Most market participants are currently forced to factor the potential short-term development of the situation in Iran into asset pricing. The scale, objectives and time horizon of military operations on both sides will have a real impact on markets. One question must nevertheless be asked: no war lasts forever.

What will happen once it ends?

Armed conflicts are negative-sum undertakings. The enormous scale of destruction and the volume of resources burned in sustaining them impose a limited time horizon on such wars. The same applies to the ongoing conflict in the Persian Gulf. The United States is facing mounting pressure from fuel and fertilizer prices, while inflation and the midterm elections are looming ever larger over President Donald Trump’s administration. On the Iranian side, the situation is even worse. The backward and neglected economy of an overcrowded desert state cannot survive under conditions of continuous and large-scale bombardment by the United States and Israel. The blockade of the Strait of Hormuz also means that both European and Asian countries, despite their lack of direct involvement in the conflict, have a vital interest in its de-escalation or at the very least in reopening the strait.

In light of all available information and based on cautious forecasts, it is already possible at this stage of the conflict to identify a number of scenarios that appear the most likely and to analyze how they may affect financial markets.

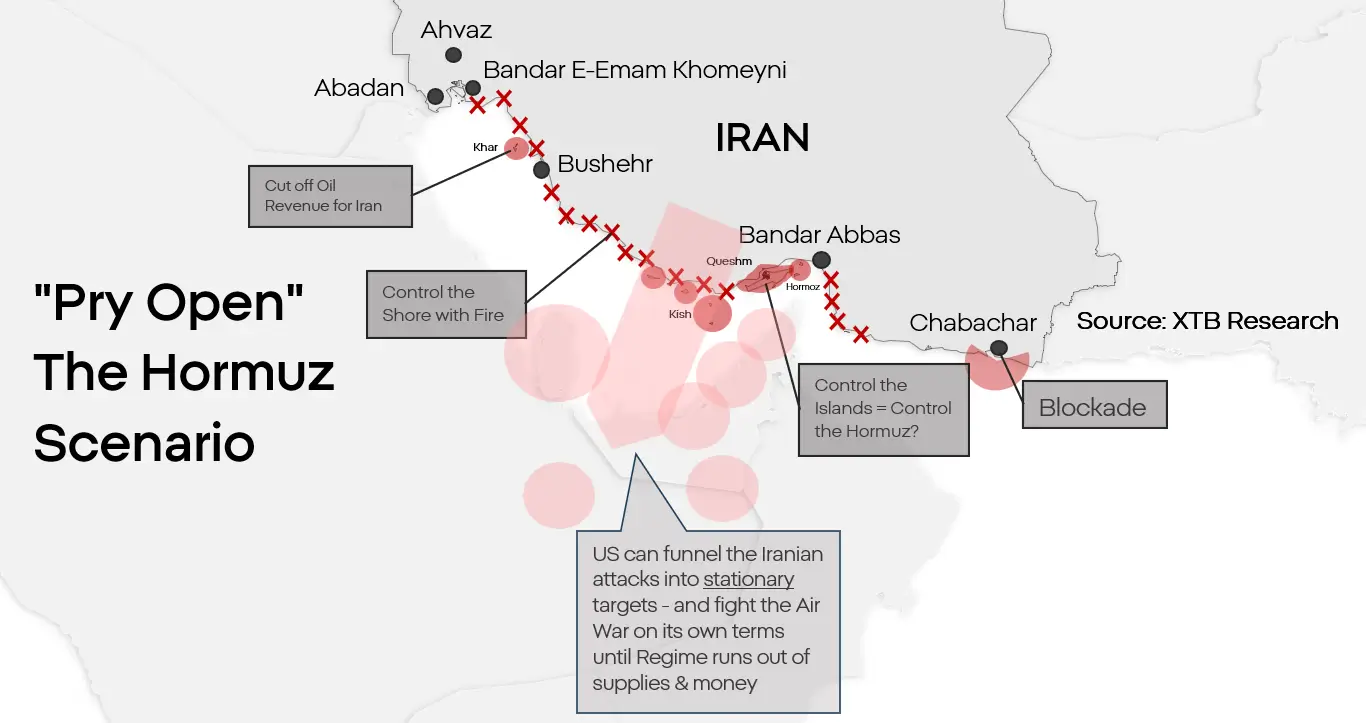

Scenario 1. Forcing the strait open and partial normalization

For now, this appears to be the base-case scenario for which both sides are preparing. While a full-scale invasion of Iran is possible, contrary to the opinion of many observers, that does not mean it will be necessary. The United States does not need to conquer Iran. It needs to neutralize Iran’s nuclear program and reopen the Strait of Hormuz. This scenario assumes a landing on one or several islands in the strait, their seizure, and the control of the coastline through naval gunfire. Iran lacks the capability to defend forward positions along the Persian Gulf coast, and the drones it uses to attack tankers are not capable of striking moving targets from deep inland. Paralysing Iran’s ability to block the strait would, over time, remove the main constraints on the American side and deprive Iran of its most important lever. This would in no way mean the fall of the government of the Islamic Republic, but over time it could force Iran into some form of ceasefire or even a limited yet still functional capitulation.

