The past week was marked by crude oil prices returning to triple digits on expiring September contracts and a continuation of the equity market selloff. Geopolitics once again served as the primary driver for investors, fueled not only by the situation in the Middle East but also by broad new US tariffs. Wall Street earnings season delivered solid corporate results, though these proved insufficient to lift investor sentiment. A fresh wave of reports from tech giants such as Microsoft and Apple might alter that dynamic. Furthermore, decision day arrives for two key central banks, namely the Federal Reserve and the Bank of Japan. Given this concentration of high-impact events, three markets warrant close attention in the coming days: USD/JPY , Gold and US100 .

USDJPY

The Japanese currency has struggled recently, with the past week defined by mounting inflationary pressure in Japan driven in part by higher global energy costs. This week brings a direct showdown between two major central banks. On Wednesday, the FOMC will announce its policy decision, followed by the second press conference from the new Fed Chair Kevin Warsh. On Friday, the Bank of Japan will present its stance on interest rates, preceded in the morning by the Tokyo consumer price index release. Market consensus anticipates that both the Fed and the BoJ will hold interest rates at current levels, with the BoJ policy rate currently at 1.0 percent. Investors will focus heavily on potential guidance regarding future monetary tightening, particularly given that the yen trades near 40-year lows alongside rising import costs. Historical currency interventions in Japan demonstrate that verbal pressure alone, lacking decisive BoJ action, offers only temporary relief for the yen. Moreover, sentiment conveyed by the US central bank remains the primary catalyst for USD/JPY trends. Should the Fed maintain a hawkish stance while the BoJ holds back from aggressive signals due to growth concerns, USDJPY could resume its upward trajectory toward the 165 level. Conversely, a hawkish surprise from the BoJ, supported by a hotter Tokyo CPI reading and upwardly revised inflation forecasts, could trigger a sharp rally in the yen and force a rapid unwinding of massive speculative short positions.

