact of energy price surge.”

“Risks to growth are tilted to the downside.”

“Worsening of global market sentiment could further dampen demand.”

“Risks to inflation are tilted to the upside.”

“Not going to say whether we’re closer to any particular scenario.”

“We are certainly moving away from baseline.”

“To where exactly? I’m not sure is the most relevant assessment.”

“Most critical is what impact energy prices will have.”

“Made an informed decision of yet insufficient info.”

“Debated at length various options.”

“Decision was unanimous.”

“Debated at length a hike.”

“Some governors may argue both sides of proposals.”

“Hard data is broadly in line with projections.”

“There is such uncertainty, we need to revisit all issues at next meeting.”

“Given position we’re at, six weeks will be the right time to assess developments.

BoE’s Bailey speaks on interest rate outlook, takes media questions

Bank of England (BoE) Governor Andrew Bailey is addressing a press conference and responding to media questions, explaining the reasons behind the central bank’s decision to hold the benchmark policy rate at 3.75% in an 8-1 vote split following the April monetary policy meeting.

Key takeaways from Bailey’s Press Conference

Monetary policy cannot prevent higher global energy prices from affecting uk economy and inflation.

Where we go from here will depend on size and duration of shock to energy prices.

We now project inflation will rise to a little over 3.5% by end of year.

Initial indirect effects of inflation are likely to be largest for food prices.

The longer the conflict in Middle East lasts, the worse the impact will become.

Size of second round effects is uncertain and will take time to build.

Monetary policy faces a difficult judgement call as cannot wait for conclusive evidence on 2nd round effects.

Under scenarios A and B, necessary interest rate response is largely achieved by not cutting rates as was expected in Feb and without further rate increase.

Prolonged spike in energy prices could lead to higher Bank Rate.

There is a good deal of space available to accommodate inflation pressures by not cutting rates as had been previously expected.

Sheer volatility of energy prices makes it impossible to put probabilities on different scenarios.

It would be a mistake to wait for second round effects before acting, that would be too late.

It will take time before we get a good read on pay as most annual settlements have already been agreed.

I think energy price profile of scenario B is more plausible than scenario A.

We do not hear that rapid return to pre-conflict energy supply conditions is likely

It is an active hold today, not a passive one.

Developing story, please refresh the page for updates.

This section below was published at 11:00 GMT to cover the Bank of England’s policy announcements and the initial market reaction.

The Bank of England (BoE) announced on Thursday that it left the benchmark policy rate unchanged at 3.75%, as widely expected, following the conclusion of the April monetary policy meeting.

The vote showed the expected split on the Monetary Policy Committee (MPC), with one member favoring a 25-basis point (bps) rate hike.

Takeaways from BoE Monetary Policy Summary

BoE Chief Economist Huw Pill voted to increase rates by 0.25 percentage points

Bailey says “reasonable” to hold rates at 3.75% given uk economic situation and uncertainty in Middle East.

CPI likely to be higher this year as effect of higher energy prices passes through.

Bailey says our job is to make sure that inflation gets back to 2% after initial impact of war on energy prices has passed.

BoE says there is a risk of material second-round effects from inflation on wage- and price-setting, policy would need to lean against this.

BoE says weaker economy and labour market and tighter financial conditions will help reduce inflation over time.

BoE Monetary Policy Report highlights

BoE has not updated central economic forecasts, gives new forecasts based on three scenarios for energy prices and inflation persistence.

BoE forecasts 2026 CPI averaging 3.3%-4.5% under different scenarios (Feb central projection: 2.2%).

BoE forecasts 2027 CPI averaging 2.6%-4.8% under different scenarios (Feb central projection: 1.9%).

BoE forecasts 2028 CPI averaging 1.5%-2.9% under different scenarios (Feb central projection: 2.0%).

BoE forecasts for 2027 GDP growth 0.8%-1.0% under different scenarios (Feb central projection 1.5%).

BoE forecasts for 2026 GDP growth 0.7%-0.8% under different scenarios (Feb central projection 0.9%).

BoE says most inflationary scenario “was likely to warrant a forceful tightening of monetary policy”.

BoE projections show inflation peaking at 6.2% in Q1 2027 under most inflationary scenario if rates only rise as markets expect.

Market reaction to BoE policy announcements

The Pound Sterling shows little reaction to the BoE policy announcements, with GBP/USD up 0.34% on the day at 1.3515, as of writing.

Pound Sterling Price Today

The table below shows the percentage change of British Pound (GBP) against listed major currencies today. British Pound was the strongest against the US Dollar.

| USD | EUR | GBP | JPY | CAD | AUD | NZD | CHF | |

|---|---|---|---|---|---|---|---|---|

| USD | -0.24% | -0.31% | -1.90% | -0.22% | -0.52% | -0.59% | -0.69% | |

| EUR | 0.24% | -0.03% | -1.68% | 0.02% | -0.27% | -0.32% | -0.42% | |

| GBP | 0.31% | 0.03% | -1.66% | 0.06% | -0.22% | -0.27% | -0.39% | |

| JPY | 1.90% | 1.68% | 1.66% | 1.70% | 1.41% | 1.29% | 1.20% | |

| CAD | 0.22% | -0.02% | -0.06% | -1.70% | -0.31% | -0.39% | -0.48% | |

| AUD | 0.52% | 0.27% | 0.22% | -1.41% | 0.31% | -0.05% | -0.15% | |

| NZD | 0.59% | 0.32% | 0.27% | -1.29% | 0.39% | 0.05% | -0.10% | |

| CHF | 0.69% | 0.42% | 0.39% | -1.20% | 0.48% | 0.15% | 0.10% |

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the British Pound from the left column and move along the horizontal line to the US Dollar, the percentage change displayed in the box will represent GBP (base)/USD (quote).