- AUD/JPY strengthens to near 111.80 in Wednesday’s Asian session.

- The cross maintains the constructive outlook above the 100-day EMA, with bullish RSI momentum.

- The initial support level is located at 111.00; the first upside barrier emerges at 112.50.

The AUD/JPY cross gathers strength to around 111.80 during the Asian trading hours on Wednesday. The Australian Dollar (AUD) edges higher against the Japanese Yen (JPY) amid improved risk sentiment. US President Donald Trump said late Tuesday that he had agreed “to suspend the bombing and attack of Iran for a period of two weeks” on the condition that Iran reopens the Strait of Hormuz.

Iranian Foreign Minister Seyed Abbas Araghchi stated that during the two weeks, safe passage through the Strait of Hormuz “will be possible via coordination with Iran’s Armed Forces and with due consideration of technical limitations.” Easing tensions in the Middle East undermines a safe-haven currency such as the JPY and acts as a tailwind for the cross in the near term.

On the other hand, fears that Japanese authorities would step in to support the domestic currency might cap the downside for the JPY. Japan’s top currency diplomat Atsushi Mimura said last week that officials may need to take “decisive” steps if speculative moves persist in the currency market.

Technical Analysis:

In the daily chart, the near-term bias of AUD/JPY is bullish as price extends its advance well above the 100-day exponential moving average around 107.50, confirming a dominant uptrend and resilient dip demand. The latest candles hold in the upper half of the Bollinger Band envelope, while the bands remain relatively wide, signalling sustained upside momentum rather than a volatility blow-off. RSI has rebounded toward the high-50s, recovering from mid-range readings and aligning with renewed buying pressure after the recent consolidation above the 111.00 handle.

Initial support emerges at 111.00, where recent lows converge with the mid-Bollinger zone, and a break below would expose deeper pullback risk toward the 110.00 area. Stronger downside protection aligns near the 109.00 region, close to the Bollinger lower band cluster and prior congestion, and a loss of this floor would weaken the broader bullish structure. On the topside, immediate resistance stands at the March 19 high of 112.61, followed by the upper boundary of the Bollinger Band of 113.15.

