EUR/USD trades lower at around 1.1390 as the US Dollar strengthens.

Increased aggression between the US and Iran has improved the US Dollar’s safe-haven demand.

Investors await Fed Chair Warsh’s testimony and the US CPI data.

The Euro (EUR) holds opening losses at around 1.1390 against the US Dollar (USD) during the mid-Asian trading session on Monday. The major currency pair faces selling pressure as the US Dollar starts the week on a strong note due to an increase in the appeal of safe-haven assets.

At press time, the US Dollar Index (DXY), which gauges the Greenback’s value against six major currencies, trades 0.2% higher to near 101.15.

Escalating military actions between the United States (US) and Iran over Tehran showing dominance over the Strait of Hormuz, a critical chokepoint to almost 20% of global energy supply, have forced investors to shift to the safe-haven fleet and have de-anchored inflation expectations.

To get cues regarding the current status of US inflation, investors will pay close attention to the Consumer Price Index (CPI) data for June, which will be released on Tuesday.

This week, investors will also focus on Federal Reserve (Fed) Chair Kevin Warsh’s two-day testimony before Congress starting on Tuesday.

Technical Analysis:

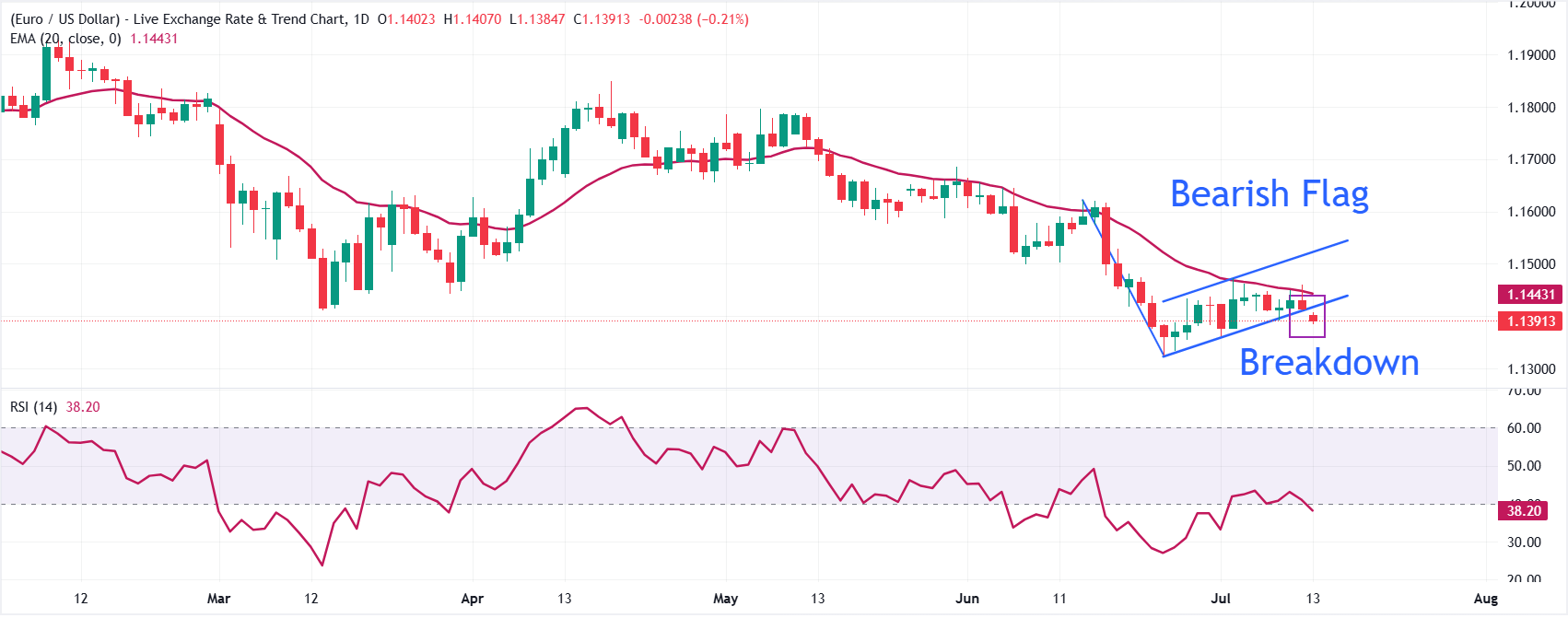

EUR/USD trades lower at around 1.1390, keeping a bearish near-term tone as spot holds beneath the 20-period Exponential Moving Average (EMA) at 1.1443 and a breakdown of the Bearish Flag formation.

