China’s offshore yuan strengthened to around 6.78 per dollar on Friday, extending gains from the previous session to its strongest level in nearly three weeks after the People’s Bank of China signaled greater tolerance for currency appreciation. The central bank set the yuan’s daily reference rate at 6.7989 per dollar, stronger than Thursday’s fixing of 6.8036 and below the closely watched 6.80 threshold for the first time since 2023. A fixing below 6.80 per dollar is widely viewed by investors as an indication that authorities are not seeking to restrain the yuan’s recent appreciation. Attention is now turning to a packed slate of Chinese economic releases due next week, including trade data, second-quarter GDP, industrial production, retail sales, and the unemployment rate. The figures are expected to provide fresh insight into the strength of the economy and could shape expectations for the yuan’s near-term direction.

Yen Jumps on Intervention Fears

The Japanese yen strengthened past 161.5 per dollar on Friday, erasing all of its losses from earlier in the week as traders remained alert to the possibility of official intervention after the currency weakened to fresh 40-year lows. Market participants are now awaiting intervention data due later this month to determine whether Japanese authorities were behind the sharp but short-lived rallies seen in recent weeks. Investors also assessed data showing Japan’s producer prices climbed 7.1% in June, marking the fastest annual increase since March 2023 amid persistent cost pressures linked to the Middle East conflict and the yen’s sharp depreciation. Meanwhile, oil prices retreated after reports indicated that the US and Iran will continue peace negotiations despite a recent escalation in hostilities. That weighed on the dollar and Treasury yields while easing pressure on the yen by reducing import cost concerns for Japan, which depends heavily on Middle Eastern oil.

Australian Dollar Set for a Muted Week

The Australian dollar rose to around $0.695 but was on track to finish the week largely unchanged as investors monitored developments surrounding the Strait of Hormuz following renewed tensions in the Middle East. The safe-haven US dollar strengthened, while oil prices climbed after the US and Iran carried out military strikes in the Gulf earlier this week. However, both countries are now set to resume peace talks despite the recent escalation. Meanwhile, the International Monetary Fund lowered its 2026 growth forecast for Australia to 1.9% from 2.0% and warned inflation would remain elevated at around 4% this year. The Reserve Bank of Australia will meet in August and is expected to keep its cash rate unchanged at 4.35%, though markets still price in a roughly 60% chance of one final rate hike later this year, depending on the movement of oil prices. Traders also await key employment and inflation data due later this month, which could offer fresh clues on the policy outlook.

EUR/GBP Price Languishes below 0.8550 with bullish attempts subdued

- EUR/GBP treads water around 0.8530, a few pips above one-year lows, at 0.8519.

- German Trade Balance surplus beat expectations in May, yet with no impact on the Euro.

- Rising geopolitical tensions and higher Oil prices are keeping Euro bulls subdued.

The Euro (EUR) keeps treading water right above one-year lows against the British Pound (GBP) on Thursday. The EUR/GBP is trading flat in the area of 0.8530 at the time of writing, weighed by rising tensions between the US and Iran and the rebound in oil prices.

In the Eurozone, German Trade Balance data beat expectations with a EUR 19.1 billion surplus in May, from the 14.5 billion surplus seen in April, as exports grew against expectations. The data, however, has failed to provide any significant support to the Euro.

Meanwhile, the US has launched a new round of attacks in Iran, which targeted US bases in Gulf countries in retaliation. US President Donald Trump said on Wednesday that the ceasefire was over, and Crude prices have bounced up nearly10% with Brent Oil hitting the $80 level on Wednesday, after bottoming near $70.00 last week.

Technical Analysis: EUR/GBP bears have lost momentum

EUR/GBP shows a bearish near-term tone, although sellers seem to have lost momentum. The Relative Strength Index (14), now near 28, highlights a bullish divergence, while the Moving Average Convergence Divergence (MACD) indicator stabilizes around the zero line, hinting at consolidation rather than a decisive bullish reversal.

Bulls, however, must break above the previous yearly low, at 0.8533 (Jul 7 low), and the top of the descending wedge pattern from mid-June highs, now around 0.8555, to confirm a bullish correction.

On the downside, below the mentioned Wednesday’s low at 0.8519, the confluence of the wedge bottom and late June 2025 lows, just above 0.8500, is likely to test bulls. Further down, there is no clear support until the early June 2025 lows, in the area of 0.84100.8863.