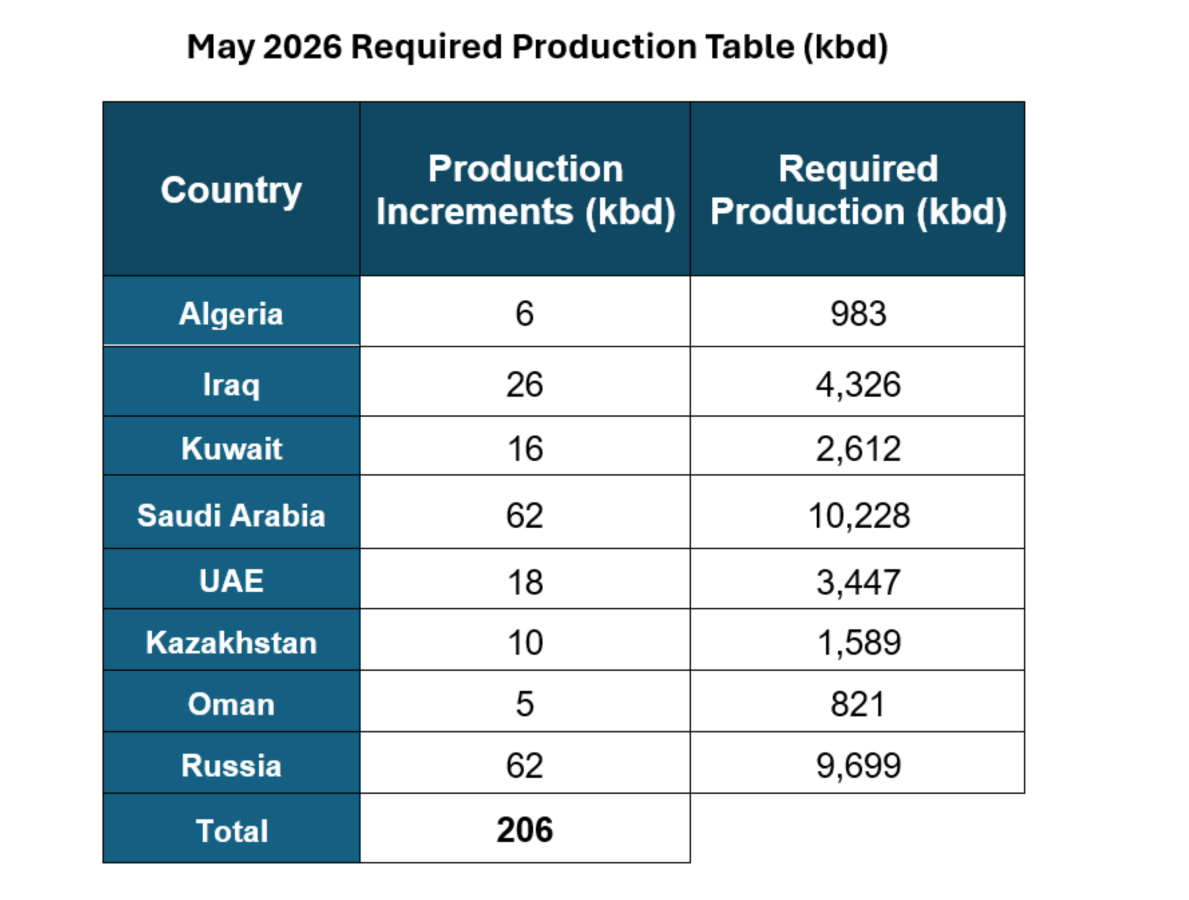

New production quotas for countries in the agreement on voluntary production cuts. It is worth noting that countries like Iraq, Kuwait, Saudi Arabia, the UAE, and also Russia have significantly reduced their production volumes recently. Source: OPEC

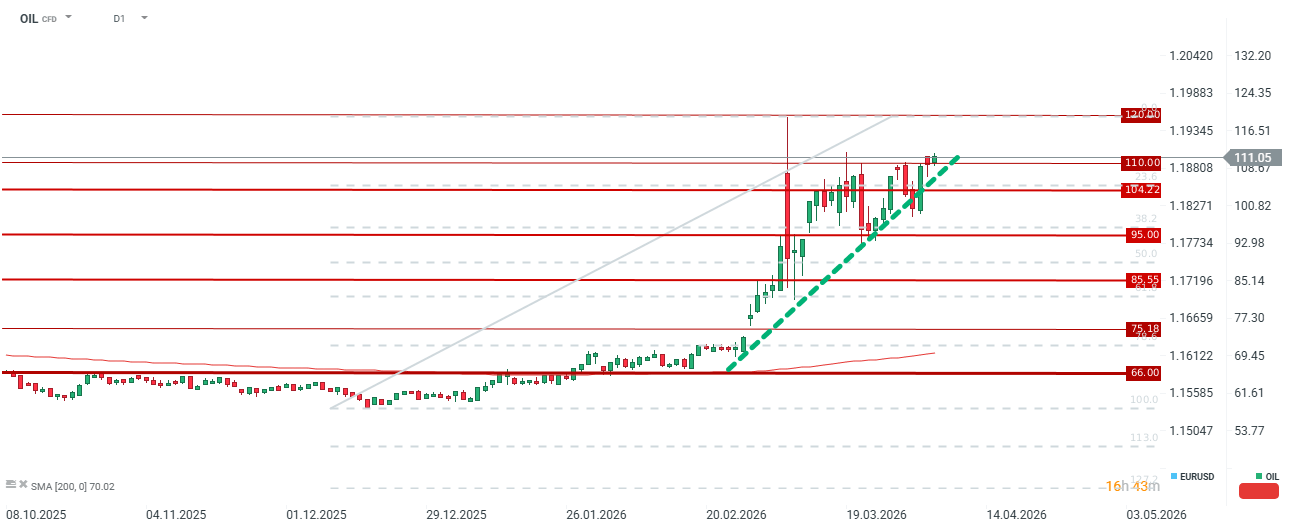

New production quotas for countries in the agreement on voluntary production cuts. It is worth noting that countries like Iraq, Kuwait, Saudi Arabia, the UAE, and also Russia have significantly reduced their production volumes recently. Source: OPEC Oil is currently in a zone of strong supply and is no longer reacting as dynamically as it was a few days ago. The Strait of Hormuz remains closed, but some ships are passing through, so prices may be under slight pressure. Nevertheless, a few ships will not lead to a significant improvement in the global supply situation. Source: xStation5

