The GBP/USD rate is rebounding slightly as the dollar (specifically the dollar index, USDIDX) corrects across the broader market after breaking out to a 13-month high. Technically, however, we are far from breaking the downward trend on GBPUSD. Even after the recent bounce, the price has been moving below the 10-day exponential moving average (EMA10; yellow) for 9 days. Furthermore, the cascade of the remaining EMAs (longer over shorter: EMA100 over EMA30, and EMA30 over EMA10) signals a clear downtrend, the reversal of which would require a series of bullish turnarounds. The chances of a strictly pro-pound turnaround remain slim. The British currency is primarily weighed down by a period of political uncertainty and the ongoing leadership transition within the ruling Labour Party following Prime Minister Starmer’s resignation.

The Guardian reported that according to preliminary internal party plans, Burnham could assume the office of Prime Minister as early as July 17. However, the anticipation—especially regarding the appointments of key cabinet members such as the Chancellor—should continue to test the pound. On the dollar side, we see a persistently hawkish Fed narrative, an increase in core PCE inflation to 3.4%, and a Q1 2026 GDP revision from 1.6% to 2.1%. The backdrop of a gathering momentum in the US economy alongside elevated inflation contrasts sharply with stagflationary tendencies in the UK. This divergence should extend the current trend on GBPUSD and the UK/US 10-year bond yield spread, until potential wage effects emerge from the recent UK energy shock, which could force the Bank of England into a more hawkish monetary policy stance. However, UK policy is already restrictive, which limits the potential for a sharp pivot.

Methodology

This recommendation was prepared based on a technical analysis of the GBPUSD chart and a fundamental analysis of the economies in question (monetary policy in the United Kingdom and the United States). The directional bias of the recommendation was determined using moving averages and market expectations regarding central bank policies. Take Profit and Stop Loss levels were established using Fibonacci retracements and price action:

TP1 and TP2 are located at the nearest support levels from November 2025.

SL is placed halfway between the EMA10 and EMA30, as well as between the 23.6% and 38.2% Fibo levels.

In mid-2026, the attention of financial markets is focused on the de-escalation of the situation in the Middle East and the race for dominance in the artificial intelligence sector, although at the same time, there is more and more talk about a bubble rather than further development. Parallelly, however, a climatic phenomenon is developing in the equatorial belt of the Pacific Ocean that has the potential to destabilize global supply chains, hit the production of key commodities, and trigger another wave of food inflation. Meteorological data from mid-2026 indicates a rapid transition of the ocean from a neutral phase to an active El Niño.

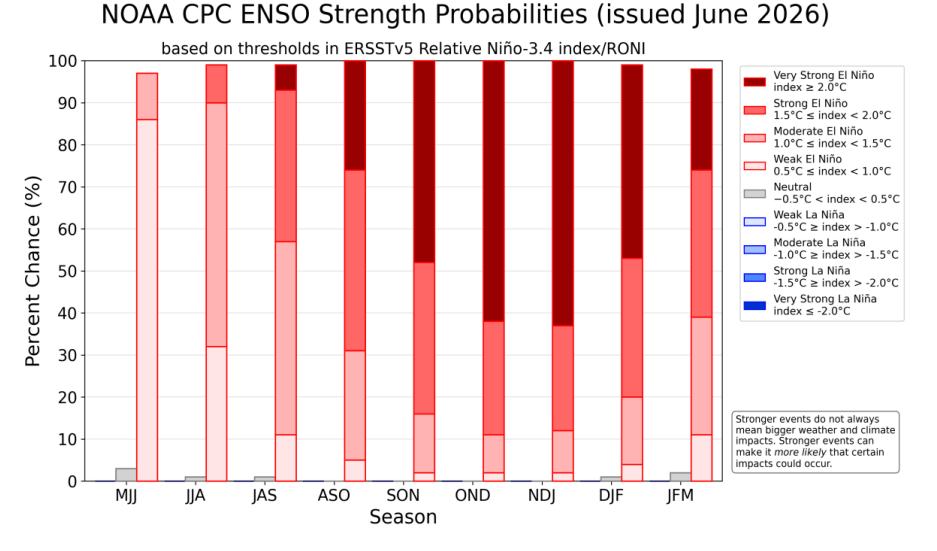

Forecasts from the American Climate Prediction Center (CPC) and the World Meteorological Organization (WMO) set the probability of this phenomenon transforming into a so-called Super El Niño before the end of the year at a level of 60% to 67%. If these forecasts materialize, the upcoming episode from the turn of 2026 and 2027 could become one of the strongest thermal anomalies recorded since 1950. How, then, should one react in market terms?

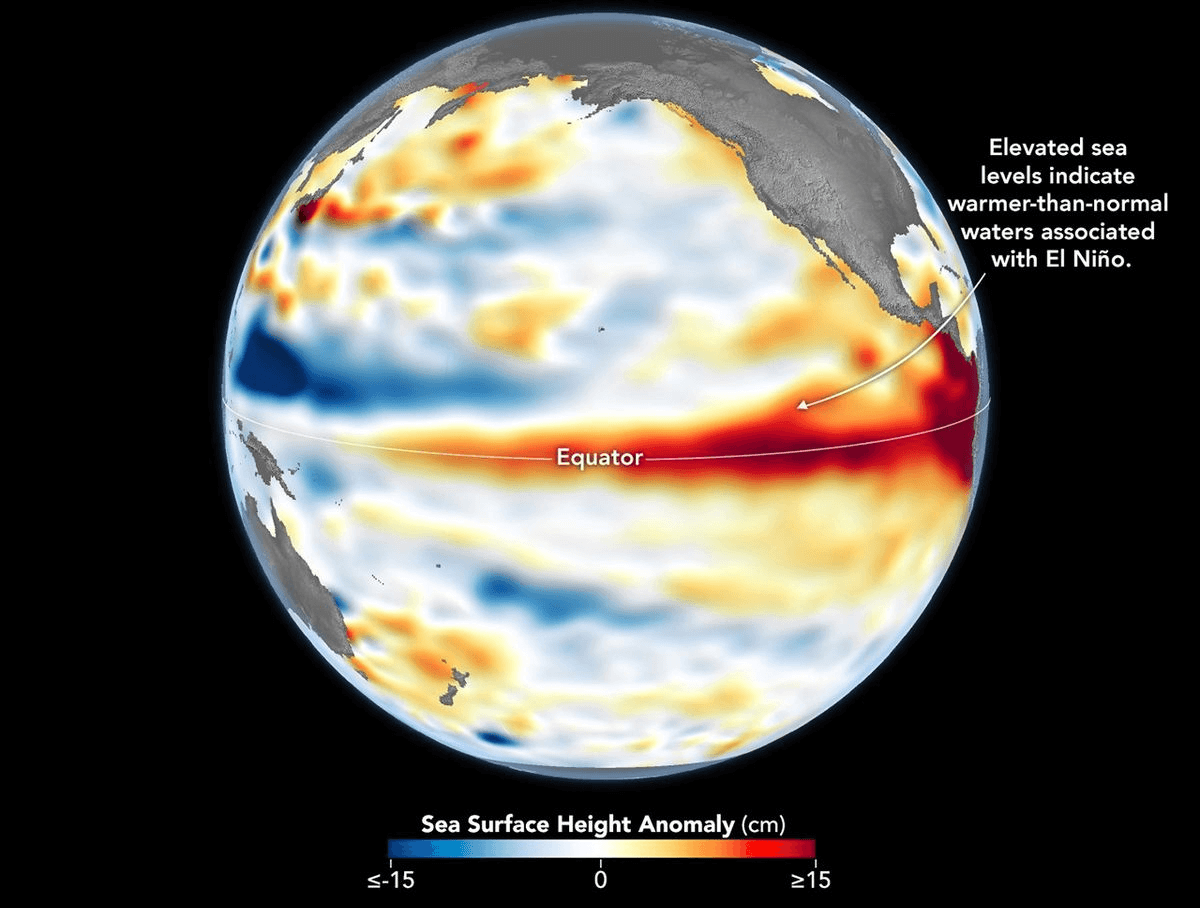

Graphic representing the height of the Pacific surface, which also coincides with water temperatures. Source: NASA

NOAA predicts over 60% probability of a Super El Niño occurring at the turn of 2026 and 2027. Source: NOAA

Physics and Climatology of ENSO: From Walker Circulation to the Implementation of the RONI IndexNormal Situation

Understanding the economic mechanism of El Niño requires an analysis of the physical processes occurring in the atmosphere and hydrosphere of the Pacific. Under neutral conditions, constant winds, called trade winds, blow from east to west, pushing sun-warmed surface waters toward Southeast Asia and Indonesia. This causes a physical accumulation of water off the coast of Asia, where the sea level is about 0.5 meters higher than off the coast of South America. Simultaneously, intense upwelling occurs off the coast of Peru and Ecuador, which is the rising of cold, oxygen- and nutrient-rich waters from the ocean floor, fueling local ecosystems and allowing for massive fish catches.

