The Pound Sterling comes under pressure against its peers after the BoE’s interest rate decision.

The BoE maintains the status quo, leaving interest rates unchanged at 3.75%.

On Wednesday, the Fed held interest rates steady in the range of 3.50%-3.75%.

The Pound Sterling (GBP) faces selling pressure, prima facie, after the Bank of England’s (BoE) monetary policy announcement. As expected, the BoE has left interest rates unchanged at 3.75%, with an 8-1 majority. This is the third straight meeting that the BoE has maintained the status quo.

BoE Chief Economist Huw Pill was the one Monetary Policy Committee (MPC) member who dissented from the hold decision and voted for an interest rate hike. Pill was expected to advocate an interest rate hike, as he stated in an event in the middle of the month, that interest rates should be raised for inflation to return to the central bank’s 2% target.

The BoE needs to make decisions that give “the most insurance” against a repeat of the 2022 inflation shock, Pill argued, warning against a “wait and see approach,” Bloomberg reported.

Meanwhile, the US Dollar (USD) faces intense selling despite growing concerns over the Strait of Hormuz outlook and a hawkish Federal Reserve (Fed) hold.

United States (US) President Donald Trump stated on late Wednesday that Washington’s naval blockade of Iranian sea ports will continue until Iran gives up its nuclear ambitions.

On Wednesday, the Fed left interest rates unchanged at 3.50%-3.75%, however, three members of the rate-setting committee dissented the decision and advocated for a move away from the monetary easing bias.

Going forward, investors will focus on the US preliminary Gross Domestic Product (GDP) data, which will be published at 12:30 GMT. On an annualized basis, the US GDP growth is expected to have remained higher at 2.3% against the previous reading of 0.5%.

H is for hawk The Bank of England will announce its latest policy decision at midday on Thursday. The market is expecting no change in rates from the Bank, and we expect an 8-1 vote split, with one of the noted hawks at the bank voting to increase rates.

The backdrop to this meeting is a deeply uncertain global outlook and the threat of a bigger inflation spike after another surge in the oil price, which has risen to a fresh war-time high on Thursday morning to more than $123 per barrel for Brent, as the blockade in the Strait of Hormuz looks like it will be in place for the long term and as Donald Trump mulls ending the ceasefire with Iran. We expect the BOE to remain as calm and composed as possible considering the backdrop, and to stress the uncertain outlook, however, now that the oil price is rising again and oil supply is likely to remain constrained for the long term, the BOE may find it hard to avoid straying into hawkish territory as it balances growth risks with inflation concerns.

We expect the Bank will stress the need to watch for second round inflation effects, for example wage growth. So far, the survey data does not suggest that firms are likely to raise wages, and the labor market is still soft, even if the unemployment rate fell below 5% in the 3 months to February. The latest DMP survey shows that expectations for wage growth this year are unchanged at 3.5%. The Bank may also address the increase in inflation expectations, which rose by 2.1% in March, according to the latest Citi-YouGov survey. This suggests that consumers are concerned about a 2022-style energy price shock, even if the Bank has been keen to stress that the economic backdrop is different this time.

Assessing the chance of a hawkish shock at the BOE

A hawkish shock would be a larger number of MPC members voting for a rate hike, especially since signals coming from the March data have been resilient so far. If we get a 6-3 split, then this could open the door to a June rate hike. That might sound hasty, however, an early hike could nip in the bud any threat of second round inflation effects, especially if the blockade of the Strait of Hormuz lasts for the long term and the oil price stays in triple figures.

What will the BOE do next

Although we do not expect any forward guidance from the BOE at today’s meeting, the market is convinced that the next move from the BOE is a rate hike. There is roughly an 84% chance of two rate hikes from the BOE this year, and the market expects rates to rise to 4.25% to combat the threat of rising inflation caused by the energy price spike. The market is expecting the BOE to signal that rates will remain higher for longer, and for now, UK inflation is expected to peak at 4% this year.

Fed’s hawkish tilt

Today’s BOE meeting follows Wednesday night’s Fed meeting. The Fed did not change policy, but it is worth noting that its policy decision was the most divided since 1992. On the back of the Fed meeting, traders now see a rate hike as more likely than a rate cut for this year, following the Fed’s hawkish hold on Jerome Powell’s last meeting as chair. There is now an 11% chance of a hike from the Fed this year, up from 5% prior to the meeting. The Fed did not change the language used in its statement at this meeting, which suggests that cuts could still be on the cards for US interest rates. However, Powell suggested that this language could be adapted in future if elevated oil prices persist and three Fed governors opposed the current language used in the statement.

The market reacted to the hawkish tone at the Fed. The Dow Jones slumped 250 points, the dollar ticked higher and US stock index futures are also pointing to losses for the S&P 500 on Thursday. We think that the market reaction to the BOE meeting is likely to be mostly felt in the bond market. UK 2-year yields rose by 8 bps on Wednesday, and yields are higher by 26bps in the past month. The 2-year yield is now trading at 4.55%, so a lot of BOE hawkishness is already priced into UK bonds. We think that the oil price is more important for the direction of UK yields and sentiment towards UK assets more generally. UK stocks have slipped behind their US counterparts in recent weeks, and until there is a rotation out of US tech stocks and into defense names like BAE Systems and Rolls Royce, we could see the UK index may continue to struggle.