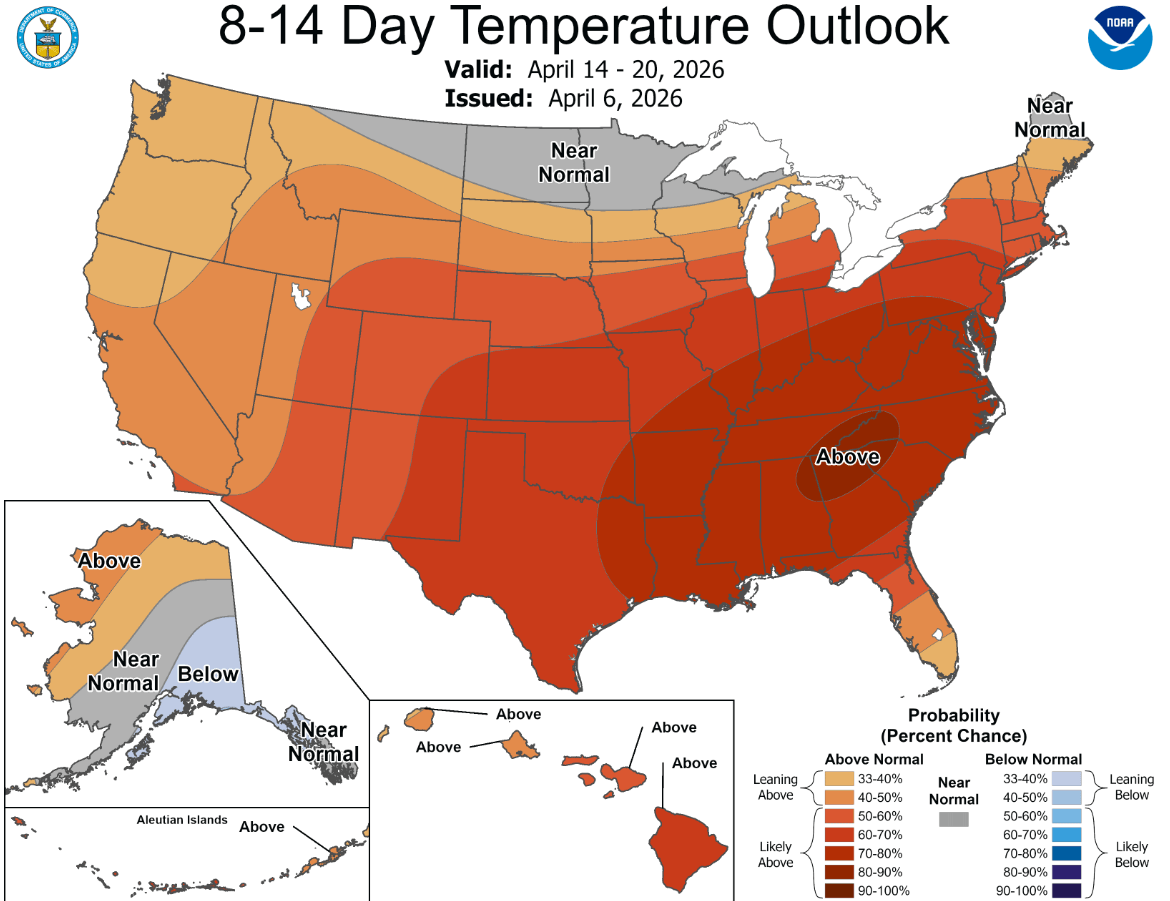

Oil is currently in a zone of strong supply and is no longer reacting as dynamically as it was a few days ago. The Strait of Hormuz remains closed, but some ships are passing through, so prices may be under slight pressure. Nevertheless, a few ships will not lead to a significant improvement in the global supply situation. Source: xStation5 Forecasts for the next 2 weeks indicate that temperatures will be higher than standard. This means that gas consumption for heating purposes should be minimal. Nevertheless, seasonal forecasts suggest that in the summer period, temperatures should also be higher, which means higher consumption in the future. Source: NOAA