El Nino

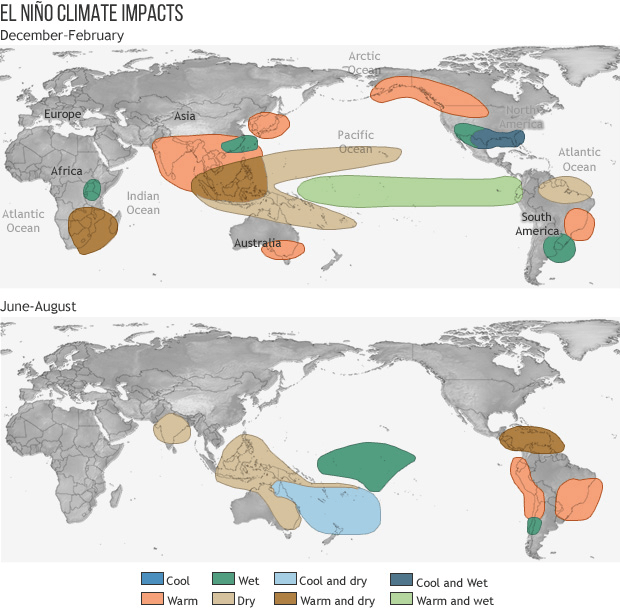

During the El Niño phase, the trade winds weaken, and sometimes even reverse their direction. Warm water accumulated in the west begins to spill back to the east, raising the sea surface temperature off the coast of South America by 1 to even 3 degrees Celsius, although most often 2 degrees are already treated as a very serious disturbance to the entire ecosystem. This process completely flattens the thermocline and blocks the pushing of cold water to the surface. The resulting giant “heater” releases thermal energy into the atmosphere, which disrupts the Walker circulation, shifts storm tracks, triggers heavy rains in South America, and catastrophic droughts in Asia and Australia, partially also affecting the situation across the globe, including Africa, which is key in the case of cocoa crops.

Weather conditions during El Niño. Source: NOAA

How to measure El Niño?

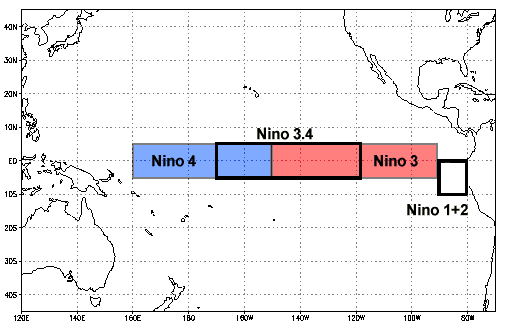

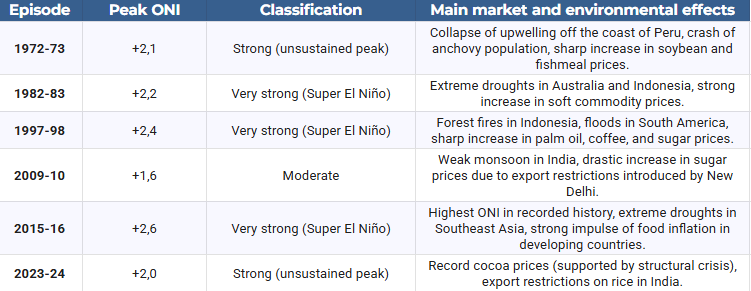

The traditional tool used to measure the strength of ENSO is the ONI (Oceanic Niño Index), calculated as a three-month moving average of sea surface temperature (SST) anomalies in the key Niño 3.4 region. A threshold of +0.5 signifies the formal occurrence of El Niño, a threshold of +1.5 defines a strong episode, and from the value of +2.0, the very strong zone begins, i.e., Super El Niño.

Key location where the El Niño phenomenon forms. Source: NOAA

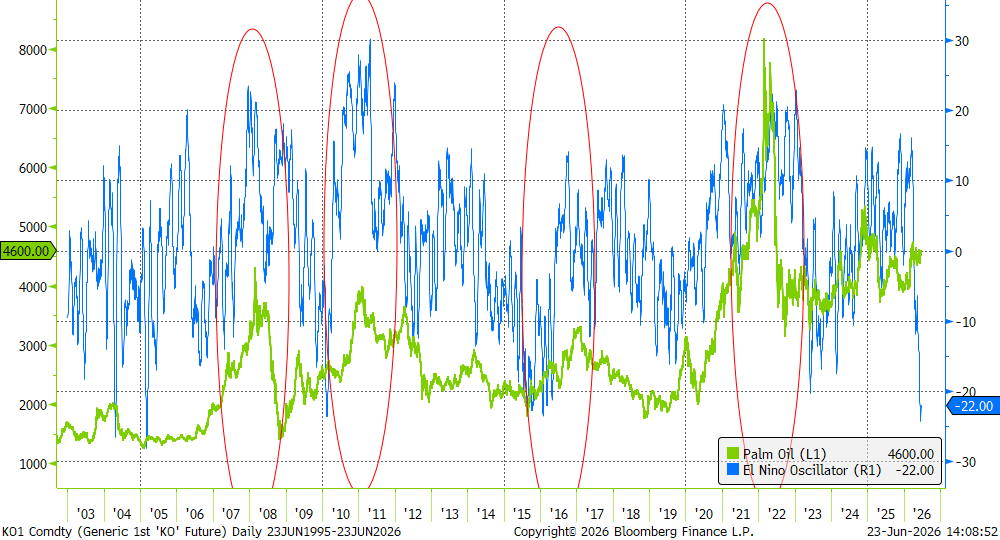

El Niño Oscillator index and palm oil prices. As can be seen, the index is currently clearly negative, indicating the absence of the phenomenon. However, this is usually a prelude to a later, stronger hit. Source: Bloomberg Finance LP Modern global warming significantly complicates the interpretation of ONI results. Record hot oceans worldwide mean that traditional indicators give misleading, inflated readings.

For example, the episode from 2023–2024 peaked according to the old methodology at +2.0, but due to a lack of stability in the anomaly, it was classified only as “strong.” For this reason, meteorological agencies in Australia (BOM), the USA (NOAA), and New Zealand implemented a new indicator – RONI (Relative Oceanic Niño Index). This index dynamically filters out the general planetary warming trend from the real, cyclic anomaly of the Pacific. It is RONI that confirms in mid-2026 that the approaching phenomenon is developing extremely fast, moving from a neutral phase into a strong strike. For comparison purposes, the table below presents the classification of historical episodes according to their maximum intensity measured by the ONI index.

Source: own study based on NOAA

Impact on GDP and the Role of the “Conflict Multiplier”

The relationship between climate physics and financial markets has been precisely described in economic research, including those published by the European Central Bank (ECB). A strong El Niño phenomenon raises global prices for non-energy commodities (agricultural goods and metals) by an average of about 5%. Crucially for monetary policy, this effect persists in markets for 6 to even 16 months after the weather shock itself. This anomaly does not affect all economies in the same way, creating drastic discrepancies in GDP dynamics:

Indonesia: Records an average GDP drop of 1% due to paralyzing droughts destroying agriculture and limiting coal and nickel mining.

United States: Gains about 0.5% of GDP (which translates to over 150 billion dollars) thanks to milder winters in the north and more favorable rainfall in the agricultural belt in the south (lower gas consumption, higher yields).

Thailand: May record a GDP growth of almost 1%, provided there is appropriate water resource management in agriculture.

On a global scale, the balance is decidedly negative. Losses resulting from lost productivity were estimated at nearly 5.7 trillion dollars for the 1997–1998 episode and over 7.8 trillion dollars for the phenomenon of 2015–2016. In mid-2026, the global economy is exceptionally vulnerable to these types of shocks due to elevated core inflation, shipping restrictions, and energy costs driven up by a previous conflict in Iran. The USDA forecasts a 4.7% increase in food prices in the USA in 2026, and for products based on sugar and cocoa, it indicates an increase of up to 8.4%. For this reason, the FAO and WFP launched a joint appeal for 202 million dollars for preventive actions in 22 priority countries.

Parallelly, drought caused by El Niño acts as a factor creating conflict. Model studies conducted by Bloomberg Economics indicate that a drastic drop in rainfall and loss of income from agriculture exacerbate competition for shrinking natural resources. Countries with low GDP per capita, high corruption, and weak institutions are particularly sensitive to this mechanism. Myanmar, Pakistan, and Nigeria are identified as countries with the highest risk of outbreaks or escalation of internal conflict in 2026. Conversely, in Latin America (Mexico, Colombia, Brazil), a prolonged lack of rainfall could overlap with existing tensions and escalate violence from drug cartels controlling water resources and rural territories.