Gold

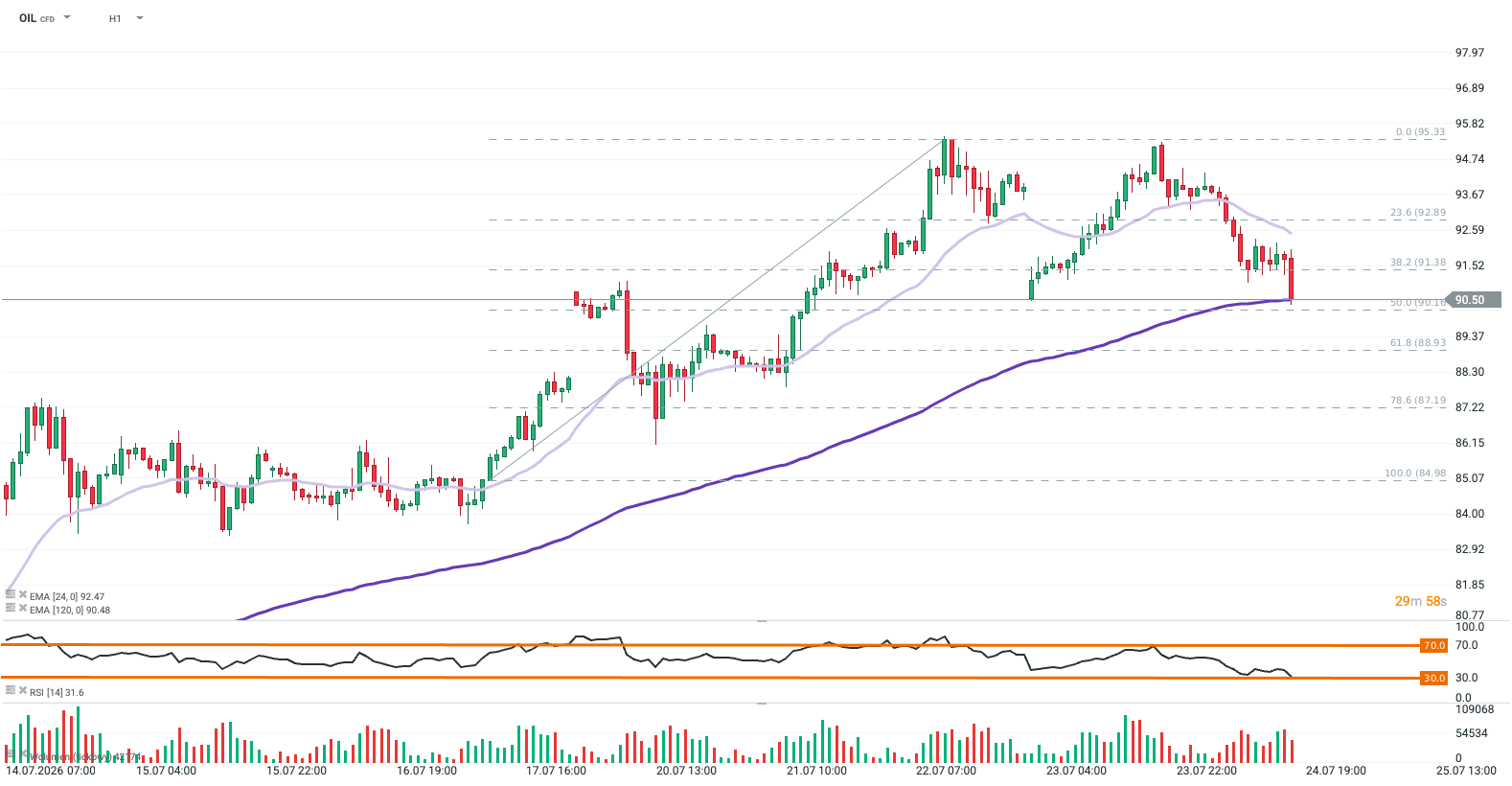

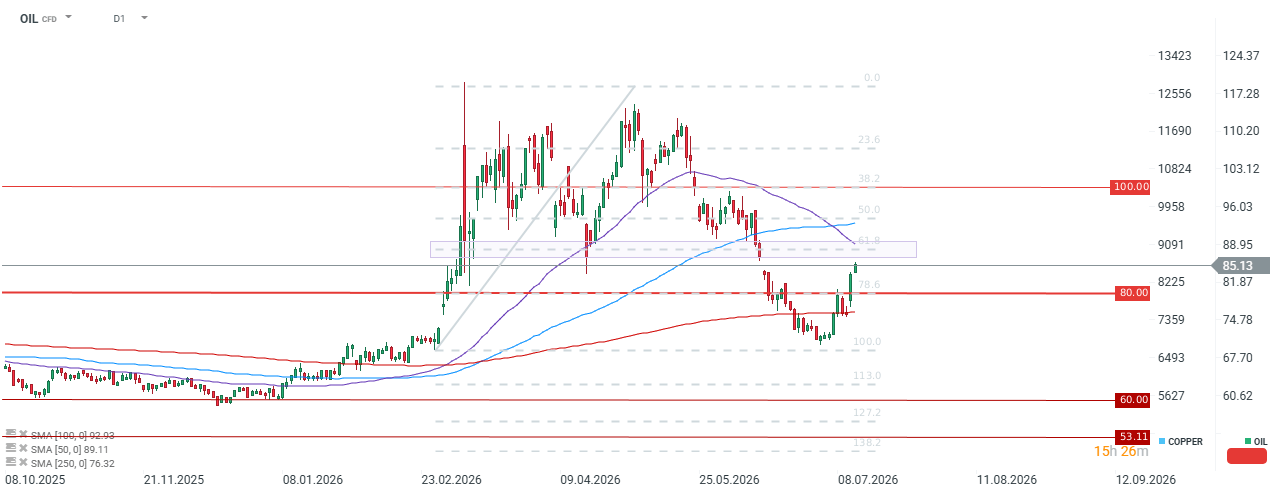

While last week was shaped by shifting sentiment surrounding Middle Eastern geopolitical tensions and oil prices, this week presents a direct test for the gold market from US monetary policy and incoming economic data. The principal catalyst for volatility will be Wednesday’s FOMC decision, followed on Thursday by US GDP figures and the June PCE inflation metric, which remains the Federal Reserve’s preferred inflation gauge. Gold continues to show high sensitivity to real interest rates and the trajectory of US Treasury yields. The bullion’s historic gains during periods when rate cuts are priced in clearly illustrate this relationship: as real yields decline, capital shifts smoothly into non-yielding assets. If Thursday’s PCE report points to persistent inflationary pressures and the Fed signals that rates must remain elevated for longer, gold could stay under pressure, particularly if crude oil marches back toward 100 dollars per barrel. In the alternative scenario, featuring a cooler PCE reading and waning geopolitical risk, the precious metal would gain strong momentum to break out of its recent downtrend.

US100 (Nasdaq 100 Futures)

The past week delivered another wave of selling across the global semiconductor and AI memory sectors. This week introduces the next slate of Big Tech quarterly earnings on Wall Street, coinciding directly with the Federal Reserve meeting. On Wednesday, Microsoft and Meta Platforms will report their quarterly results, followed by Apple and Amazon on Thursday. These announcements overlap with the FOMC interest rate decision on Wednesday and the US GDP and PCE releases on Thursday. Investors will scrutinize not only top-line revenue growth but primarily the return on capital expenditure dedicated to artificial intelligence infrastructure. Stretched valuations among Big Tech firms leave a remarkably narrow margin for error. Market dynamics seen during previous tech corrections demonstrate that even minor disappointment regarding forward margin outlooks can trigger index-wide selling, regardless of robust current earnings. Strong reports from market leaders coupled with measured commentary from the Fed could provide the US100 with the momentum needed to rebound from its recent pullbacks. Conversely, disappointing forward guidance paired with hawkish rhetoric from Kevin Warsh risks deepening the ongoing correction.