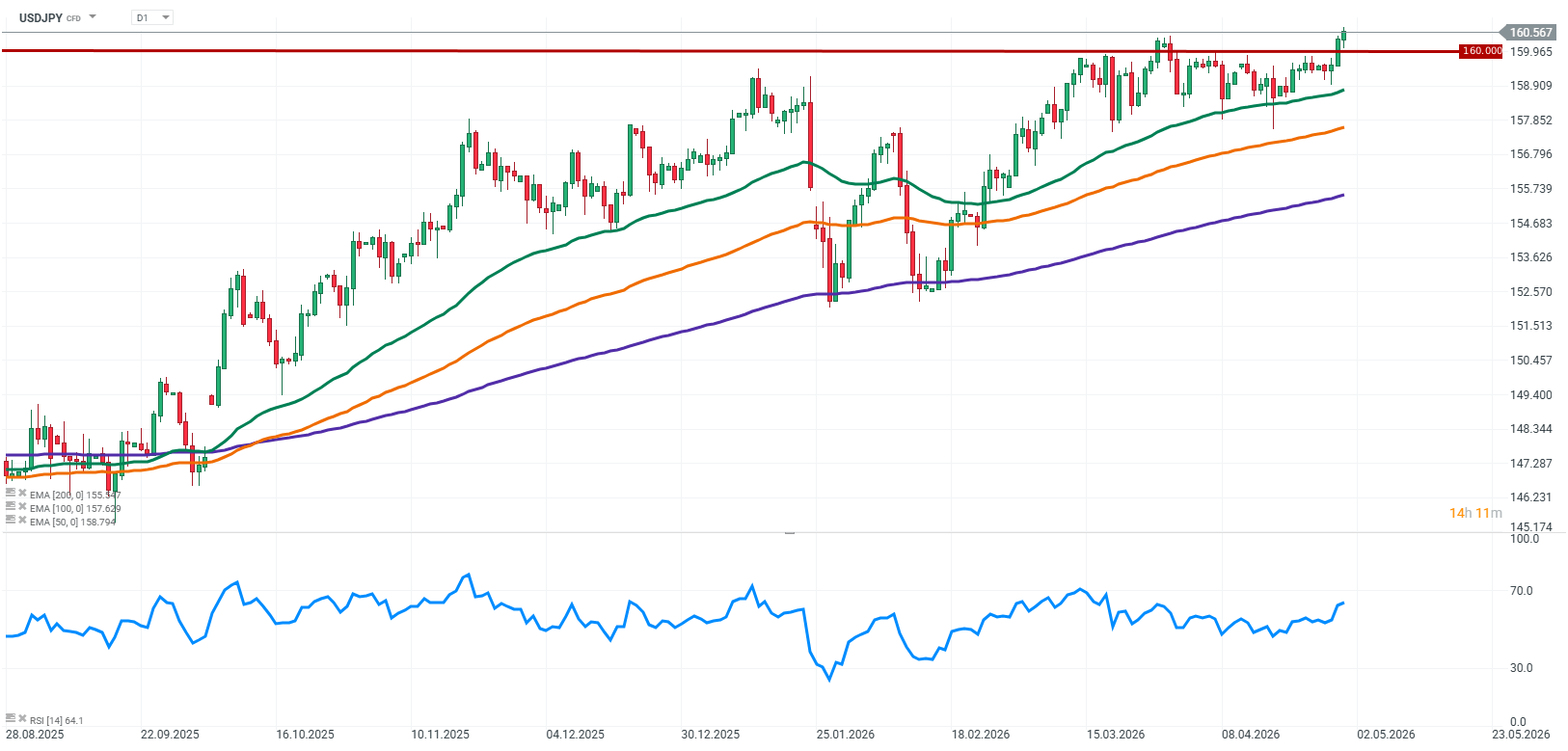

USDJPY has decisively broken through the psychological 160 level, reaching new multi-month highs and entering territory that was until recently treated as an informal red line for Japanese authorities. Importantly, the breakout has not been met with any strong verbal pushback from the Ministry of Finance, which the market interprets as a growing tolerance for further yen weakness, at least in the short term. This move is not happening in isolation. It reflects the classic combination of two dominant macro forces: a persistently wide interest rate differential and mounting pressures within Japan’s real economy, which are becoming increasingly difficult to ignore.

Source xStation5

What is driving USDJPY?Fed and BOJ stable rates, diverging narratives

Both the Federal Reserve and the Bank of Japan left interest rates unchanged, which in itself was not a surprise for markets. The key focus, however, was on communication nuances that further widened the divergence between the two economies. The Fed remains relatively hawkish, emphasizing the resilience of the US economy and a lack of urgency to pivot toward rate cuts. As a result, the dollar continues to benefit from higher yields and the sustained attractiveness of carry trade strategies. On the other side, the BOJ remains cautious, trying to balance the end of ultra-loose monetary policy with the risks of tightening too quickly. However, it is becoming increasingly clear that the issue is no longer only imported inflation driven by commodities, but also yen weakness itself, which is now amplifying domestic price pressures.