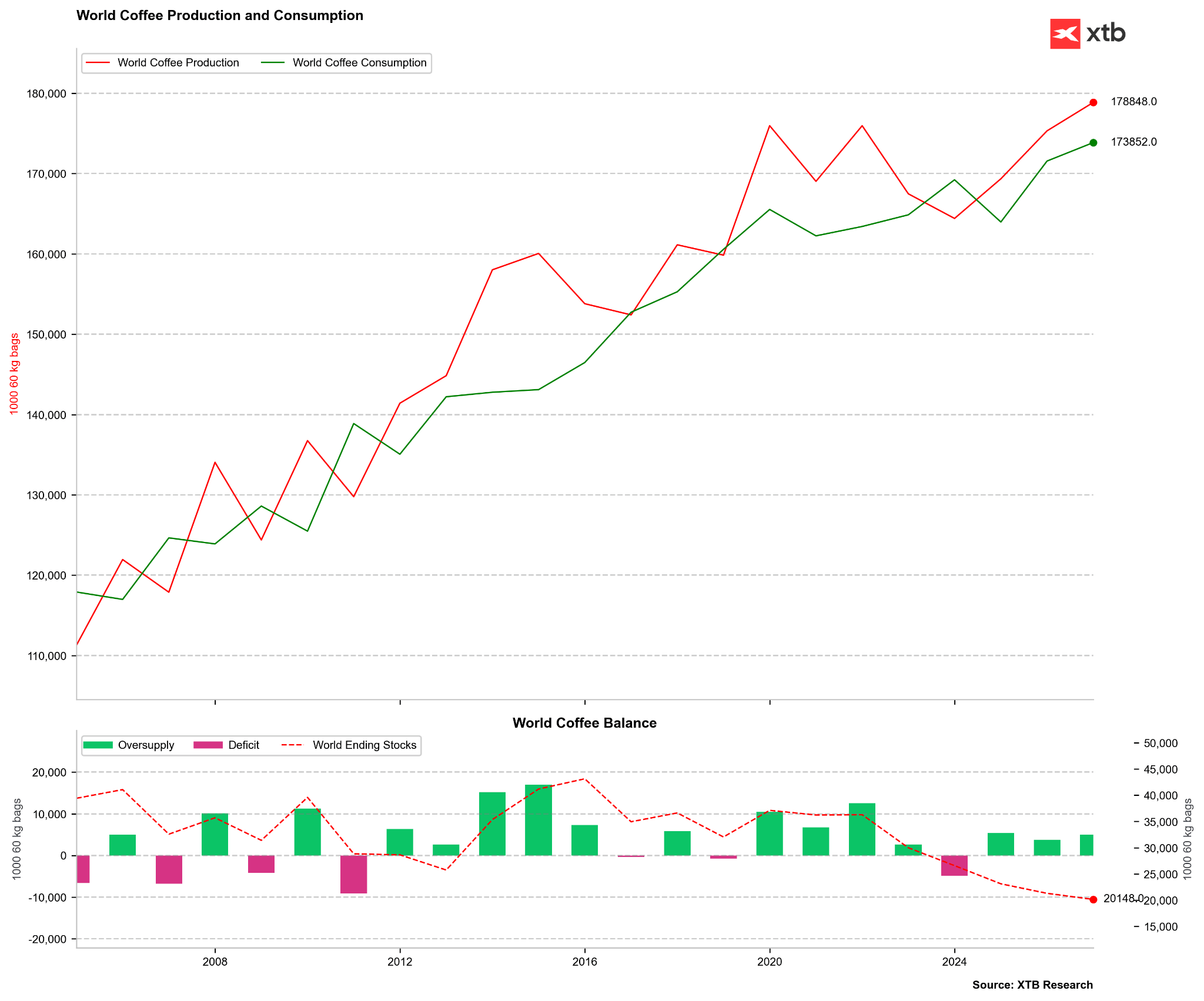

El Niño and Key Soft Commodity Markets: Coffee and Cocoa

The coffee and cocoa markets are considered litmus tests for the strength of El Niño due to the geographical concentration of crops in the equatorial zone. In the years 2026–2027, this phenomenon overlaps with previous structural shortages, triggering powerful reshuffles in the pricing of futures contracts.

Cocoa: Threat to Main Harvests in West Africa and Disease Crisis in Ecuador

A popular market narrative assumes the simplification that El Niño means drought in West Africa, which will translate into an uncontrolled increase in cocoa prices. The reality, however, is more complex because the direct ENSO climate signal for Côte d’Ivoire and Ghana (accounting for nearly 60% of global supply) is weaker than for Asia. The historical price record from 2023–2024 resulted mainly from structural problems: a fertilizer crisis caused by war, a lack of investment in tree rejuvenation, and destructive Harmattan winds. In the second half of 2026, markets fear the superimposition of these structural weaknesses on weather anomalies. Three factors determine the current, pro-growth positioning of capital:

Weak fruit setting: Early surveys on plantations in West Africa point to extremely low setting of young fruits (cherelles) for the 2026/2027 season, which heralds poor main harvests starting in October.

Revision of the commodity balance: StoneX drastically cut its global cocoa surplus forecast for the 2026/2027 season to just 149,000 tons (compared to an estimated 267,000 tons in January). Conversely, Citigroup predicts a deep deficit of 56,000 tons in the 2026/2027 season. On the other hand, forecasts appeared that the current season might end with an oversupply as high as 400,000 tons, mainly due to weak demand.

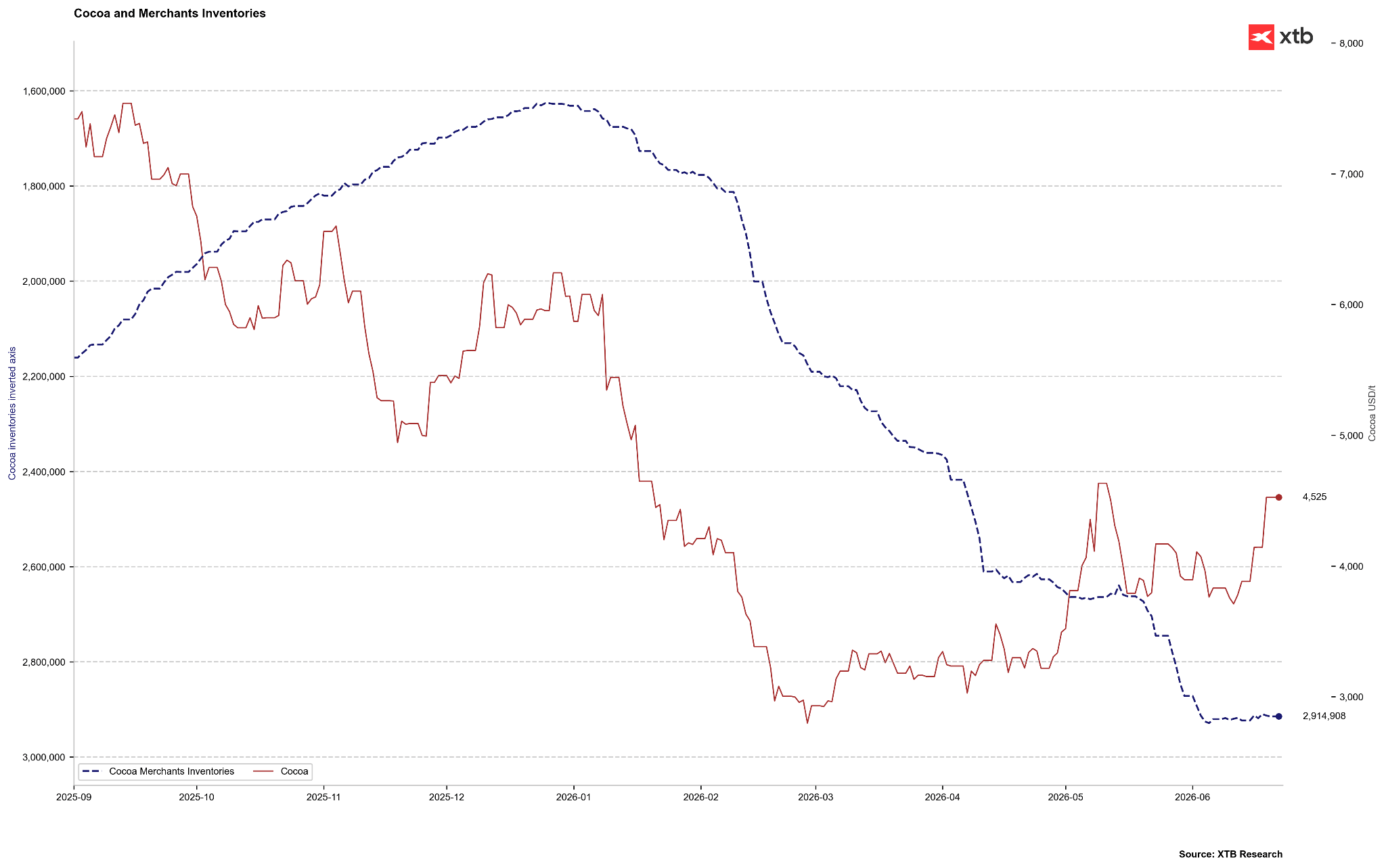

Demand destruction as a brake: A bearish counterweight is the high ICE-certified stocks (reaching nearly 2.9 million bags in June 2026) and a clear drop in cocoa processing (grinding) in Europe (down 7.8% year-on-year in the first quarter of 2026 – the lowest reading in 17 years) and North America (down 3.8% year-on-year).

Cocoa stocks are at their highest in several years, though it is worth remembering that in 2023-2024 there was a massive contraction in stocks. We are now theoretically at the seasonal peak. If stocks start to grow, however, it could mean the scale of oversupply is larger than expected. Source: Bloomberg Finance LP, XTB

Despite weakening demand in developed countries, Citigroup predicts that due to Super El Niño, cocoa prices will permanently exceed the level of 5,000 dollars per ton in the next three months, with the potential to reach 6,000 dollars per ton on a 12-month horizon. An additional catalyst for increases is the situation in Ecuador (the world’s third-largest producer). El Niño brings heavy rains and floods there. Extreme humidity in the period from December 2026 to February 2027 creates ideal conditions for the spread of fungal diseases (such as moniliasis or black pod rot), which directly destroys crops and prevents traditional sun-drying of harvested beans. Ecuador recently aspired to second place in terms of production, but due to its own problems, it will likely remain in third place, just behind Ghana.

