US Dollar Index declines as safe-haven demand fades amid growing optimism over easing Middle East tensions.

Trump said that the US may withdraw from the Iran conflict within two to three weeks.

Fed’s Powell said long-term inflation expectations remain well anchored.

The US Dollar Index (DXY), which measures the value of the US Dollar (USD) against six major currencies, is extending its losses for the second successive day and hovering around 99.80 during the Asian hours on Wednesday.

The Greenback weakens amid fading safe-haven demand amid a moderation in Middle East tensions. US President Donald Trump stated on Tuesday that the United States (US) would be “leaving very soon” from the Iran war, noting that a withdrawal could take place within two to three weeks. The comments reinforce earlier remarks suggesting that US strategic objectives have largely been fulfilled, raising expectations of a relatively swift resolution to the conflict.

Iranian President Masoud Pezeshkian expressed a willingness to de-escalate regional tensions if specific guarantees are met. However, Foreign Minister Abbas Araghchi took a firmer stance, asserting that Tehran is not seeking a temporary ceasefire but rather a complete termination of the war. He stressed the need for binding assurances against future aggression as well as compensation for damages, highlighting lingering uncertainty around the conflict’s resolution.

Moreover, Federal Reserve (Fed) Chair Jerome Powell said earlier that long-term inflation expectations remain well anchored, easing concerns that higher energy prices will quickly lift inflation and reduce the urgency for policy action.

Most market participants are currently forced to factor the potential short-term development of the situation in Iran into asset pricing. The scale, objectives and time horizon of military operations on both sides will have a real impact on markets. One question must nevertheless be asked: no war lasts forever.

What will happen once it ends?

Armed conflicts are negative-sum undertakings. The enormous scale of destruction and the volume of resources burned in sustaining them impose a limited time horizon on such wars. The same applies to the ongoing conflict in the Persian Gulf. The United States is facing mounting pressure from fuel and fertilizer prices, while inflation and the midterm elections are looming ever larger over President Donald Trump’s administration. On the Iranian side, the situation is even worse. The backward and neglected economy of an overcrowded desert state cannot survive under conditions of continuous and large-scale bombardment by the United States and Israel. The blockade of the Strait of Hormuz also means that both European and Asian countries, despite their lack of direct involvement in the conflict, have a vital interest in its de-escalation or at the very least in reopening the strait.

In light of all available information and based on cautious forecasts, it is already possible at this stage of the conflict to identify a number of scenarios that appear the most likely and to analyze how they may affect financial markets.