Japan trapped in a cost and commodities squeeze

Japan’s economic fundamentals are sending increasingly mixed signals. Retail sales suggest some resilience in consumer demand, while industrial production disappointed in March, partly due to supply chain disruptions and rising cost pressures linked to global commodity tensions. Particularly important is the situation around the Strait of Hormuz, which continues to elevate risks for global oil and gas flows. For Japan, a heavily import-dependent energy economy, this translates into higher production costs and a deteriorating trade balance. In this context, reports of a possible return of energy subsidies during the summer highlight the government’s attempt to cushion cost pressures, although such measures appear more like short-term stabilization tools rather than a structural response to persistent yen weakness.

160 as a psychological level and a test of market patience

The break above 160 is not purely a technical move. It represents a direct test of Japan’s tolerance threshold for currency weakness. Historically, these levels have been associated with heightened sensitivity from authorities, yet the lack of immediate reaction is encouraging the market to probe further. At this stage, the balance of forces remains tilted toward fundamentals. A persistently wide US–Japan rate differential continues to support capital flows into the dollar, while weak Japanese industrial data and commodity-driven pressures leave the BOJ with little room to tighten policy aggressively in the near term.

Outlook

The current USDJPY move increasingly resembles a classic carry trade driven environment, where fundamentals and momentum reinforce each other. Unless there is a meaningful shift in BOJ policy or a more forceful intervention from the Ministry of Finance, the path of least resistance remains higher. The key question is no longer whether 160 would be broken, but how long the market will continue testing the absence of intervention and where the true line in the sand ultimately lies.

EUR/GBP softens to around 0.8660 in Thursday’s early European session.

German Retail Sales fell by 2.0% MoM in March, weaker than expected.

The ECB and BoE interest rate decisions will take center stage later on Thursday.

The EUR/GBP cross declines to near 0.8660 during the early European trading hours on Thursday. The Euro (EUR) weakens against the Pound Sterling (GBP) following the downbeat German Retail Sales data. The preliminary readings of Gross Domestic Product (GDP) from Germany and the Eurozone are due later on Thursday. Also, the European Central Bank (ECB) and the Bank of England (BoE) interest rate decisions will be in the spotlight.

Data released by Destatis on Thursday showed that German Retail Sales, a key measure of consumer spending, fell 2.0% MoM in March. This figure followed a decline of 0.3% in February (revised from -0.6%) and came in weaker than the expectations of a 0.1% decrease.

On an annualized basis, Retail Sales dropped 2.0% in March, versus an estimated rise of 0.5% and the prior release of 0.9% growth (revised from 0.7%). The EUR attracts some sellers in an immediate reaction to the weaker German economic data.

The ECB is widely expected to keep interest rates unchanged at its policy meeting on Thursday due to high uncertainty. Nonetheless, rising inflation, driven by energy price volatility from the Iran war, has raised the expectation of a rate hike in June. Economists predict a quarter-point hike at June’s meeting, and markets now fully price two additional ones after that before the year is out, according to Bloomberg.

The BoE is likely to keep interest rates on hold at its April policy meeting on Thursday as it awaits the economic fallout from the Iran war. Traders will closely monitor the speech from BoE Governor Andrew Bailey for any suggestions that higher borrowing costs are likely to be needed.

“The hikes fully priced into financial markets were already weighing on the economy, reducing the likelihood that the BoE will actually have to raise Bank Rate, at least for now,” said Andrew Wishart, senior UK economist at Berenberg.

A report released by the Bank of Japan (BoJ) on Thursday revealed that the impact of weak Japanese Yen shock on inflation bigger than that from oil shock. The weakening of the JPY pushes up prices for wide range of goods services, thereby gives bigger boost to consumer inflation excluding fresh food, energy.

Key quotes

Impact of weak Yen shock on inflation bigger than that from oil shock.

Weak Yen pushes up prices for wide range of goods services, thereby gives bigger boost to consumer inflation excluding fresh food, energy.

Oil price rises put fairly big upward pressure on smaller number of goods related to energy, which means impact on CPI excluding fresh food, energy isn’t very big.

Weak Yen shock expands wage, profit margin and leads to increase in GDP deflater, while energy shock squeezes wage, profit margin and leads to decrease in GDP deflater.

Under risk scenario projecting elevated oil prices, weaker Yen, stock falls, real GDP forecasts will be -0.1% point to 0.2% point lower in fiscal 2026-2028 than BoJ’s median baseline projections.

Under risk scenario, core consumer inflation will overshoot significantly from BoJ’s median baseline projections, could hover around 3% in fiscal 2026, 2027.

Such overshoot of inflation could heighten medium-, long-term inflation expectations.

If there is big supply chain disruption, real GDP could undershoot sharply while bottlenecks could lead to non-linear rise in inflation.

BoJ will scrutinise various risk factors more than ever as growth, price developments could sharply deviate from its baseline projections depending on Middle East developments.

Market reaction

As of writing, the USD/JPY pair is up 0.02% on the day at 160.48.

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.