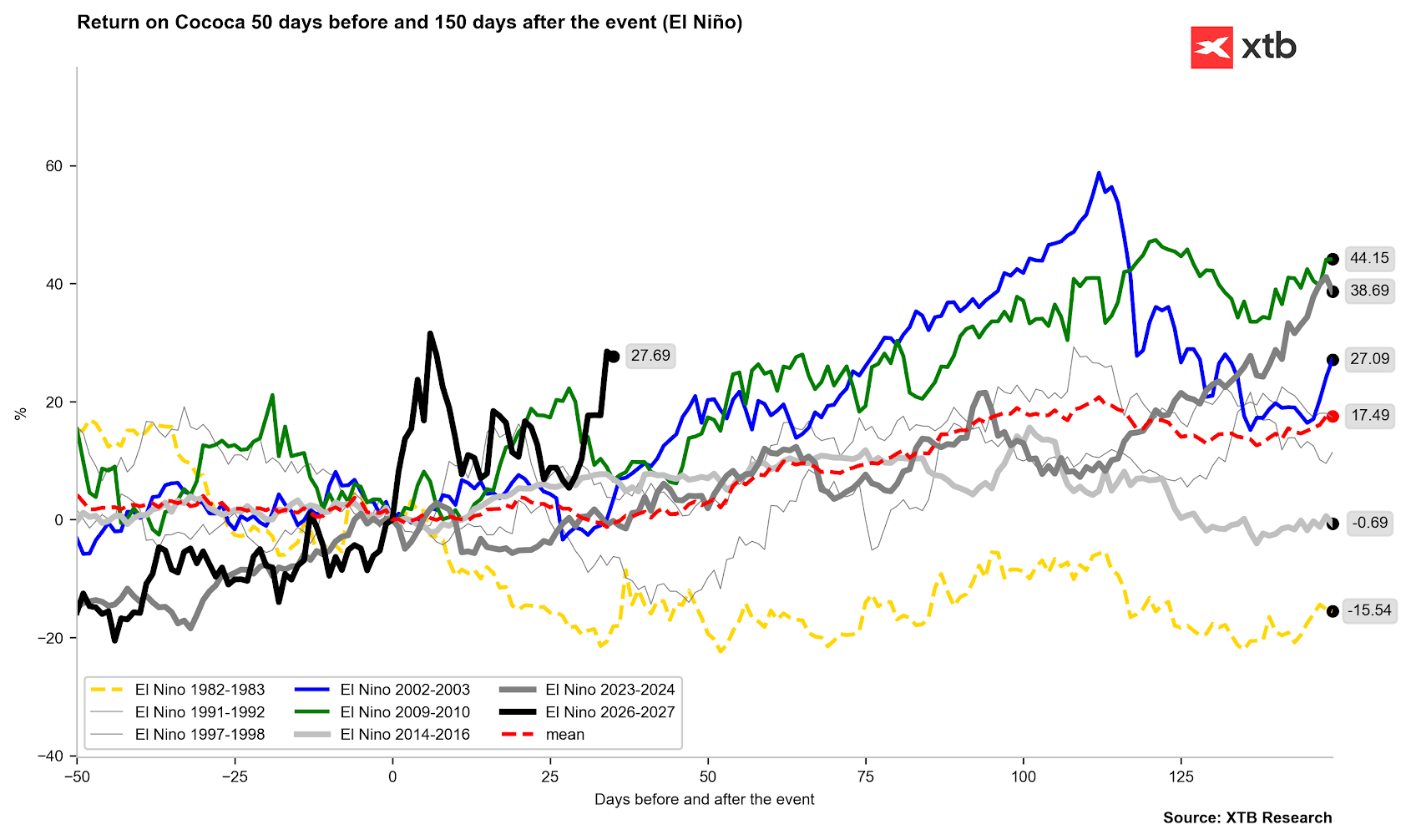

Most El Niño periods ended with clear price increases. What’s more, the impact of El Niño from 2023 still reached strongly into 2024. Source: Bloomberg Finance LP, XTB

Coffee: Extreme Drought for Robusta and Vegetative Anomalies for Arabica

In the coffee market, the El Niño phenomenon triggers starkly different reactions depending on the species and growing region:

Robusta (Vietnam, Indonesia): Southeast Asia accounts for about 50% of global Robusta production. El Niño brings extreme heatwaves and droughts to these areas, which drastically lowers yields. Although Vietnamese exports in the period of January-May 2026 increased by 7.9% year-on-year, the upcoming lack of rainfall creates a high risk of a drastic supply shortage in the next several months, which is already pushing Robusta futures contracts to multi-month highs.

Arabica (Brazil): El Niño initially brings excessive rains in Brazil. In the short term, this complicates and delays harvesting (by mid-June 2026, only 15.8% of crops were harvested compared to 26.6% in the same period of 2024). Although the USDA forecasts record Brazilian harvests at 71.9 million bags (up 14% year-on-year), rains deteriorate the quality of harvested beans and stimulate premature flowering of coffee trees before the harvest is complete, which threatens bud dropping and damage to production potential for the 2027/2028 season. There is also a high risk that heavy rains will give way to a severe drought in key growing regions in September and October 2026, which will prevent proper flowering and trigger a sharp rise in Arabica prices.

USDA data for several years has shown an oversupply, but this does not always coincide with the narrative from other institutions, particularly the Brazilian CONAB. Source: Bloomberg Finance LP

Market Paradoxes and Energy-Industrial Commodities

The impact of El Niño on commodity markets abounds in anomalies that defy the intuition of inexperienced market participants:

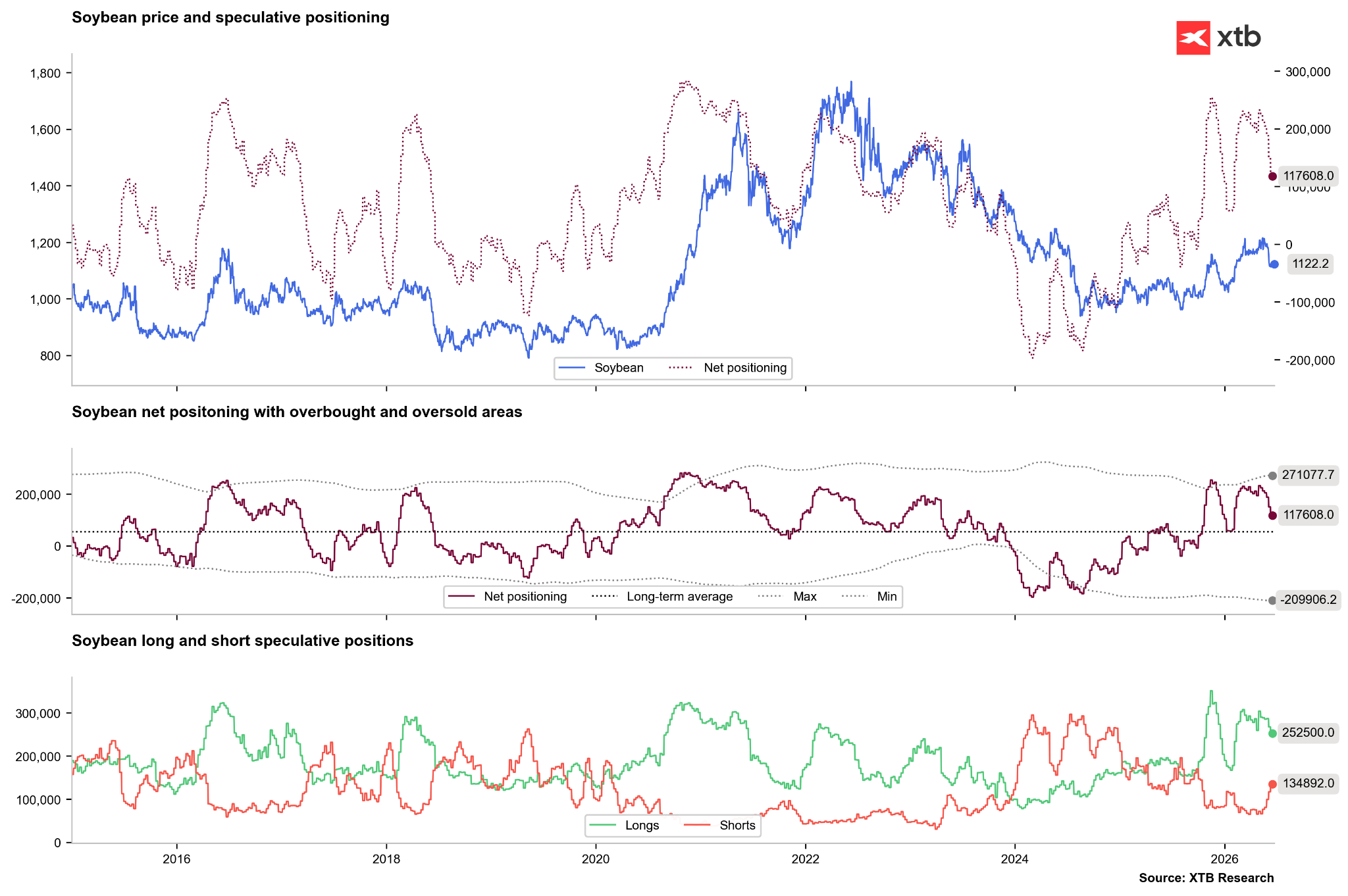

Soybeans as a beneficiary of rainfall: While most crops are destroyed, soybeans are a structural beneficiary of El Niño. This phenomenon brings abundant rainfall to the US growing belt, in Argentina, and in southern Brazil. Historically, this translates into yield increases of 10% to 15% above the trend, generating global oversupply and triggering sharp price drops on the Chicago exchanges.

Bearish pressure on American natural gas: El Niño brings milder and warmer winters to the northern United States. This results in a drastic drop in demand for gas for home heating, exerting strong downward pressure on the commodity’s price (bear market) in the USA, which stands in contradiction to the general trend of rising commodity prices.

Hydroelectric crisis in China: Chinese electricity demand in 2026 is growing by 5% year-on-year, driven by the development of AI data centers and EV charging. The drought caused by El Niño drastically limits production from Chinese hydroelectric plants. Consequently, local governments are forced to substitute hydro energy with coal and gas generation. Beijing issued a categorical decree ordering power plants to rebuild coal stocks to a level covering a minimum of 20 days of consumption, which stimulates price increases for thermal coal.

Copper logistics paralysis in Chile and Peru: South America in copper mining zones experiences heavy rains and floods. This leads to the washing out of transport roads, flooding of mine infrastructure, deficits in local hydro energy, and mudslides. The supply restriction from these two key countries constitutes a strong upward impulse for copper prices on the LME.

Investors are starting to position for a soybean production surplus. The number of longs is clearly being reduced, while the number of shorts is rising. Source: Bloomberg Finance LP, XTB

Guide to Listed Companies: Winners and Losers of Super El Niño

For stock market investors, Super El Niño constitutes a significant capital allocation factor. The following discussion presents companies that may see improvement in financial results, and those that are exposed to serious operational and financial risks.