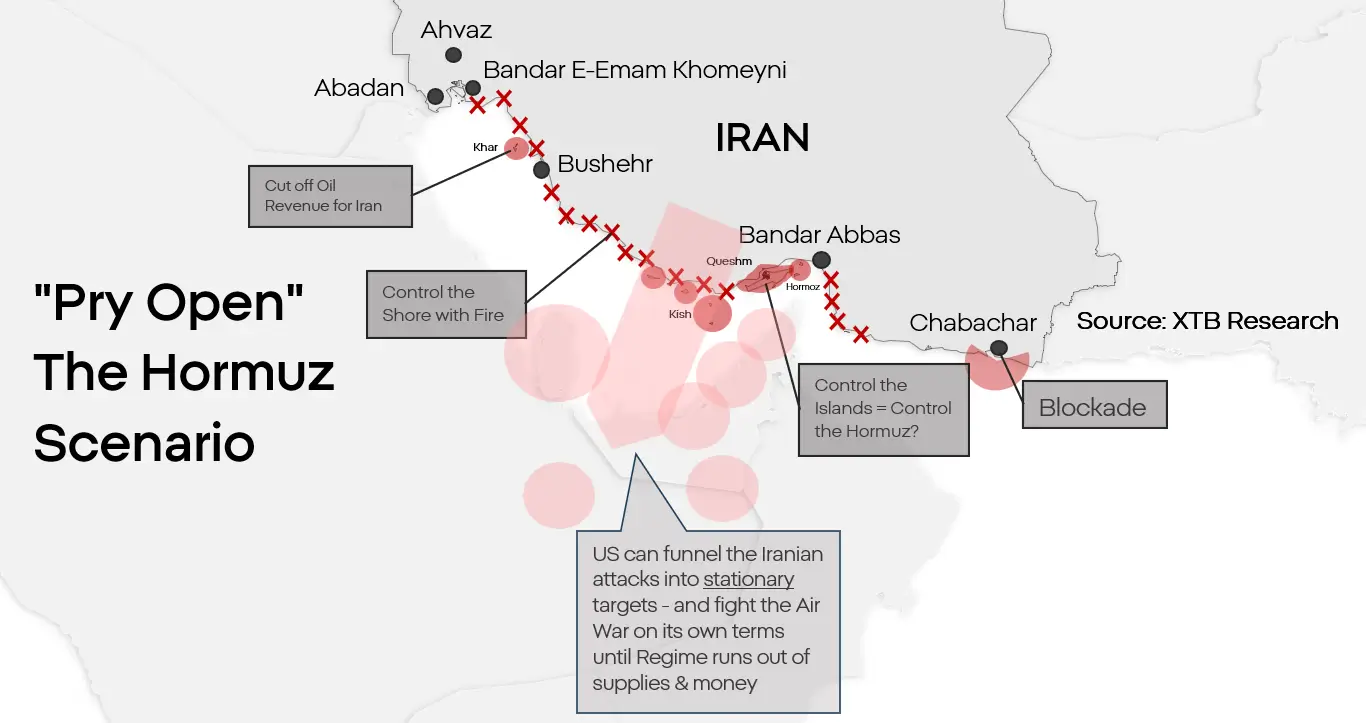

Scenario 1. Forcing the strait open and partial normalization

For now, this appears to be the base-case scenario for which both sides are preparing. While a full-scale invasion of Iran is possible, contrary to the opinion of many observers, that does not mean it will be necessary. The United States does not need to conquer Iran. It needs to neutralize Iran’s nuclear program and reopen the Strait of Hormuz. This scenario assumes a landing on one or several islands in the strait, their seizure, and the control of the coastline through naval gunfire. Iran lacks the capability to defend forward positions along the Persian Gulf coast, and the drones it uses to attack tankers are not capable of striking moving targets from deep inland. Paralysing Iran’s ability to block the strait would, over time, remove the main constraints on the American side and deprive Iran of its most important lever. This would in no way mean the fall of the government of the Islamic Republic, but over time it could force Iran into some form of ceasefire or even a limited yet still functional capitulation.

Market reaction:

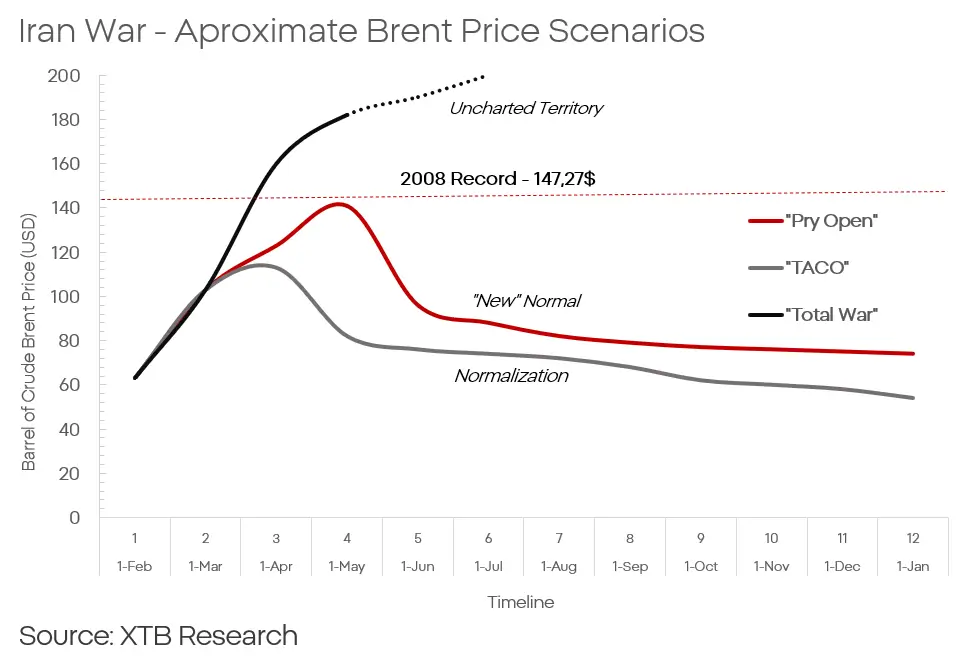

Support for oil prices primarily over the longer term. Such an operation could last many months, and Iran, even if defeated, would remain dangerous. Beyond the costs of reconstruction and the normalization of supply chains, this would imply a persistent long-term risk premium tied to the possibility of renewed conflict in the strait.

A short-term rise in Brent to around $120 to $140 per barrel

Followed by a gradual decline to around $80 per barrel, with a long-term risk premium of $5 to $10

Escalation could also support gold prices and valuations of defense-sector companies.

A 5 to 7% increase in gold prices is possible in the short to medium term on the back of escalation.

It would also put pressure on emerging-market currencies.

A long-term but moderate decline in Asian equities and parts of the European market is also likely.

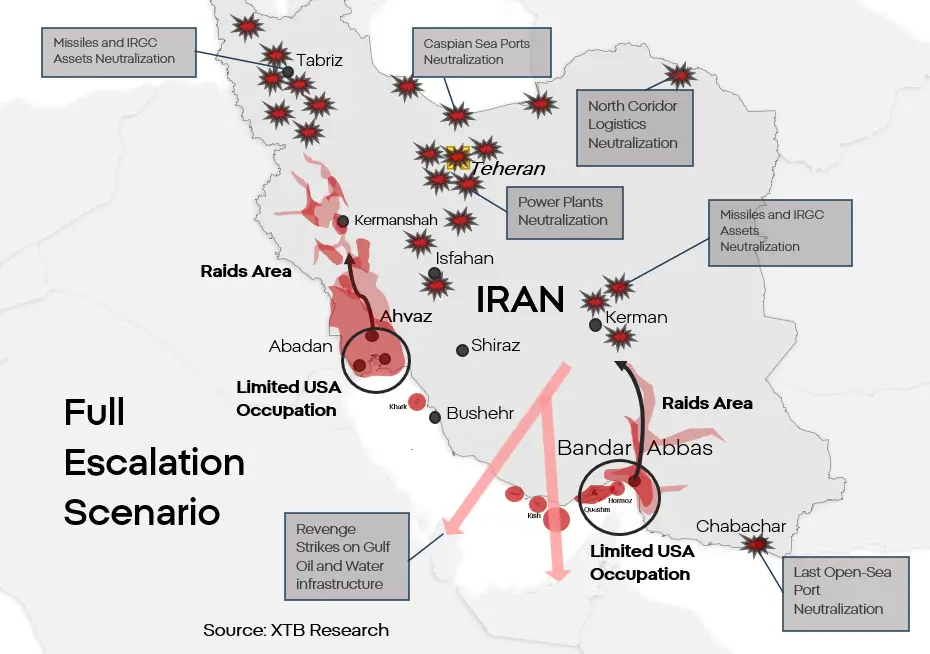

Scenario 2. Total escalation and a fragile peace

This is the logical “maximum option”, representing an extension of the first scenario. It assumes a genuine attempt to destroy the Iranian regime in its current form and to sign some kind of “agreement” with whatever remains of it. It should be remembered that both sides, though the United States to a greater extent, are still limiting the scale of their attacks and the profile of their targets. The United States could combine a ground strike with attacks on critical infrastructure. Damage to infrastructure used for energy production and water supply in Iran would lead to a humanitarian crisis on a scale that is difficult to imagine. A scale that would make it impossible for the regime to continue military operations and organized resistance. In retaliation, Iran would attempt to strike, with all remaining means, desalination infrastructure as well as extraction and refining assets in the GCC states. Iran does not possess the capability to cause a full collapse of energy and water systems on the other side of the Gulf. However, the destruction could be severe enough to force the evacuation of part of the population from the area, while infrastructure damage could leave installations out of use for many months after the end of the conflict.