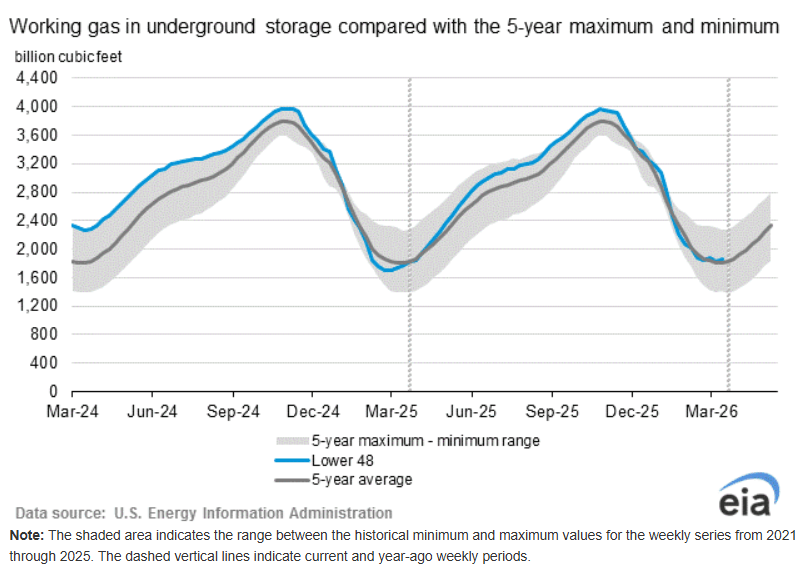

Forecasts for the next 2 weeks indicate that temperatures will be higher than standard. This means that gas consumption for heating purposes should be minimal. Nevertheless, seasonal forecasts suggest that in the summer period, temperatures should also be higher, which means higher consumption in the future. Source: NOAA Gas inventories have fallen toward the 5-year average, but are now starting to rebound. In March, we had 2 reports that showed a rebound in inventories, despite the theoretical duration of the heating season. Source: EIA

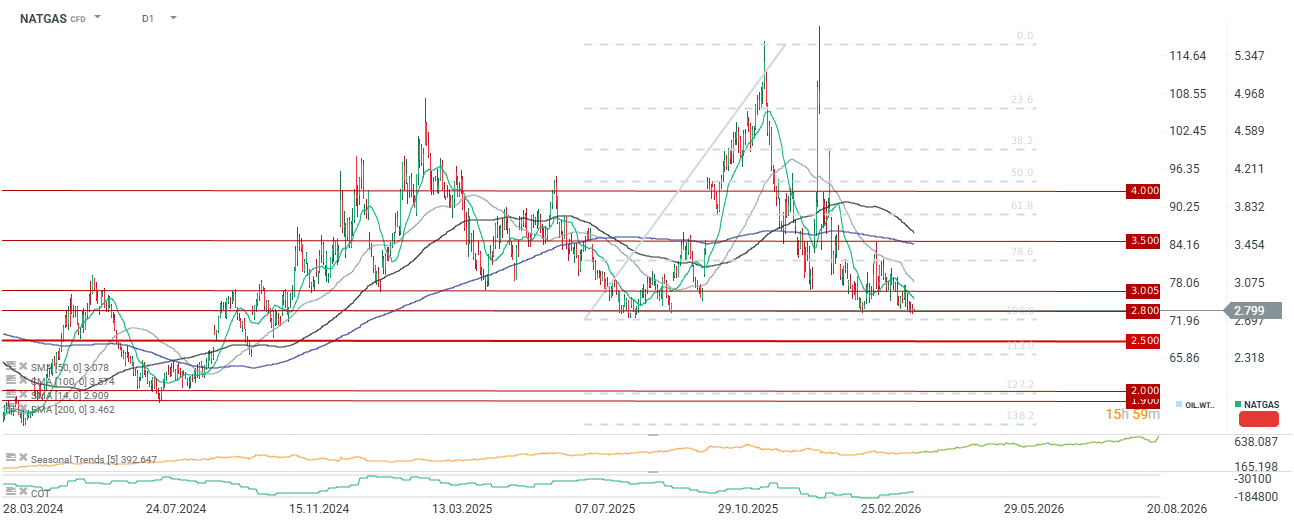

Gas inventories have fallen toward the 5-year average, but are now starting to rebound. In March, we had 2 reports that showed a rebound in inventories, despite the theoretical duration of the heating season. Source: EIA The price is at very important support around $2.8/MMBTU. Source: xStation5