Fertilizer and Crop Protection Sector

Weather anomalies and falling yields force farmers to intensify fertilization and protection of surviving crops to save revenues, which supports producers of agricultural production inputs.

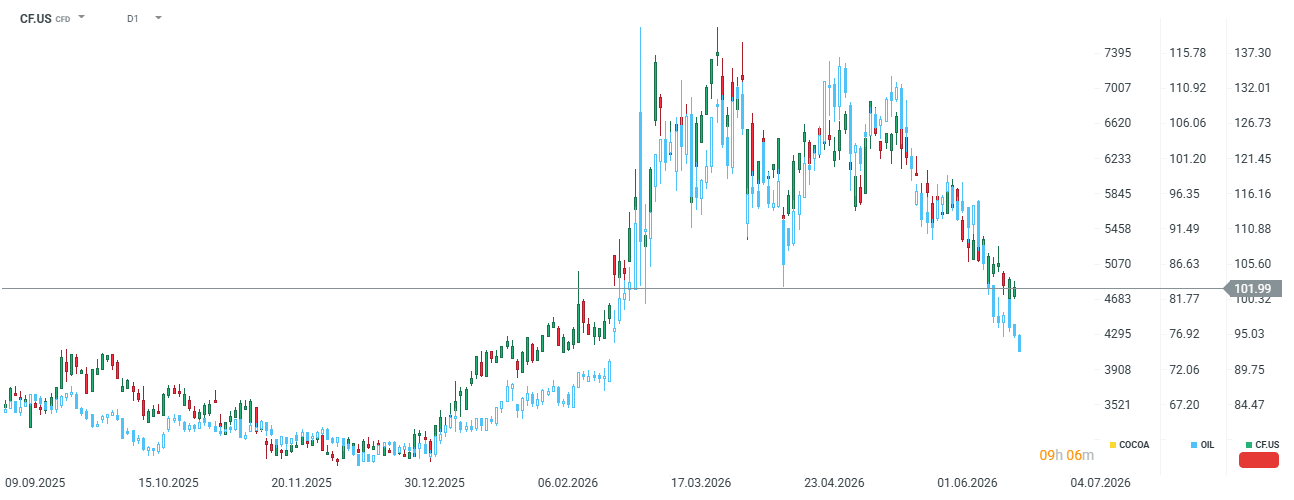

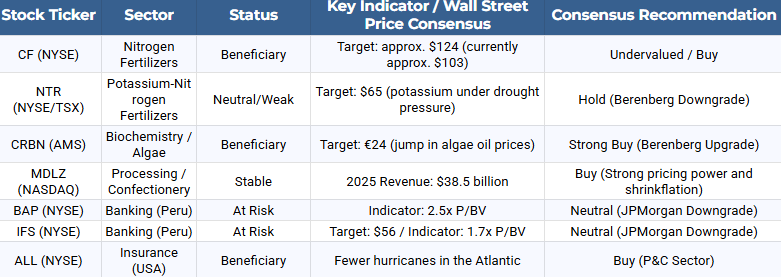

CF Industries Holdings Inc. (CF): The company focuses on nitrogen fertilizers. In mid-2026, its valuation fluctuates around 102 dollars (about 19% below the analyst consensus of 124 dollars). CF Industries benefits from cheap gas in the USA (the main raw material for ammonia production), maintaining a high EBITDA margin while European competitors struggle with more expensive raw materials. An additional long-term factor is the implementation of the 3.7 billion dollar Blue Point project in the low-emission ammonia segment.

The company gained significantly in value during the crisis related to the Strait of Hormuz. It may turn out that fertilizers will again come under upward pressure. Source: xStation5

Nutrien Ltd. (NTR): The company shows a more nuanced risk profile. It has strong nitrogen exposure, but droughts caused by El Niño drastically delay farmer demand for potash, leading Berenberg to downgrade NTR to “Hold” with a target price of 65 dollars. The company offers a stable dividend yield of 3.4%, but its growth potential in 2026 is limited by the fall in potash prices. Currently, shares are trading around 61 USD.

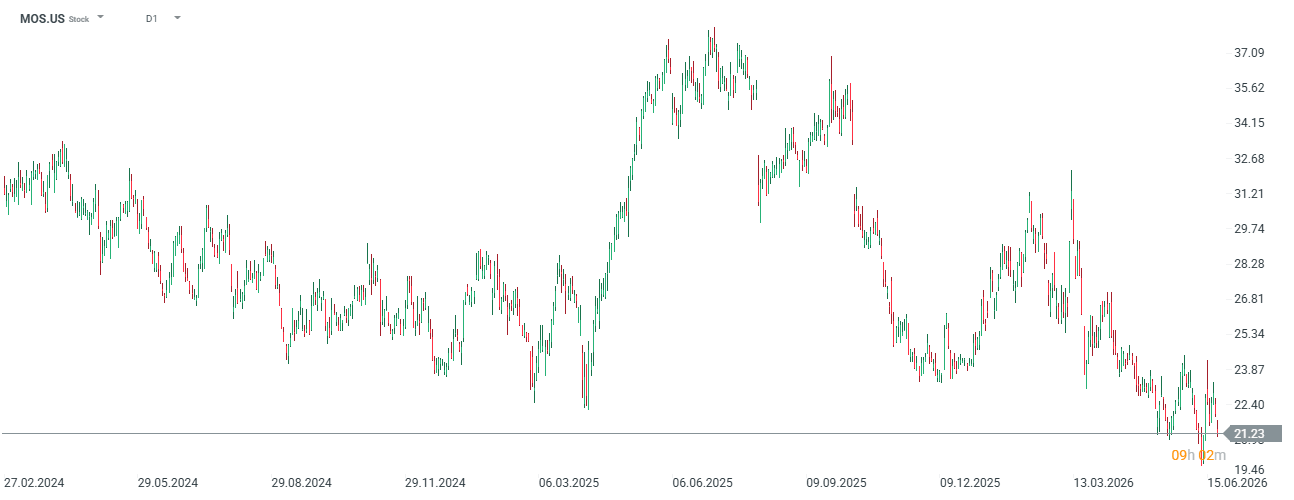

The Mosaic Co. (MOS): The company is heavily dependent on potash sales, which in drought conditions weakening demand for this nutrient puts it in a worse market position. The company is currently at multi-year lows, around 21 USD, but in 2025 it traded as high as 37 USD.

Corteva Inc. (CTVA): As a global provider of advanced seeds and chemical crop protection, it may see revenue growth as farmers pay a premium for drought- and pathogen-resistant biotechnologies.

Biochemical and Aquaculture Sector

Thermal anomalies in the Pacific drastically change the cost structure in global feed and food production.

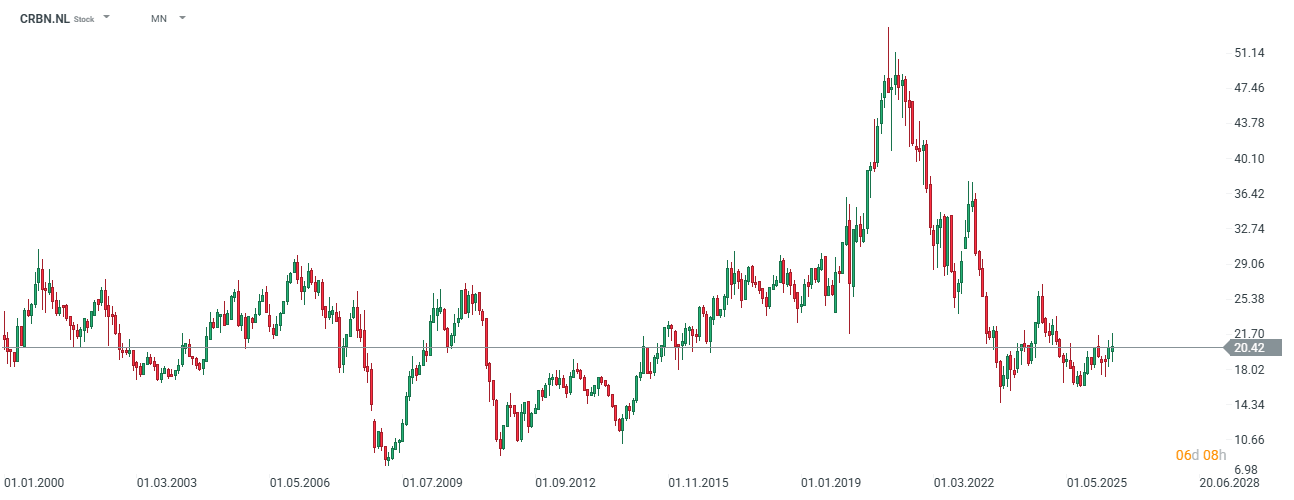

Corbion NV (CRBN.NL): The company is a key winner of the raw material crisis in Peru. The upwelling blockage off the coast of Peru led to a complete halt of anchovy fishing in May 2026. Prices of traditional fish oil (a key ingredient in salmon feeds and dietary supplements) jumped from 3.10 dollars per kilogram in July 2025 to a record 10 dollars per kilogram in June 2026. Corbion is a global leader in industrial production of alternative algae oil rich in Omega-3 fatty acids. The price jump of natural fish oil made Corbion’s product reach price parity, generating powerful demand from feed and baby formula producers. Berenberg raised its recommendation for Corbion to “Buy” with a target price of 24 euros, forecasting EBITDA growth from the algae segment alone to 44 million euros in 2026 and 49 million euros in 2027. The company is also cited as an attractive acquisition target for global players following the planned spin-off of the polylactic acid (PLA) segment.