Neither the Iranian military nor the IRGC is capable of repelling a determined American ground assault, should one occur. The combination of unrestricted strikes on Iran and a limited ground invasion in the region, for example in Khuzestan or Bandar Abbas, would give the United States room to establish a forward operating base for special forces raids aimed at neutralizing Iran’s nuclear program and/or supporting any anti-government movements. Such a scenario would, at enormous cost to all sides, lead to the partial or complete neutralization of Iran as a threat to the region.

Market reaction:

The rise in oil prices would be larger and more violent, although it is difficult to predict how prices would behave over the long term given such a major shift in the regional balance of power.

The price of Brent could initially reach as high as $160 to $180 per barrel

Gold prices could also rise.

A return to $5,100 would be within reach.

The conflict would likely spread geographically even further, which could push airline stocks even lower.

Another sell-off of around 6 to 10% should be expected.

The dollar could once again experience extraordinary gains, similar to those seen in 2022.

Possible levels would be around 1.18-1,2 on EUR/USD and 3.8 to 3.9 on USD/PLN

Defense-sector stocks would likely reach new highs.

Scenario 3. Iranian-style “TACO”

Escalation is currently the base-case scenario, but it is not the only one. Although it would undoubtedly be difficult, Donald Trump may decide to attempt to withdraw the United States from the conflict without bringing it to a definitive resolution. A scenario involving de-escalation and a U.S. withdrawal from the strait on terms close to those desired by Iran is less likely, not only because it would represent a reputational defeat for the United States, but also because of the difficult-to-ignore informal influence Israel exerts on American foreign policy. That does not mean, however, that it is impossible. A military defeat, political crisis or economic crisis could force the United States into some form of compromise that, from Washington’s perspective, would amount to defeat. Such a compromise could be more or less formal and would ultimately involve some form of sanctions relief in exchange for a certain degree or type of disarmament on Iran’s part.

Market reaction:

In the scenario most favorable to Iran, the possibility would emerge for the country to reintegrate into the global market. In the medium and long term, this would imply a collapse in oil prices.

After a ceasefire is signed, oil could quickly fall to around $75 per barrel, and over the course of several quarters could even reach the $50 range.

A decline in geopolitical risk would put pressure on the dollar and defense stocks.

A gradual return of EUR/USD to around 1.10 – 1.12 would be possible.

Despite the decline in risk, gold should still perform relatively well due to inflation risk and demand from central banks.

That would not, however, apply to silver or platinum.

A rebound in cryptocurrencies and in the shares of companies most heavily hit by the conflict, such as airlines, car manufacturers and the tourism sector, would also be possible.

Gains could range from several to even a dozen or so percent.

This would also represent a reputational, and not only reputational, defeat for the United States. In the short term, this might not have a major effect on capital allocation, but over the longer term it could lead to a shift in the economic and market center of gravity away from the United States and toward Europe and Asia.

The material on this page does not constitute financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other specific needs. All information provided, including opinions, market research, mathematical results and technical analyzes published on the Website or transmitted To you by other means, it is provided for information purposes only and should in no way be construed as an offer or solicitation for a transaction in any financial instrument, nor should the information provided be construed as advice of a legal or financial nature on which any investment decisions you make should be based exclusively To your level of understanding, investment objectives, financial situation, or other specific needs, any decision to act on the information published on the Website or sent to you by other means is entirely at your own risk if you In doubt or unsure about your understanding of a particular product, instrument, service or transaction, you should seek professional or legal advice before trading. Investing in CFDs carries a high level of risk, as they are leveraged products and have small movements Often the market can result in much larger movements in the value of your investment, and this can work against you or in your favor. Please ensure you fully understand the risks involved, taking into account investments objectives and level of experience, before trading and, if necessary, seek independent advice.

USD/CAD rises to fresh three-month highs despite a softer US Dollar.

Canada’s GDP signals a soft start to the year, with a modest rebound expected in February.