Euro Price This week

The table below shows the percentage change of Euro (EUR) against listed major currencies this week. Euro was the strongest against the Japanese Yen.

| USD | EUR | GBP | JPY | CAD | AUD | NZD | CHF | |

|---|---|---|---|---|---|---|---|---|

| USD | 0.03% | -0.46% | 0.65% | -0.20% | -0.03% | -0.32% | 0.38% | |

| EUR | -0.03% | -0.51% | 0.61% | -0.26% | -0.03% | -0.39% | 0.30% | |

| GBP | 0.46% | 0.51% | 1.00% | 0.26% | 0.47% | 0.13% | 0.82% | |

| JPY | -0.65% | -0.61% | -1.00% | -0.87% | -0.55% | -0.93% | -0.28% | |

| CAD | 0.20% | 0.26% | -0.26% | 0.87% | 0.30% | -0.07% | 0.56% | |

| AUD | 0.03% | 0.03% | -0.47% | 0.55% | -0.30% | -0.36% | 0.33% | |

| NZD | 0.32% | 0.39% | -0.13% | 0.93% | 0.07% | 0.36% | 0.69% | |

| CHF | -0.38% | -0.30% | -0.82% | 0.28% | -0.56% | -0.33% | -0.69% |

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the Euro from the left column and move along the horizontal line to the US Dollar, the percentage change displayed in the box will represent EUR (base)/USD (quote).

AUD/JPY Price Weakens to near 112.50, but uptrend remains constructive

- AUD/JPY weakens to near 112.62 in Thursday’s early European session.

- The cross keeps a constructive bullish bias, but further consolidation cannot be ruled out with neutral RSI momentum.

- The initial support level is located at 112.55; the immediate resistance level to watch is 113.55.

The AUD/JPY cross trades in negative territory around 112.62 during the early European trading hours on Thursday. The Japanese Yen (JPY) edges higher against the Australian Dollar (AUD) amid escalating tensions in the Middle East after US President Donald Trump said an interim agreement to end the war with Iran was “over.”

Traders are also on high alert for possible intervention from Japanese officials. “The yen’s current weakness is excessive and fails to reflect the strong fundamentals of the Japanese economy, a misalignment that could prompt major central banks to launch coordinated intervention,” said Michael Nizard, head of multi-asset and overlay at Edmond de Rothschild Asset Management.

Technical Analysis:

In the daily chart, AUD/JPY holds above the 100-day moving average (MA) and the Bollinger Bands’ 20-day simple moving average (SMA), which together suggest a constructive bullish bias after the recent pullback. Price also remains comfortably above the lower Bollinger band, while the upper band marks the next upside objective as the pair grinds higher; the Relative Strength Index (14) near 50 keeps momentum neutral, hinting at consolidation rather than exhaustion for now.

On the downside, initial support is seen at the 100-day MA at 112.55, followed by the Bollinger midline around 112.42 and then the lower band at 111.15, where buyers would likely defend the broader uptrend. On the other hand, the first upside barrier emerges at the June 16 high of 113.55. The next hurdle is seen at the upper Bollinger band at 113.70, en route to the May 13 high of 114.74.

GBP/USD Price – Holds a constructive bullish tone above 1.3400 as UK political risk eases

- GBP/USD gathers strength to near 1.3405 in Thursday’s early European session.

- The pair maintains constructive bias, with a mildly bullish RSI momentum.

- The first upside barrier emerges at 1.3470; the initial support level to watch is 1.3300.

The GBP/USD pair trades in positive territory around 1.3405 during the early European trading hours on Thursday. Fading political uncertainty in the United Kingdom (UK) provides some support to the British Pound (GBP) against the US Dollar (USD).

Following the resignation of Keir Starmer in late June, UK political risk has eased significantly. The formal race to replace outgoing Prime Minister Keir Starmer begins on July 9. Frontrunner Andy Burnham is widely expected to become Prime Minister by July 20.

Technical Analysis:

In the daily chart, GBP/USD holds a mildly bullish near-term bias as price sits above the Bollinger middle band and the 100-day simple moving average (SMA). The pair is pressing the upper half of the recent range, with the Bollinger Bands (20, 2) still widening modestly, while the Relative Strength Index (14) at 57.6 suggests constructive but not overextended upside momentum.

On the topside, initial resistance is aligned with the Bollinger upper band at 1.3470, where buyers could hesitate. On the downside, immediate support is provided by the Bollinger middle band near 1.3300, while a deeper pullback would likely be contained by the Bollinger lower band around 1.3130.