The company has lost almost 1/3 of its value since the peak in 2020. Source: xStation5

Food Processing and Candy Manufacturer Sector

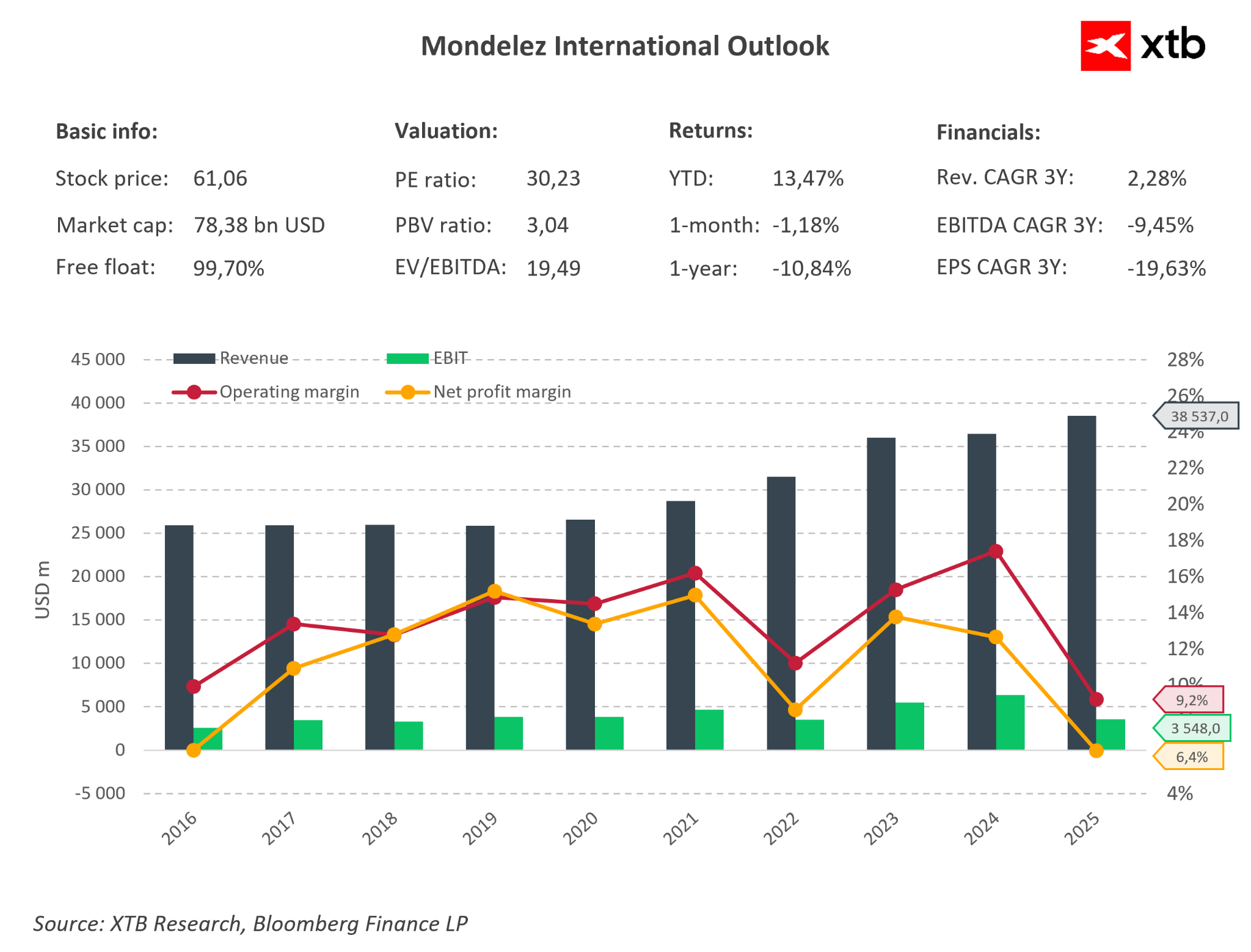

Mondelēz International Inc. (MDLZ): As the owner of brands such as Cadbury, Milka, and Toblerone, the company is one of the largest global consumers of cocoa and sugar. In conditions of raw material crisis caused by El Niño, Mondelez uses a highly effective margin protection strategy through so-called “shrinkflation” (reducing the weight of products while maintaining existing price points) and intense expansion in the premium segment. CEO Dirk Van de Put argues that consumers are more willing to accept a smaller bar than a higher price on the shelf. Additionally, the company invested 65 million CHF in expanding the Toblerone factory in Bern, transforming it into a global Center of Excellence. This strategy allows for maintaining high profitability (in 2025 revenues grew 5.8% y/y to 38.5 billion USD, and net profit reached 2.45 billion USD). Although CFO Luca Zaramella indicates some stabilization and “normalization” of cocoa prices from extreme highs, this raw material remains structurally expensive, meaning Mondelez’s ability to pass costs on to consumers (pricing power) will be a key factor deciding the preservation of margins in the 2026/2027 season.

The company currently has fairly low margins, but due to the situation, there is significant potential for a return to the 2023 situation. Additionally, the company appears to be undervalued currently, looking at a fundamental valuation based on averages from the last 5 years. The company’s shares are more than 20% below historical peaks. Source: Bloomberg Finance LP, XTB

Insurance and Financial Sector

Shifts in jet streams caused by El Niño generate asymmetric risks for financial institutions.

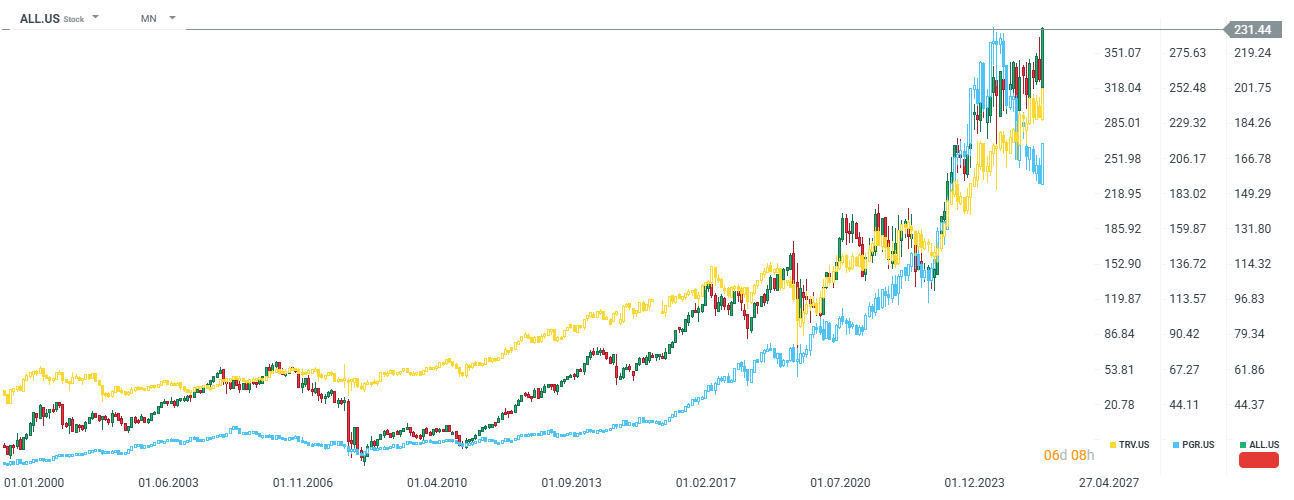

Allstate Corp. (ALL.US). Progressive Corp. (PGR) / Travelers (TRV): Theoretical beneficiaries of El Niño. This phenomenon causes strong wind shear over the Atlantic, which makes it difficult for destructive hurricanes to form off the coast of Florida and in the Gulf of Mexico (NOAA forecasts indicate a drop in the number of named storms to a level of 8 to 14 in the 2026 season compared to a norm of 14). Fewer hurricanes mean a radical reduction in claim costs for American property insurers. However, the unpredictability of climate change remains a risk, as it could bring other local disasters.

Allstate and Travelers are currently at historical levels, while Progressive Corp may appear somewhat undervalued relative to the sector. Source: xStation5

Credicorp Ltd. (BAP). Intercorp Financial Services (IFS): Peruvian financial holdings were downgraded by JPMorgan to a “Neutral” recommendation. El Niño directly hits key sectors of the Peruvian economy, namely fishing and agriculture. JPMorgan indicates that bank valuations at 2.5 times book value for BAP (target price around 360 dollars) and 1.7 times for IFS (target price around 56 dollars) do not fully discount the risk of an increase in write-offs on unpaid agricultural and fishing loans and the political uncertainty associated with the power transition process in Peru.

Summary and Conclusions for Commodity and Equity Investors

The Super El Niño anomaly at the turn of 2026 and 2027 should not be treated as a simple signal for speculative purchase of all agricultural commodities. Precise positioning in the market requires considering climate asymmetry and overlapping structural factors. The basis of an effective strategy is abandoning traditional ONI index readings in favor of the RONI index, which is cleared of the ocean warming trend. Investors should avoid exposure to soybeans and American natural gas (or look for sell signals), which, due to the specificity of Pacific teleconnections, become natural beneficiaries and exhibit a downward trend.

In turn, the key growth potential lies in soft commodities such as Robusta coffee (which partially translates into Arabica coffee prices) and cocoa, where El Niño drastically deepens an already tight supply-demand balance. On the other hand, an aspect that El Niño does not take into account is demand, which is depleted after these commodities hit historical peaks. In the equity segment, the optimal choice is capital allocation into companies with a high barrier to entry and direct operational leverage on the effects of

EURUSD starts today’s session in a noticeably tense yet somewhat uneven atmosphere, where the market lacks a single dominant narrative. On one side, investors are already looking ahead to the evening and the Federal Reserve’s decision, which could set the tone for the US dollar over the coming weeks. On the other side, Europe refuses to fade into the background, as fresh inflation data once again highlights that the ECB story and its future policy response to price pressures remain unresolved.