The Relative Strength Index (14) hovers near 38, hinting at persistent but not extreme downside momentum.

On the topside, initial resistance is aligned with the lower boundary of the parallel channel near 1.1424, followed by the 20-period EMA at 1.1443, with the channel top around 1.1530 acting as a stronger cap if a rebound extends. On the downside, major support levels are the June 24 low at 1.1324, followed by 1.1300.

The past week brought a sharp bout of volatility to global markets, particularly within the commodities sector.

An initial rebound in crude prices, fueled by escalating tensions in the Middle East, reverberated with redoubled force across weather-sensitive agricultural commodities. Markets enter the new week with attention firmly fixed on the United States. The macroeconomic calendar is packed with pivotal events poised to shape investor sentiment over the coming days.

The main highlights include the release of US consumer price index (CPI) data for June, congressional testimony by the newly appointed Fed Chair Kevin Warsh, and the official kickoff of the Wall Street earnings season. Given this confluence of catalysts, three markets warrant close scrutiny in the near term: GOLD , US500 and COCOA .

GOLD

This week, investor focus in the gold market will shift entirely toward the US dollar and the interest rate outlook, both of which face two powerful catalysts. On Tuesday, the US June CPI reading will be released, with consensus expectations pointing to a moderate deceleration in price growth. Following the release of the FOMC minutes, the market will pivot to the next Warsh-related event: the Fed Chair’s semi-annual testimony before Congress. Warsh will appear before the House Financial Services Committee on Tuesday, followed by questioning from the Senate Banking Committee on Wednesday.

Historically, during leadership transitions at the Federal Reserve, markets closely parse every word for clues regarding the future path of monetary policy. Hints of a more dovish tilt would provide potent fuel for a rally in gold, whereas unyielding hawkish rhetoric could unleash heavy selling pressure. However, it is worth noting that Warsh himself has signaled he does not intend to offer forward guidance to the markets. Consequently, the market’s own interpretation of his remarks will be critical.

US500 (S&P 500 Futures)

For the US equity market and its benchmark S&P 500 index, this week marks the commencement of another crucial corporate earnings season. Traditionally, the cycle kicks off with Wall Street’s banking giants; JPMorgan Chase, Citigroup, Wells Fargo, Goldman Sachs, and Bank of America are all scheduled to report on Tuesday.

Beyond financials, investors will closely dissect earnings from tech heavyweights ASML and TSMC (Wednesday and Thursday) as well as Netflix (Thursday). Juxtaposing these corporate results with Wednesday’s release of the Federal Reserve’s Beige Book and Thursday’s US retail sales data will provide a more comprehensive economic mosaic. This will allow market participants to gauge whether the US economy and its consumers remain resilient enough to sustain corporate earnings capable of justifying today’s stretched equity valuations.

COCOA

Cocoa has enjoyed a spectacular first half of the year. Following a sharp sell-off early on, the soft commodity is currently staging a massive rebound. While current prices remain below the historic highs printed in 2024, they have surged by roughly 60% since the El Niño weather phenomenon was officially declared last month. Measured from its recent troughs, the pace of the rebound reaches as high as 120%. Violent volatility in recent days has been driven by supply anxieties out of West Africa, where cocoa crop development was initially hit by torrential rains, and plantations are now threatened by the hot, dry conditions associated with El Niño.

Furthermore, the ICE exchange raised margin requirements in response to market instability, a move that only exacerbated swings and forced the capitulation of some speculative capital. This week will prove pivotal for investors in this market as attention shifts from weather patterns to hard demand data. Crucial quarterly European cocoa grindings data is due on Thursday.

