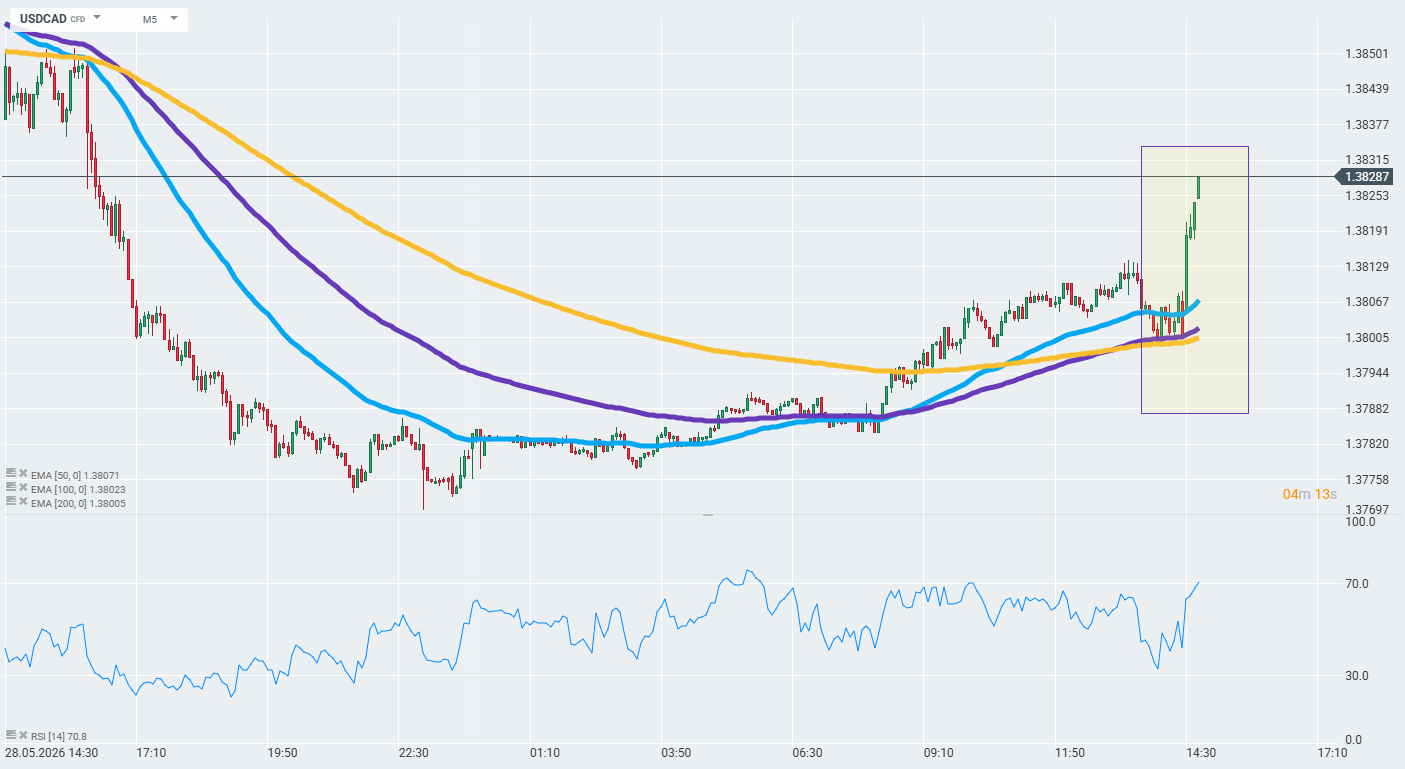

- USD/CHF rises as the Swiss Franc weakens ahead of key Swiss Retail, GDP, and PMI data.

- The US Dollar strengthens on safe-haven demand as investors closely monitor fluid US-Iran peace negotiations.

- Geopolitical uncertainty intensified after Israel ordered its troops to advance further into Lebanon.

USD/CHF gains ground after two days of losses, trading around 0.7830 during the Asian hours on Monday. The pair gains ground as the Swiss Franc (CHF) weakens ahead of the release of key economic data including, Swiss Real Retail Sales for April, Q1 Gross Domestic Product, and May’s SVME – Purchasing Managers’ Index (PMI). Traders will shift their focus on the Institute for Supply Management’s (ISM) Manufacturing PMI, which provides a reliable outlook on the state of the US manufacturing sector.

The USD/CHF pair appreciates as the US Dollar (USD) maintains its strength on increased safe-haven demand, driven by market participants closely assessing the highly fluid developments surrounding United States (US)-Iran peace negotiations.

US President Donald Trump seeks to alter and reinforce several key terms of the proposal aimed at ending the US-Israel war on Iran. According to the BBC, these requested changes specifically target regulations surrounding the strategic Strait of Hormuz and the mandatory removal of highly enriched uranium.

Axios further reported that Trump wants to tighten multiple points of the deal he deems critical, particularly the handling and disposal of Iran’s nuclear material. A senior US official noted that Trump has been briefed that a formal response from Iran regarding these adjusted terms could take up to three days.

The geopolitical uncertainty continues to increase after Israel has ordered its troops to advance further into Lebanon, marking a tactical escalation in its conflict with the Iran-backed militant group Hezbollah. The military push comes despite a ceasefire agreement announced more than six weeks ago, severely threatening to unravel earlier diplomatic progress.