In practice, EURUSD is trading in an environment where no clear narrative has taken control. Market participants are simultaneously trying to price in the Fed, the ECB, and the widening divergence between them, which naturally increases volatility and means that any new impulse can quickly shift the balance of forces. In such a setup, the currency pair becomes particularly sensitive to changes in expectations, especially on a day filled with major macroeconomic events.

Source: xStation5

What is driving EURUSD today?Kevin Warsh’s debut and the Fed credibility test

Today’s Federal Reserve meeting carries special significance as it is the first under the leadership of Kevin Warsh. Markets are almost fully aligned in expecting interest rates to remain unchanged in the 3.50–3.75% range, but the decision itself is not the key focus. Far more important will be the tone of communication and how the new Fed Chair outlines the future path of monetary policy. Warsh takes control at a time when US inflation remains sticky and the economy continues to show relative resilience, limiting room for an early policy easing cycle. This makes today’s message potentially a directional signal for the entire Fed cycle. Even a subtle shift toward a more hawkish stance could strengthen the US dollar and add downward pressure on EURUSD.

Europe: inflation in line with forecasts, but pressure persists

On the European side, today brought the final release of May HICP inflation. The reading of 3.2% year on year came in exactly in line with consensus expectations, which helps stabilize short-term market positioning. However, it does not change the broader picture, where inflation remains elevated compared to last year. This keeps price pressures firmly on the radar of the European Central Bank. Particular attention continues to be drawn to persistent core inflation and the services component, both of which still show no clear disinflationary trend.

ECB and rising risks of further tightening

The lack of any positive surprise in inflation data leaves the ECB in a challenging position. After its recent rate hike, markets are once again reassessing whether the tightening cycle is truly over. If price pressures in services remain elevated and core inflation fails to meaningfully ease, the European Central Bank may be forced into another move later this year. Such a scenario limits the downside potential for the euro and acts as an important counterbalance to US dollar strength.

Market picture: tension between two central banks

EURUSD remains a market driven by two opposing narratives. On one side, investors are focused on the Fed and its impact on US dollar valuation. On the other, persistent inflation in Europe continues to support cautious expectations regarding the ECB. In this environment, markets become highly sensitive to central bank communication, while the technical structure of price action reinforces the sense of a fragile equilibrium, vulnerable to sharp shifts.

Key takeaways

Today’s EURUSD session is shaped by two opposing forces that broadly offset each other

The Fed remains the primary driver for the US dollar and could set the tone for the coming period

Europe continues to face persistent inflation with no clear signs of meaningful easing

The market remains in a wait-and-see mode with no dominant narrative

The key resolution will likely come only after the evening Fed decision and press conference

The United Kingdom (UK) headline Consumer Price Index (CPI) climbed 2.8% over the year in May, compared to a rise of 2.8% in April, the data released by the Office for National Statistics (ONS) showed on Wednesday. The UK inflation reading was well above the Bank of England’s (BoE) 2% inflation target.

The core CPI (excluding volatile food and energy items) rose 2.6% year-over-year (YoY) in the same period, compared to April’s 2.5% print and came in softer than the forecast of 2.7%.

Meanwhile, the monthly UK CPI arrived at 0.2% in May versus a rise of 0.7% reported in April, below the market consensus of 0.4%.

The British Pound (GBP) attracts some sellers in an immediate reaction to the UK inflation report. At the time of writing, the GBP/USD pair is trading 0.05% lower on the day to trade at 1.3420.

Pound Sterling Price Today

The table below shows the percentage change of British Pound (GBP) against listed major currencies today. British Pound was the weakest against the Swiss Franc.

USD

EUR

GBP

JPY

CAD

AUD

NZD

CHF

USD

-0.04%

0.02%

-0.08%

0.03%

0.12%

0.19%

-0.22%

EUR

0.04%

0.06%

-0.02%

0.06%

0.15%

0.26%

-0.17%

GBP

-0.02%

-0.06%

-0.09%

0.03%

0.13%

0.19%

-0.20%

JPY

0.08%

0.02%

0.09%

0.10%

0.19%

0.22%

-0.10%

CAD

-0.03%

-0.06%

-0.03%

-0.10%

0.09%

0.16%

-0.21%

AUD

-0.12%

-0.15%

-0.13%

-0.19%

-0.09%

0.09%

-0.29%

NZD

-0.19%

-0.26%

-0.19%

-0.22%

-0.16%

-0.09%

-0.38%

CHF

0.22%

0.17%

0.20%

0.10%

0.21%

0.29%

0.38%

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the British Pound from the left column and move along the horizontal line to the US Dollar, the percentage change displayed in the box will represent GBP (base)/USD (quote).

What do United Kingdom CPI inflation data mean for the British Pound?

The UK CPI is a measure of consumer price inflation, the rate at which the prices of goods and services bought by households rise or fall. This figure is one of the most important economic indicators for the GBP because it measures inflation and plays a key role in the Bank of England’s (BoE) monetary policy decisions.

Hotter-than-expected CPI Inflation suggests stronger price pressures in the economy. Traders may expect the BoE to keep interest rates higher-for-longer or consider additional rate hikes.

On the other hand, softer-than-expected outcomes may indicate easing price pressures in the UK economy. Markets could increase their bets on future BoE rate cuts.

Technical Analysis: GBP/USD maintains a neutral outlook in the near-term

In the daily chart, GBP/USD holds just above the Bollinger middle band, while still capped by the 100-day simple moving average (SMA). This configuration suggests a neutral near-term bias, with price consolidating inside the Bollinger envelope rather than trending. The Relative Strength Index (RSI) at roughly 50 hints at balanced momentum, leaving the pair dependent on a break outside this nearby band-and-MA corridor to define the next directional move.

On the topside, initial resistance emerges at the 100-day SMA around 1.3460, with the Bollinger upper band near 1.3498 forming a secondary barrier if buyers extend the recovery. On the downside, immediate support is seen at the Bollinger middle band around 1.3420, ahead of a deeper cushion at the Bollinger lower band close to 1.3345, where a break would expose a broader corrective phase.

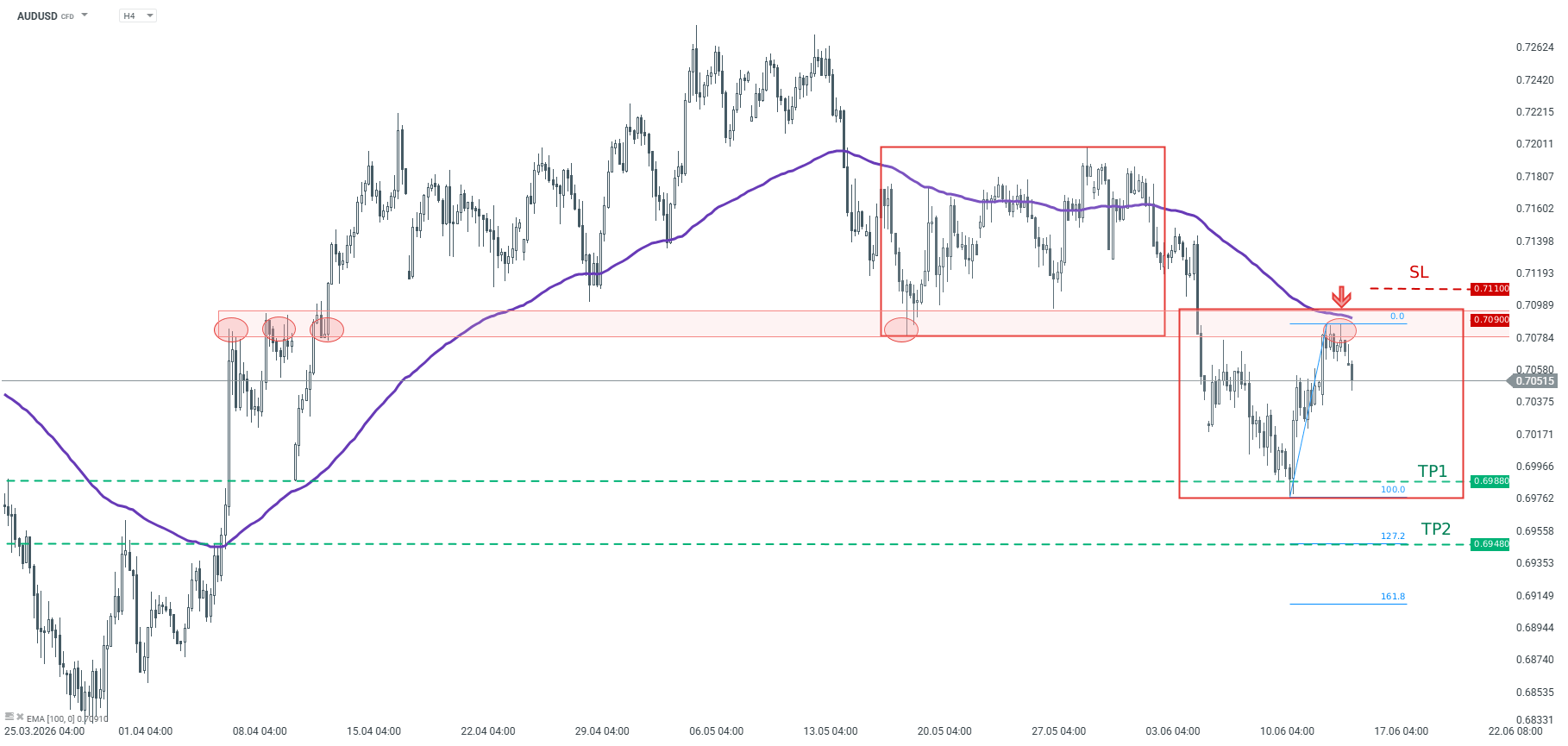

The pair bounced off the key resistance area near 0.7090 Short – term trend remains downward from the mid-May

Recommendation:

Trade: Short position on AUDUSD at market price Target: 0.6988, 0.6948 Stop: 0.7110

Opinion:

AUDUSD has been trading in a downward move recently. Looking at the H4 interval, one can see that the price bounced off the key 0.7090 resistance area. Red area near 0.7090 handle on the chart below is marked with previous price reactions, 100-period moving average from H1 interval, as well as upper limit of 1:1 structure. Taking this into account, continuation of the downward move looks to be the base case scenario for now. We recommend going short AUDUSD at market price with two targets: 0.6988 and 0.6948. We also recommend placing a stop loss order at 0.7110.