A recent report from industry giant Barry Callebaut did register the first increase in sales volumes in over two years—partly driven by an earlier price correction—but the company simultaneously warned that global confectionery consumption remains under pressure. Following such a monumental rally from its lows, the upcoming grindings data will serve as an absolute litmus test of whether high prices have triggered genuine demand destruction, or if the market still has room to run.

The upcoming week will bring a major test for the US Dollar (USD), with investors focusing on the United States Consumer Price Index (CPI), Federal Reserve (Fed) Chair Kevin Warsh’s congressional testimony and a broad set of activity indicators. China’s second-quarter Gross Domestic Product (GDP) and the Bank of Canada’s (BoC) interest-rate decision will also attract significant attention.

The US Dollar Index (DXY) trades near 101.00, recovering from a one-week low hit earlier on Friday as investors balance softer recent labor market data against renewed geopolitical uncertainty and persistent inflation concerns. Tuesday’s US CPI report will be the central event for the Greenback.

Headline CPI is expected to decline 0.1% MoM in June, following a 0.5% increase in May, while annual inflation previously stood at 4.2%. Core CPI is forecast to rise 0.3% MoM, up from 0.2%, while the annual core rate is expected to remain unchanged at 2.9%.

On another note, Fed Chair Warsh will testify on Tuesday and Wednesday, giving markets an opportunity to assess how policymakers balance elevated inflation against signs of weaker hiring. Comments from several Fed officials and the release of the Beige Book will provide additional guidance.

US Dollar Price Today

The table below shows the percentage change of US Dollar (USD) against listed major currencies today. US Dollar was the strongest against the Swiss Franc.

USD

EUR

GBP

JPY

CAD

AUD

NZD

CHF

USD

0.12%

0.07%

-0.42%

-0.08%

-0.17%

-0.14%

0.21%

EUR

-0.12%

-0.05%

-0.54%

-0.19%

-0.30%

-0.27%

0.09%

GBP

-0.07%

0.05%

-0.50%

-0.13%

-0.25%

-0.23%

0.13%

JPY

0.42%

0.54%

0.50%

0.34%

0.25%

0.25%

0.60%

CAD

0.08%

0.19%

0.13%

-0.34%

-0.10%

-0.08%

0.27%

AUD

0.17%

0.30%

0.25%

-0.25%

0.10%

0.02%

0.35%

NZD

0.14%

0.27%

0.23%

-0.25%

0.08%

-0.02%

0.34%

CHF

-0.21%

-0.09%

-0.13%

-0.60%

-0.27%

-0.35%

-0.34%

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the US Dollar from the left column and move along the horizontal line to the Japanese Yen, the percentage change displayed in the box will represent USD (base)/JPY (quote).

EUR/USD trades lower near 1.1420, retreating as the US Dollar recovers from its weekly low, and is set to finish the week with a 0.19% loss. The pair will remain highly sensitive to US CPI and Warsh’s testimony, while the European calendar includes industrial production and final inflation figures.

GBP/USD trades near 1.3400, with a weekly gain of around 0.34% after reaching a three-week high. The Pound Sterling (GBP) faces an important domestic calendar, with United Kingdom (UK) GDP, industrial production, and manufacturing output due on Thursday. UK GDP is expected to grow 0.1% MoM in May, following a 0.1% contraction. Industrial production is forecast to rise 0.1%, while manufacturing production is expected to decline 0.1% after increasing 0.4% previously.

USD/JPY trades lower near 161.70 on Friday but is set to close the week with a 0.24% gain. The pair will remain driven by US Treasury yields, Fed expectations, and concerns over possible intervention by Japanese authorities. A hotter-than-expected US CPI report could lift yields and revive upward pressure on USD/JPY. Softer inflation could extend the pair’s decline and offer further support to the Japanese Yen.

AUD/USD trades slightly higher near 0.6950, supported by a softer broader US Dollar backdrop and recent strength in the Chinese Yuan. However, the Aussie’s direction next week will depend heavily on Chinese economic data and US inflation. Wednesday’s Chinese GDP report is expected to show the economy expanding 4.4% YoY in the second quarter, slowing from 5%. Quarterly growth is forecast at 0.9%. Industrial production is expected to rise 4.7%, while retail sales are projected to decline 0.1% YoY.

