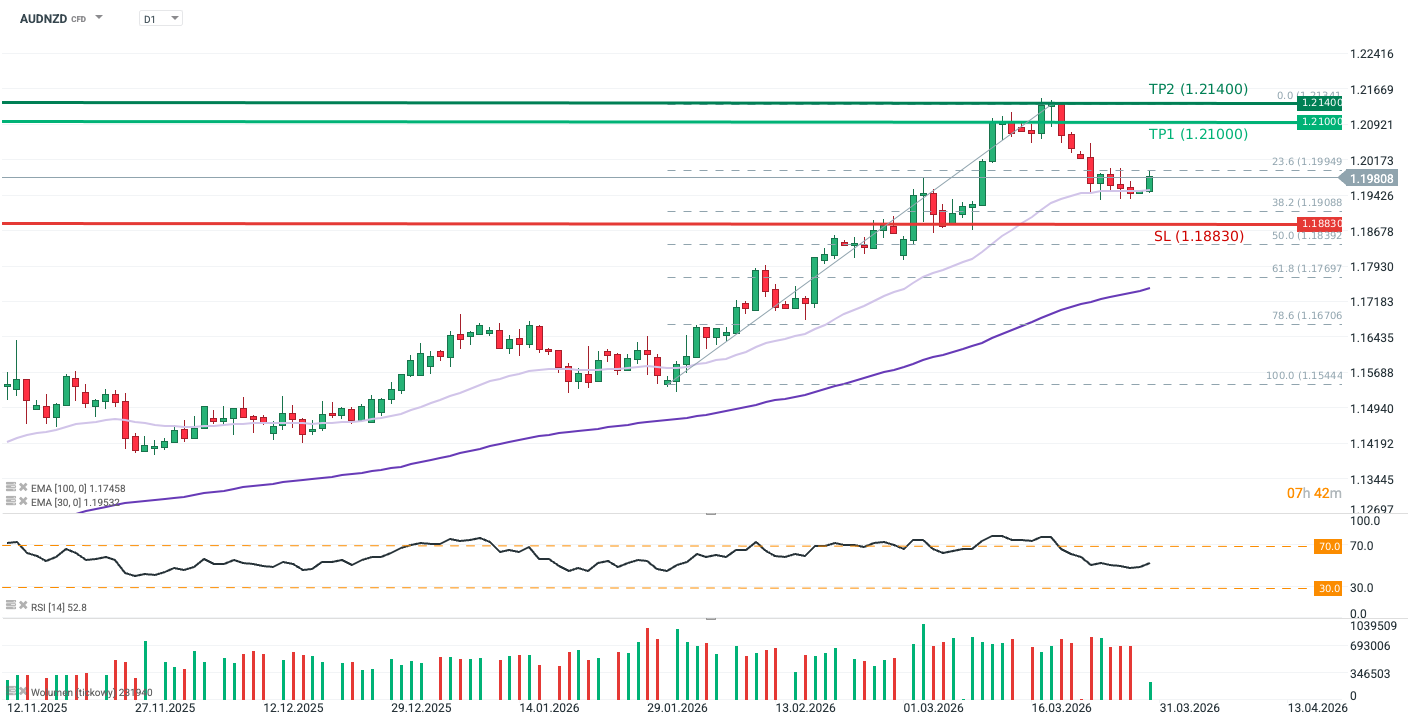

Facts

- AUDNZD rebounded from the 30-day exponential moving average (EMA30; light purple) during today’s session.

- The swap market (OIS curve) currently prices an approximately 60% probability of an interest rate hike in Australia for May, compared to approximately 8% in New Zealand.

- The RSI stands at approximately 52, remaining well below the overbought threshold (i.e., below 70).

Recommendation

- Long Position (BUY) at market price

- Target Prices (Take Profit): 1.21000 (TP1), 1.21400 (TP2)

- Stop Loss (SL): 1.18830

Source: xStation5

Opinion

AUDNZD recently underwent a correction triggered by a global decline in risk appetite and concerns regarding an economic slowdown in China. As China is highly dependent on Iranian oil, its trade ties with the Australian mining industry significantly influence the Australian dollar’s valuation. However, the downward move stalled at the EMA30; after several days of sideways trading, the pair rebounded, signaling a likely continuation of the broader uptrend.

While global inflation concerns driven by energy prices remain prevalent, the Reserve Bank of Australia (RBA) continues to position itself as the most hawkish central bank among G10 nations, with rates currently at 4.10%. This creates a favorable carry trade opportunity against the significantly more dovish Reserve Bank of New Zealand (RBNZ), where rates stand at 2.25%.

The 10-year bond yield spread between the two economies has remained stable since early March (at approximately 30 bps). Therefore, in the short term, Australia’s active hiking cycle should continue to support the AUDNZD trend. A primary risk factor would be a decisive pivot from the RBNZ; according to the OIS curve, markets expect the RBNZ to resume hikes in the autumn, potentially ending the year with rates at 3%.

Methodology

This recommendation was prepared based on a technical analysis of the AUDNZD chart and a fundamental analysis of both economies (focusing on Australian and New Zealand monetary policy). The directional bias was determined using moving averages, price action, and market expectations regarding central bank responses to the ongoing conflict in Iran. Take Profit and Stop Loss levels were set using Price Action methodology (TP1 at the nearest resistance, TP2 at the recent peak, and SL at the nearest swing low).