US Dollar eases from multi-month highs as traders reassess risk sentiment.

USD/CAD edges higher on Tuesday, with the Canadian Dollar (CAD) extending its decline against the US Dollar (USD) for a seventh consecutive day, even as the Greenback eases. At the time of writing, the pair is trading around 1.3960, hovering near its highest level since December 2025.

The US Dollar Index (DXY), which tracks the Greenback’s value against a basket of six major currencies, is trading near 100.17, pulling back after touching fresh ten-month highs of 100.64 earlier in the day.

The pullback in the US Dollar appears largely technical, while some easing in geopolitical risk sentiment is also weighing on demand after The Wall Street Journal reported that Donald Trump is willing to end the US military campaign against Iran even if the Strait of Hormuz remains largely closed.

However, geopolitical risks remain elevated. Iran’s Islamic Revolutionary Guard Corps (IRGC) warned that it could target US companies in the region starting April 1 in retaliation for recent attacks.

The Loonie has remained under sustained pressure since the US-Israel war with Iran erupted, pushing energy prices sharply higher. While Canada is a net Oil exporter, persistent downside pressure on the CAD reflects growing concerns that elevated energy costs could weigh on domestic demand and slow broader economic growth.

Adding to the cautious tone, Canada’s January Gross Domestic Product (GDP) rose by 0.1% MoM, slightly above expectations for a flat reading, though it marked a slowdown from the previous 0.2% expansion, pointing to soft underlying economic momentum at the start of the year.

However, preliminary estimates suggest that real GDP rose by 0.2% in February, indicating a modest pickup in activity and keeping growth broadly in line with the Bank of Canada’s 1.8% projection outlined in its January Monetary Policy Report.

Meanwhile, traders are increasingly pricing in at least two Bank of Canada (BoC) rate hikes by year-end amid oil-driven inflation pressures. However, persistent labour market headwinds and contained underlying inflation suggest the Bank could remain patient, with rate hikes likely only if Oil prices stay elevated for longer.

In the United States, economic data released on Tuesday showed that JOLTS Job Openings fell to 6.882 million in February from 7.24 million in January, slightly below expectations of 6.92 million.

US Conference Board Consumer Confidence rose to 91.8 in March, beating forecasts of 87.9 and improving from 91 in February.

EUR/GBP trades choppy as traders assess Eurozone inflation and UK growth data.

Rising energy costs push Eurozone inflation above target, adding pressure on the ECB.

UK growth stays weak, limiting the scope for aggressive BoE tightening.

EUR/GBP trades in a choppy range on Tuesday, as traders digest the latest economic data from both the United Kingdom and the Eurozone. At the time of writing, the cross is trading around 0.8691, rebounding after marking an intraday low of 0.8676.

The latest Eurozone preliminary inflation data, the first since the escalation of tensions in the Middle East, showed early signs of the impact from rising energy prices, pushing inflation above the ECB’s 2% target.

Headline inflation showed a notable pickup, with the Harmonized Index of Consumer Prices (HICP) rising by 1.2% MoM in March, accelerating from 0.6% in February. On an annual basis, inflation rose to 2.5% from 1.9%, coming in below expectations of 2.7%.

Core inflation, however, remained more contained. The Core HICP rose 0.8% MoM, unchanged from the previous month, while the annual rate eased slightly to 2.3%, coming in below both the 2.4% forecast and the prior reading.

The data strengthen the case that the European Central Bank (ECB) could consider raising rates in the coming months if Oil prices remain elevated. However, markets are scaling back expectations of any immediate rate hike that had been priced in earlier, as rising energy costs are also fueling concerns about an economic slowdown, particularly in the Eurozone given its heavy reliance on imported energy.

EU Energy Commissioner Dan Jørgensen warned that member states should prepare for a prolonged disruption to energy markets due to the Iran war, according to a letter sent to EU energy ministers.

ECB policymaker Madis Müller said on Tuesday that “the ECB must act if energy prices stay high for a long period,” adding that a rate hike in April “cannot be ruled out.”