USD/CAD trades lower near 1.4150 ahead of Wednesday’s Bank of Canada policy decision. The BoC is expected to leave its benchmark rate unchanged at 2.25%. The accompanying Monetary Policy Report, policy statement and press conference will be closely examined for guidance on inflation, domestic demand and future rate moves. A hawkish message could extend USD/CAD’s decline, while a cautious stance may limit the Canadian Dollar’s strength.

West Texas Intermediate (WTI) Oil trades muted near $71.60 per barrel as investors assess the risk of renewed supply disruptions linked to tensions between the United States and Iran. Oil prices could become more volatile if diplomatic efforts deteriorate further or concerns surrounding Middle Eastern supply routes intensify. However, signs of weaker global demand, particularly from China, may limit gains.

Gold trades lower near $4,102, losing ground as the US Dollar recovers and investors prepare for the US inflation report. The precious metal remains supported by geopolitical uncertainty, although higher Treasury yields could create additional pressure.

Anticipating economic perspectives: Voices on the horizon

Monday, July 13:

Fed’s Bowman

Fed’s Waller

ECB’s Schnabel

BoE’s Pill

Tuesday, July 14:

Fed’s Warsh

Fed’s Barr

Fed’s Goolsbee

Fed’s Cook

Fed’s Bowman

BoE’s Bailey

Wednesday, July 15:

Fed’s Williams

Fed’s Chair Warsh

ECB’s Nagel

Fed’s Cook

Fed’s Musalem

Thursday, July 16:

Fed’s Logan

Fed’s Schmid

Fed’s Jefferson

Friday, July 17:

ECB’s Cipollone

Central banks’ meetings and upcoming data releases to shape

The main monetary-policy event will be the Bank of Canada interest-rate decision on Wednesday, July 15. The central bank is expected to leave its policy rate unchanged at 2.25%.

The BoC will also publish its Monetary Policy Report and policy statement, followed by a press conference. No interest-rate decisions are scheduled from the Fed, ECB, BoE, BoJ, RBA or RBNZ.