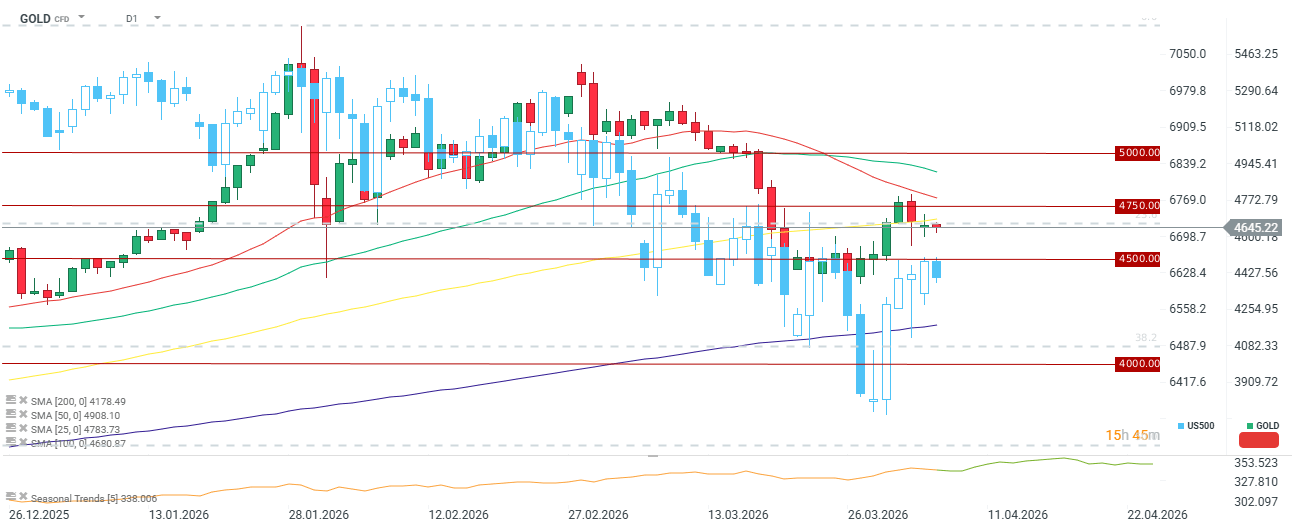

The price is at very important support around $2.8/MMBTU. Source: xStation5 The correlation between the price of gold and the US500 has been quite high since almost the beginning of this year. Nevertheless, the scale of the US500 rebound recently does not coincide so strongly with the rebound in the gold price. Source: xStation5

The correlation between the price of gold and the US500 has been quite high since almost the beginning of this year. Nevertheless, the scale of the US500 rebound recently does not coincide so strongly with the rebound in the gold price. Source: xStation5 The cocoa price remains at low levels due to the lack of signs of a demand rebound. Theoretically, we should observe an improvement in the second half of this year after the exhaustion of inventories from previous years. Source: xStation5

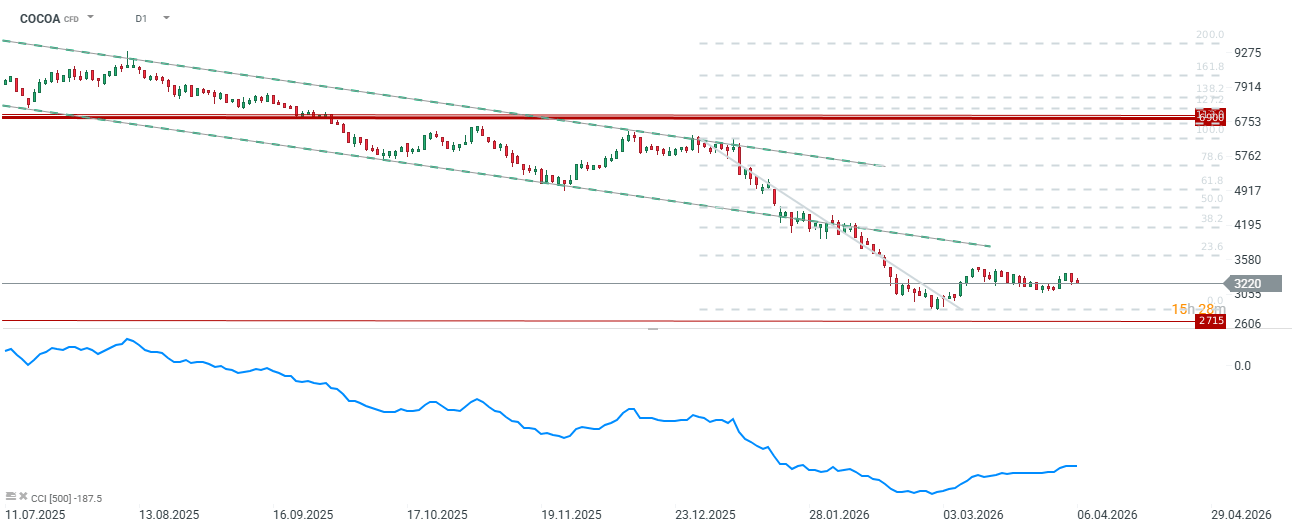

The cocoa price remains at low levels due to the lack of signs of a demand rebound. Theoretically, we should observe an improvement in the second half of this year after the exhaustion of inventories from previous years. Source: xStation5