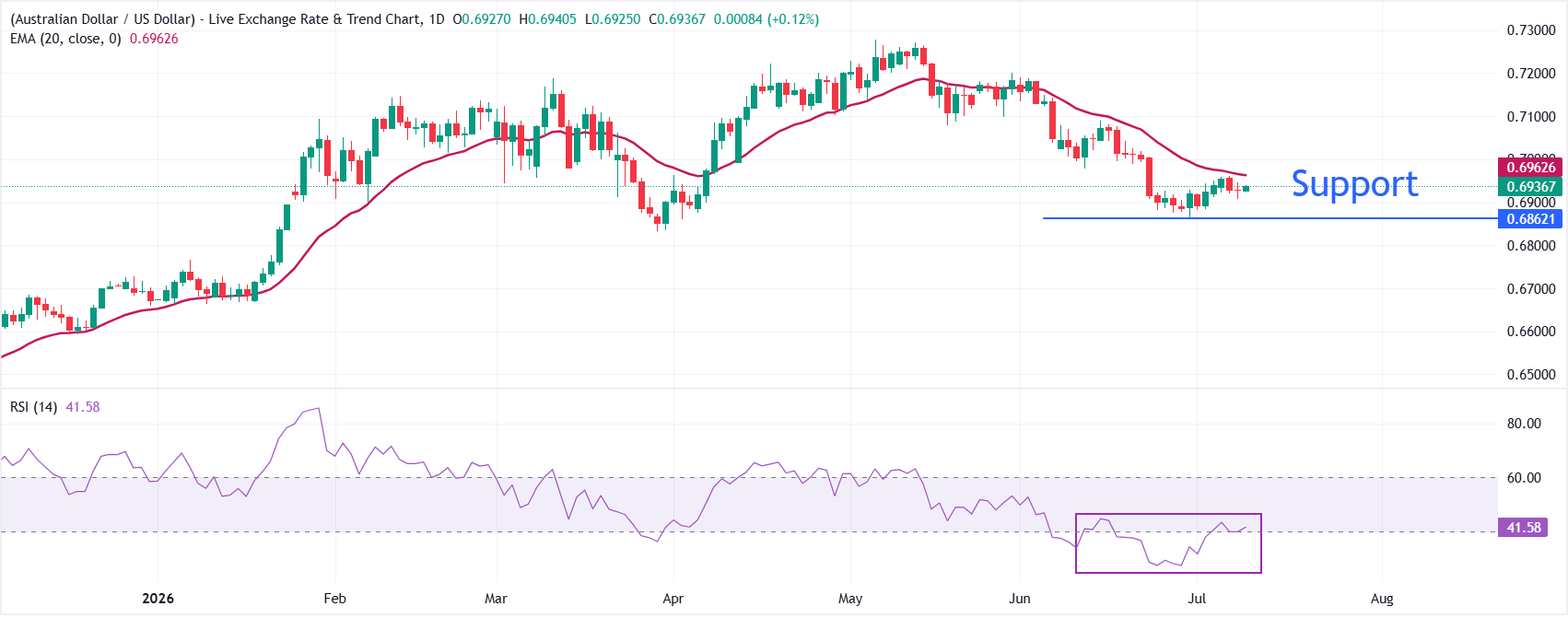

AUD/USD Price – 0.6860 is key support level amid geopolitical risks

- The Australian Dollar edges up against the US Dollar despite multiple headwinds.

- Middle East war may last longer due to US attacks on Iranian infrastructure.

- The FOMC minutes show that several policymakers see the need for monetary policy tightening.

The Australian Dollar (AUD) trades marginally higher at around 0.6935 against the US Dollar (USD) during the European trading session on Thursday. The Aussie pair edges up as the US Dollar ticks lower despite escalating Middle East risks and hawkish Federal Open Market Committee (FOMC) Minutes of the June policy meeting.

At press time, the US Dollar Index (DXY), which gauges the Greenback’s value against six major currencies, trades 0.13% lower to near 100.92.

The attacks on Iranian infrastructure by United States (US) military forces signal that the restart of the war would last long, a scenario that might keep oil prices higher and the appeal of safe-haven assets upbeat. According to Axios, the US Air Force bombed two railway bridges in Iran on Wednesday.

Meanwhile, the FOMC Minutes showed on Wednesday that policymakers are concerned about upside inflation risks and several of them see the need to tighten monetary conditions to ease price pressures.

In the Australian region, traders might consider raising hawkish Reserve Bank of Australia (RBA) bets again as Assistant Governor Sarah Hunter has reiterated that the central bank would act, if needed, for inflation to return to target and maintain sustainable full employment.

Lately, traders pared hawkish RBA bets as the Australian monthly Consumer Price Index (CPI) has cooled down in the last two months.

AUD/USD technical analysis

AUD/USD trades slightly higher at around 0.6936, but maintains a bearish near-term tone as it remains below the 20-period exponential moving average (EMA) at 0.6963.

The pair has been unable to reclaim this short-term trend proxy, suggesting that rallies are likely to be capped while price holds under the EMA. The Relative Strength Index (RSI) at 41.46 stays below the midline, hinting at persistent, though not extreme, selling pressure.

On the topside, initial resistance is defined by the 20-period EMA at 0.6963, which is the first level bulls would need to overcome to ease the current downside bias. Above the moving average, the next resistance for the pair will be the psychological level of 0.7000. Looking down, the June low at 0.6865 is the key support level; a break below that would expose the pair to the March low at 0.6833.