Market reaction:

- Support for oil prices primarily over the longer term. Such an operation could last many months, and Iran, even if defeated, would remain dangerous. Beyond the costs of reconstruction and the normalization of supply chains, this would imply a persistent long-term risk premium tied to the possibility of renewed conflict in the strait.

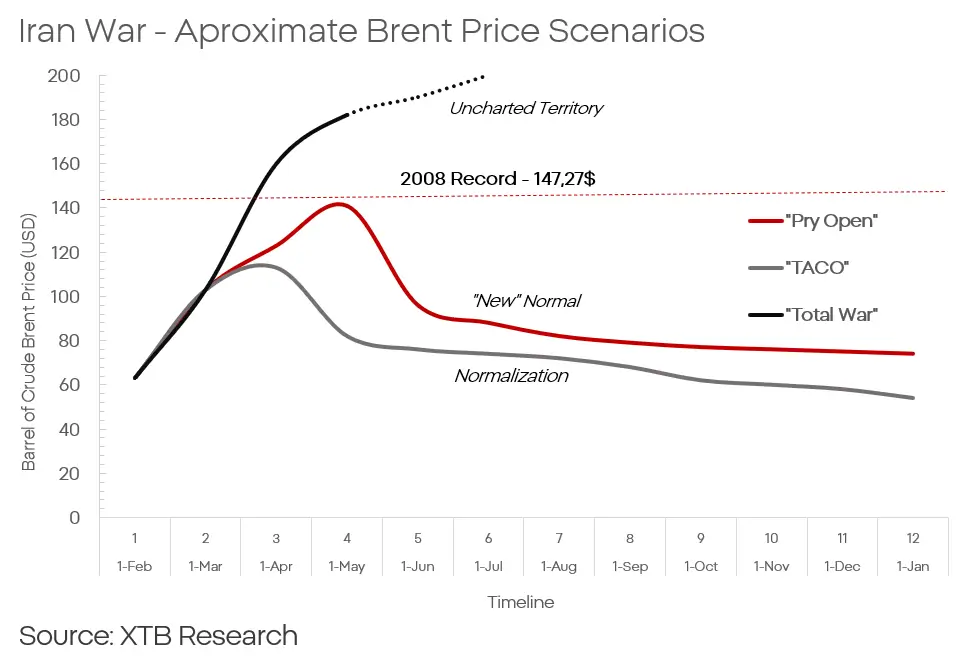

- A short-term rise in Brent to around $120 to $140 per barrel

- Followed by a gradual decline to around $80 per barrel, with a long-term risk premium of $5 to $10

- Escalation could also support gold prices and valuations of defense-sector companies.

- A 5 to 7% increase in gold prices is possible in the short to medium term on the back of escalation.

- It would also put pressure on emerging-market currencies.

- A long-term but moderate decline in Asian equities and parts of the European market is also likely.