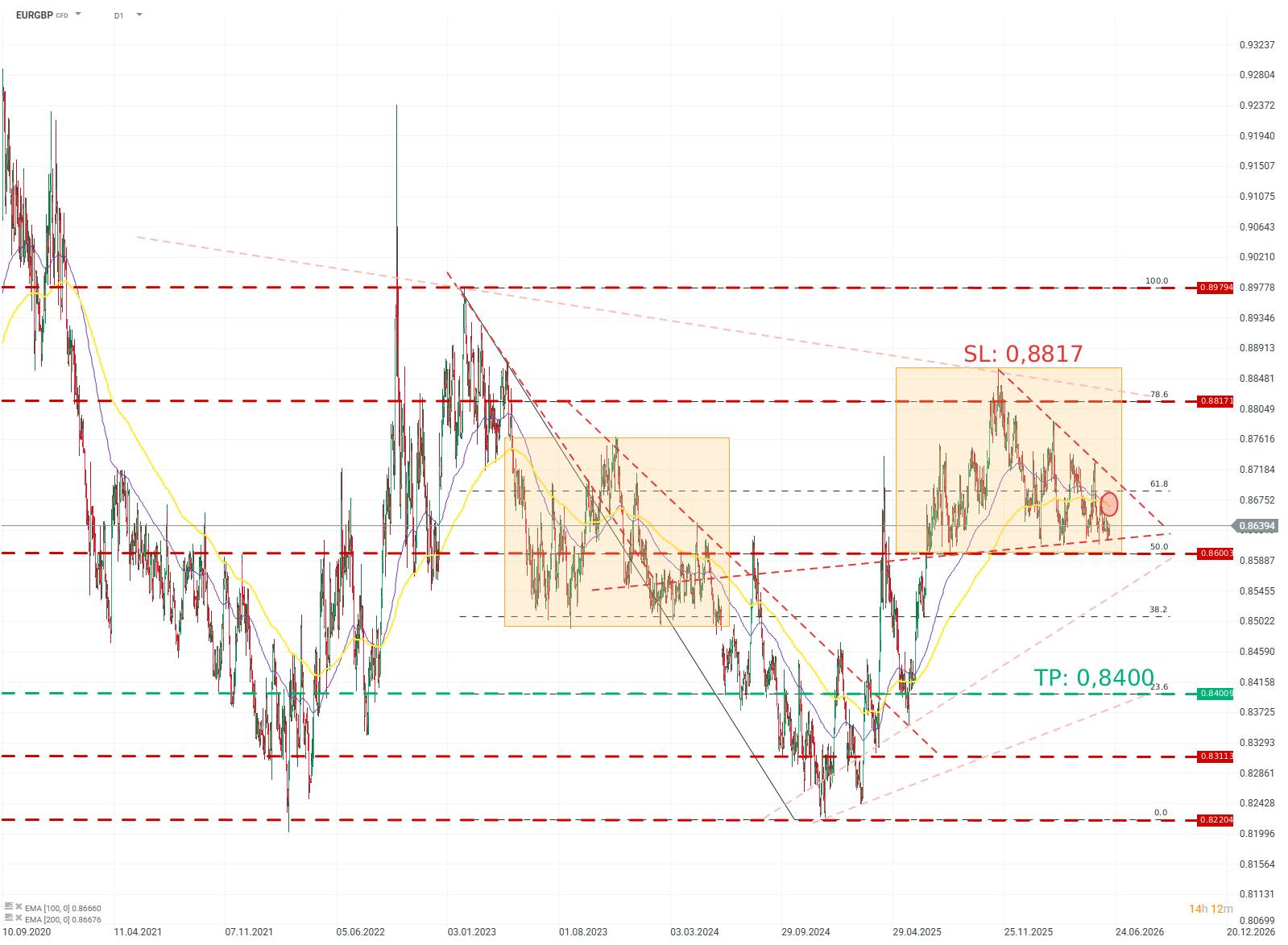

The price is near the lower boundary of a consolidation range between 0.886 and 0.861.

Upward corrections within the consolidation are breaking to increasingly lower levels, while at the same time testing resistance around 0.863.

The EMA100 has crossed the EMA200 from above.

Recommendation:

Short position (Sell) on EURGBP at the market price.

Target price (Take Profit; TP): 0.8400

Stop Loss (SL): 0.8817

EURGBP (D1)

Source: xStation5

OPINION :

The EURGBP rate is once again testing the lower boundary of the consolidation, which can also be treated as a developing 1:1 pattern, potentially ending with a downside breakout. The repeated defense of the ~0.86 level indicates the strength of this zone; however, increasingly weaker upward corrections within the consolidation reveal buyer weakness and point to the likely direction of further price movement.

Methodology and assumptions:

The recommendation is based on technical analysis of the chart, in particular EMA moving averages and Fibonacci levels.

The target level was determined based on Fibonacci levels.

The protective stop-loss order was set based on a favorable risk-to-reward ratio and with reference to a Fibonacci level.

NZD/USD may find initial support at the rectangle’s lower boundary near 0.5790.

The 14-day Relative Strength Index around 43 suggests waning upside momentum rather than outright oversold conditions.

The initial barrier lies at the nine-day EMA of 0.5853.

NZD/USD gains ground for the second successive day, trading around 0.5810 during the Asian hours on Tuesday. Technical analysis of the daily chart suggests the spot price is moving sideways within a rectangle pattern, reflecting a period of market consolidation and indecision.

The NZD/USD pair is maintaining a bearish near-term bias as spot holds beneath both the nine-day and 50-day Exponential Moving Averages (EMAs). The alignment of price below these short- and medium-term EMAs suggests rallies are likely to be sold, while a soft 14-day Relative Strength Index (RSI) reading around 43 hints at waning upside momentum rather than outright oversold conditions.

The NZD/USD pair may find initial support at the lower boundary of the rectangle around 0.5790, followed by the two-week low of 0.5782, recorded on June 8. A break below this confluence support zone would put downward pressure on the pair to navigate the region around a six-month low of 0.5681, which was recorded on April 6.

On the upside, the NZD/USD pair may rise toward the primary barrier at the nine-day EMA of 0.5853, followed by the 50-day EMA at 0.5875. A successful break above these moving averages could support the pair to approach the upper boundary of the rectangle around 0.5990, followed by the three-month high of 0.5995, which was reached on February 29.

(The technical analysis of this story was written with the help of an AI tool.)

New Zealand Dollar Price Today

The table below shows the percentage change of New Zealand Dollar (NZD) against listed major currencies today. New Zealand Dollar was the strongest against the Japanese Yen.

USD

EUR

GBP

JPY

CAD

AUD

NZD

CHF

USD

-0.02%

-0.07%

0.05%

-0.04%

0.00%

-0.18%

-0.04%

EUR

0.02%

-0.02%

0.09%

-0.01%

0.07%

-0.12%

0.01%

GBP

0.07%

0.02%

0.13%

0.06%

0.06%

-0.11%

0.04%

JPY

-0.05%

-0.09%

-0.13%

-0.08%

-0.03%

-0.21%

-0.08%

CAD

0.04%

0.01%

-0.06%

0.08%

0.04%

-0.12%

0.00%

AUD

-0.00%

-0.07%

-0.06%

0.03%

-0.04%

-0.16%

-0.04%

NZD

0.18%

0.12%

0.11%

0.21%

0.12%

0.16%

0.12%

CHF

0.04%

-0.01%

-0.04%

0.08%

-0.00%

0.04%

-0.12%

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the New Zealand Dollar from the left column and move along the horizontal line to the US Dollar, the percentage change displayed in the box will represent NZD (base)/USD (quote).

EUR/JPY gathers strength near 184.85 in Tuesday’s early European session.

The cross keeps the bullish vibe, but further consolidation cannot be ruled out in near term with neutral RSI momentum.

The initial support level is seen at 184.50; the immediate resistance level to watch is 185.12.

The EUR/JPY cross holds positive ground around 184.85 during the early European session on Tuesday. A hawkish stance from the European Central Bank (ECB) underpins the Euro (EUR) against the Japanese Yen (JPY). The ECB will hold its June monetary policy meeting on Thursday. Markets have fully priced in a 25-basis-point (bps) rate hike after Eurozone inflation surged to 3.2%.

Markets are on high alert for foreign exchange intervention from Japanese authorities. This, in turn, might support the JPY and act as a headwind for the cross. Japanese authorities have issued strong verbal warnings, stating that the government is fully prepared to take decisive and appropriate action to protect the domestic currency.

Technical Analysis:

In the daily chart, EUR/JPY holds a constructive bullish bias as spot remains above the 100-day simple moving average (SMA) and the Bollinger band midline. Price also sits comfortably above the lower Bollinger band, suggesting the broader uptrend structure is still intact, while the Relative Strength Index (RSI) at 45.9 leans slightly soft but remains in neutral territory, hinting at consolidative rather than impulsive downside momentum.

On the downside, the initial support zone is formed by the 100-day SMA at 184.50, followed by the lower Bollinger band near 184.20, which should limit deeper pullbacks if the bullish structure is to persist. The first upside barrier emerges at the the Bollinger band midline at 185.12, en route to the upper boundary of the Bollinger Band at 185.12. Any follow-through buying above this level could pave the way to the 186.00 psychological level.

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.