In the United Kingdom, growth remained modest. GDP rose 0.1% QoQ in Q4, in line with expectations and unchanged from the preliminary estimate. On a yearly basis, the economy grew 1%, also matching forecasts.

Meanwhile, traders expect the Bank of England (BoE) to consider rate hikes to deal with oil-driven inflation. However, weak growth in the UK, reflected in the latest Q4 GDP data, points to a stagflationary environment, complicating the central bank’s policy outlook.

The euro closed March below $1.15, nearing its lowest point in nearly two weeks, after a volatile month marked by escalating tensions in the Middle East. The common currency lost over 2% against the dollar as traders assessed the economic impact of the deepening conflict. Adding to the uncertainty, a Wall Street Journal report revealed that US President Donald Trump had signaled a potential end to the US military campaign against Iran, even if the critical Strait of Hormuz remained largely blocked. Soaring oil prices fueled inflation across Europe, prompting markets to drastically revise their expectations for the European Central Bank’s policy.

Investors now anticipate at least two interest rate hikes in 2026, abandoning earlier forecasts of a 40% chance of a rate cut. While French central bank chief François Villeroy de Galhau reaffirmed the ECB’s commitment to curbing energy-driven inflation, he cautioned that it was “too early” to specify the timing of any rate adjustments.

The offshore yuan edged higher to around 6.91 per dollar on Tuesday, extending modest gains from the previous session, supported by the unexpectedly strong return of expansion in PMI data. Official figures showed composite PMI rising to a three-month high of 50.5 in March 2026, signaling renewed growth across both sub-sectors.

The manufacturing PMI rose to a one-year high of 50.4, while the non-manufacturing PMI increased to 50.1, supported by government stimulus, strong holiday spending, and solid exports despite global supply chain disruptions and volatile energy markets. However, while the Chinese policymakers have repeatedly emphasized the need to pivot the economy toward domestic consumption and reduce reliance on external demand, geopolitical risks, such as the ongoing Middle East war, could weigh on business activity in the coming months. The yuan is still on track for a monthly decline, as the US dollar continues to benefit from safe-haven demand amid geopolitical turbulence.

DXY attracts some sellers following a modest Asian session rise to a fresh YTD top.

Trump is reportedly open to ending the war without reopening the Strait of Hormuz.

Inflation concerns and rising Fed rate hike bets should help limit losses for the USD.

The US Dollar Index (DXY), which tracks the Greenback against a basket of currencies, retreated from its highest level since May 2025, touched during the Asian session this Tuesday, snapping a five-day winning streak. The index, however, lacks follow-through selling amid contrasting headlines over peace talks to end the war in the Middle East and currently trades around the 100.40-100.45 region, down less than 0.10% for the day.

The Wall Street Journal reported on Monday that US President Donald Trump is willing to end the military campaign against Iran even if the Strait of Hormuz remains largely closed. The headlines trigger a turnaround in the global risk sentiment, which, in turn, is seen undermining the safe-haven USD. Furthermore, a corrective pullback in Crude Oil prices helps ease inflationary concerns and keep US Treasury bond yields on the defensive, turning out to be another factor weighing on the Greenback.

Meanwhile, Trump issued a stark warning that the US could launch massive strikes on Iran’s key energy infrastructure if a deal is not reached soon and if the Strait of Hormuz is not immediately reopened to commercial traffic. Moreover, Iran has signaled reluctance to engage in direct negotiations with the US, highlighting fragile diplomatic progress. Adding to this, the US is still deploying additional troops and assets to the region, fueling uncertainty about a quick de-escalation of tensions in the region.

This should act as a tailwind for Crude Oil prices, which keeps inflation risks and bets for a rate hike by the US Federal Reserve (Fed) in play. The hawkish outlook, in turn, should help limit deeper losses for the USD and warrants some caution before confirming that the index has topped out in the near term. Traders now look to the US economic data – JOLTS Job Openings and the Conference Board’s US Consumer Confidence Index, for a fresh impetus later during the North American session.

US Dollar Price Today

The table below shows the percentage change of US Dollar (USD) against listed major currencies today. US Dollar was the strongest against the New Zealand Dollar.