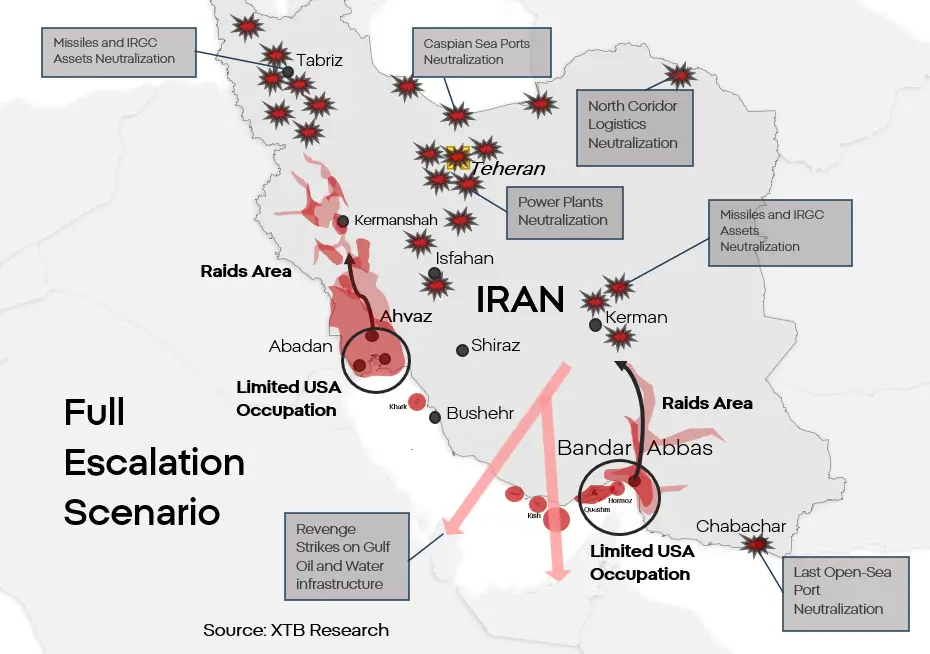

Scenario 2. Total escalation and a fragile peace

This is the logical “maximum option”, representing an extension of the first scenario. It assumes a genuine attempt to destroy the Iranian regime in its current form and to sign some kind of “agreement” with whatever remains of it. It should be remembered that both sides, though the United States to a greater extent, are still limiting the scale of their attacks and the profile of their targets. The United States could combine a ground strike with attacks on critical infrastructure. Damage to infrastructure used for energy production and water supply in Iran would lead to a humanitarian crisis on a scale that is difficult to imagine. A scale that would make it impossible for the regime to continue military operations and organized resistance. In retaliation, Iran would attempt to strike, with all remaining means, desalination infrastructure as well as extraction and refining assets in the GCC states. Iran does not possess the capability to cause a full collapse of energy and water systems on the other side of the Gulf. However, the destruction could be severe enough to force the evacuation of part of the population from the area, while infrastructure damage could leave installations out of use for many months after the end of the conflict.

Neither the Iranian military nor the IRGC is capable of repelling a determined American ground assault, should one occur. The combination of unrestricted strikes on Iran and a limited ground invasion in the region, for example in Khuzestan or Bandar Abbas, would give the United States room to establish a forward operating base for special forces raids aimed at neutralizing Iran’s nuclear program and/or supporting any anti-government movements. Such a scenario would, at enormous cost to all sides, lead to the partial or complete neutralization of Iran as a threat to the region.

Market reaction:

- The rise in oil prices would be larger and more violent, although it is difficult to predict how prices would behave over the long term given such a major shift in the regional balance of power.

- The price of Brent could initially reach as high as $160 to $180 per barrel

- Gold prices could also rise.

- A return to $5,100 would be within reach.

- The conflict would likely spread geographically even further, which could push airline stocks even lower.

- Another sell-off of around 6 to 10% should be expected.

- The dollar could once again experience extraordinary gains, similar to those seen in 2022.

- Possible levels would be around 1.18-1,2 on EUR/USD and 3.8 to 3.9 on USD/PLN

- Defense-sector stocks would likely reach new highs.

Scenario 3. Iranian-style “TACO”

Escalation is currently the base-case scenario, but it is not the only one. Although it would undoubtedly be difficult, Donald Trump may decide to attempt to withdraw the United States from the conflict without bringing it to a definitive resolution. A scenario involving de-escalation and a U.S. withdrawal from the strait on terms close to those desired by Iran is less likely, not only because it would represent a reputational defeat for the United States, but also because of the difficult-to-ignore informal influence Israel exerts on American foreign policy. That does not mean, however, that it is impossible. A military defeat, political crisis or economic crisis could force the United States into some form of compromise that, from Washington’s perspective, would amount to defeat. Such a compromise could be more or less formal and would ultimately involve some form of sanctions relief in exchange for a certain degree or type of disarmament on Iran’s part.

Market reaction:

- In the scenario most favorable to Iran, the possibility would emerge for the country to reintegrate into the global market. In the medium and long term, this would imply a collapse in oil prices.

- After a ceasefire is signed, oil could quickly fall to around $75 per barrel, and over the course of several quarters could even reach the $50 range.

- A decline in geopolitical risk would put pressure on the dollar and defense stocks.

- A gradual return of EUR/USD to around 1.10 – 1.12 would be possible.

- Despite the decline in risk, gold should still perform relatively well due to inflation risk and demand from central banks.

- That would not, however, apply to silver or platinum.

- A rebound in cryptocurrencies and in the shares of companies most heavily hit by the conflict, such as airlines, car manufacturers and the tourism sector, would also be possible.

- Gains could range from several to even a dozen or so percent.

- This would also represent a reputational, and not only reputational, defeat for the United States. In the short term, this might not have a major effect on capital allocation, but over the longer term it could lead to a shift in the economic and market center of gravity away from the United States and toward Europe and Asia.

The material on this page does not constitute financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other specific needs. All information provided, including opinions, market research, mathematical results and technical analyzes published on the Website or transmitted To you by other means, it is provided for information purposes only and should in no way be construed as an offer or solicitation for a transaction in any financial instrument, nor should the information provided be construed as advice of a legal or financial nature on which any investment decisions you make should be based exclusively To your level of understanding, investment objectives, financial situation, or other specific needs, any decision to act on the information published on the Website or sent to you by other means is entirely at your own risk if you In doubt or unsure about your understanding of a particular product, instrument, service or transaction, you should seek professional or legal advice before trading. Investing in CFDs carries a high level of risk, as they are leveraged products and have small movements Often the market can result in much larger movements in the value of your investment, and this can work against you or in your favor. Please ensure you fully understand the risks involved, taking into account investments objectives and level of experience, before trading and, if necessary, seek independent advice.