USD

EUR

GBP

JPY

CAD

AUD

NZD

CHF

USD

-0.06%

-0.14%

-0.03%

0.03%

-0.01%

0.03%

-0.12%

EUR

0.06%

-0.07%

0.05%

0.13%

0.08%

0.12%

-0.03%

GBP

0.14%

0.07%

0.13%

0.21%

0.16%

0.20%

0.05%

JPY

0.03%

-0.05%

-0.13%

0.06%

0.02%

0.05%

-0.08%

CAD

-0.03%

-0.13%

-0.21%

-0.06%

-0.04%

-0.00%

-0.15%

AUD

0.00%

-0.08%

-0.16%

-0.02%

0.04%

0.05%

-0.11%

NZD

-0.03%

-0.12%

-0.20%

-0.05%

0.00%

-0.05%

-0.16%

CHF

0.12%

0.03%

-0.05%

0.08%

0.15%

0.11%

0.16%

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the US Dollar from the left column and move along the horizontal line to the Japanese Yen, the percentage change displayed in the box will represent USD (base)/JPY (quote).

AUD/USD enters a bearish consolidation phase near a two-month low set on Monday.

The hawkish RBA Minutes and Iran de-escalation hopes offer some support to the pair.

The technical setup seems tilted in favor of bears and backs the case for deeper losses.

The AUD/USD pair seesaws between tepid gains/minor losses during the Asian session on Tuesday and consolidates its recent losses registered over the past week or so, to its lowest level in over two months, touched the previous day. Spot prices currently trade around mid-0.6800s, nearly unchanged for the day, amid mixed fundamental cues.

The Australian Dollar (AUD) draws some support from the hawkish Reserve Bank of Australia (RBA) meeting Minutes, showing that board members agreed further tightening would likely be needed. Adding to this, reviving hopes for a de-escalation of tensions in the Middle East boosts investors’ confidence, prompting a modest US Dollar (USD) pullback from the year-to-date and further benefiting the risk-sensitive AUD/USD pair.

From a technical perspective, spot prices find some support near the rising 100-day Simple Moving Average (SMA), around the 0.6820 area, which tempers the downside. However, the Moving Average Convergence Divergence (MACD) indicator stays below its signal line in negative territory, while the Relative Strength Index (RSI) slips toward 36, both reinforcing fading bullish momentum and favoring further corrective pressure.

The 100-day SMA is closely followed by the 38.2% Fibonacci retracement level of the November-March move higher, around the 0.6800 round figure, which should act as a key pivotal point for short-term traders. Some follow-through selling below the recent lows in the 0.6880–0.6850 region would turn the focus toward the 61.8% Fibo. level at 0.6713. A clear break under 0.6713 would open the path toward the 78.6% level at 0.6586 and signal a deeper fall.

On the flip side, the initial resistance emerges at the 50% retracement at 0.6803, now acting as a nearby pivot, with stronger resistance at the 38.2% Fibo. level at 0.6892. A sustained recovery above 0.6892 would expose the 23.6% retracement at 0.7003, where sellers previously capped advances. Nevertheless, the near-term bias is mildly bearish as the AUD/USD pair holds well below the 23.6% Fibo. retracement near the 0.7000 psychological mark.

(The technical analysis of this story was written with the help of an AI tool.)

🇦🇺 AUD / 🇨🇦 CAD — Australian Dollar / Canadian Dollar

🇪🇺 EUR / 🇯🇵 JPY — Euro / Japanese Yen

🇬🇧 GBP / 🇯🇵 JPY — British Pound / Japanese Yen

🇦🇺 AUD / 🇳🇿 NZD — Australian Dollar / New Zealand Dollar

🇪🇺 EUR / 🇬🇧 GBP — Euro / British Pound

🇪🇺 EUR / 🇦🇺 AUD — Euro / Australian Dollar

🇬🇧 GBP / 🇨🇦 CAD — British Pound / Canadian Dollar

🇪🇺 EUR / 🇨🇦 CAD — Euro / Canadian Dollar

Manage Consent

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.