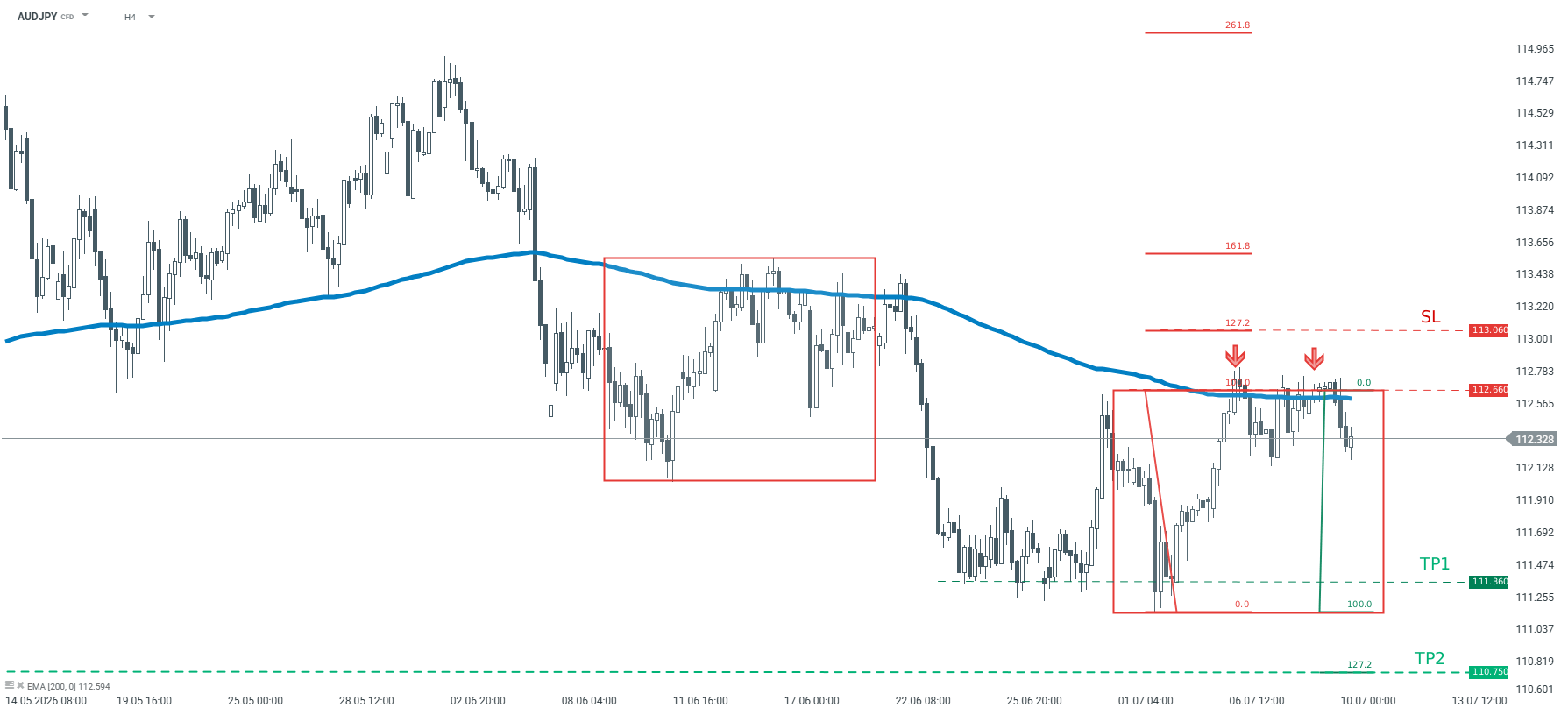

Recommendation: Trade: Short AUDJPY at market price Target: 111.36, 110.75 Stop: 113.06

Opinion:

Looking at AUDJPY on the H4 interval, one can see that the pair is trying to return to the main trend. Bulls did not manage to break above the key resistance at 112.66, and sellers took over. The aforementioned resistance is a result of an upper limit of 1:1 structure. According to the Overbalance strategy, as long as the price sits below it, one should expect the price to go lower. In addition, the price sits below the 200-period moving average which confirms the bearish sentiment. We recommend going short AUDJPY at market price with two targets: 111.36, 110.75 We also recommend placing a stop loss order at 113.06.

he yen strengthened on Friday following an announcement by Japanese Finance Minister Satsuki Katayama that the government intends to encourage pension funds, including the GPIF, to increase their investments in domestic financial assets — a move that many analysts regard as potentially more effective in supporting the currency than direct intervention. The market reacted with a sharp, though so far short-lived, rebound in USD/JPY from above 162 to 161.29, representing a move of almost 0.7 per cent.

Can pension funds sustain this reversal in the trend?

The key question traders are asking is: will the government actually bring about a structural change in the GPIF’s asset allocation, or is this merely verbal intervention without any real action? Today’s reaction can be described as a ‘knee-jerk reaction’, highlighting that the sustainability of further yen purchases requires concrete commitment, not just declarations. Since 2020, the GPIF has maintained a symmetrical 50/50 allocation between domestic and foreign assets, and as recently as March 2025, the fund confirmed that it has no plans to change this structure until 2030, which is indicative of significant institutional inertia.

Investors need to see concrete action, not just words, for the trend of a weakening yen to be reversed — including more aggressive interest rate rises by the BOJ, a reduction in the fiscal deficit, and a genuine change in the GPIF’s asset allocation. This does not alter the fact that even a slight ‘structural shift’ in the allocation would have a huge impact given the scale of the fund, whilst supporting the currency, bonds and shares. History shows, however, that the GPIF has already made radical shifts in its allocation (for example, in 2014 it reduced the share of domestic bonds from 60% to 35%, whilst increasing its equity holdings), so the scenario of a change is not unrealistic, but it requires a formal decision by the fund’s board, not merely a comment from the minister.

Kumiharu Shigehara, the former chief economist at the BOJ, offers a different perspective in the debate, warning that a weak yen is not a strength, but a warning sign — real wages in Japan have been falling for four years running, and the benefits of depreciation mainly go to exporters and asset holders, whilst households pay a higher price for imported energy and food. In his view, a sustained strengthening of the yen requires fiscal credibility, normalisation of monetary policy and productivity growth — not mere rhetoric or intervention.

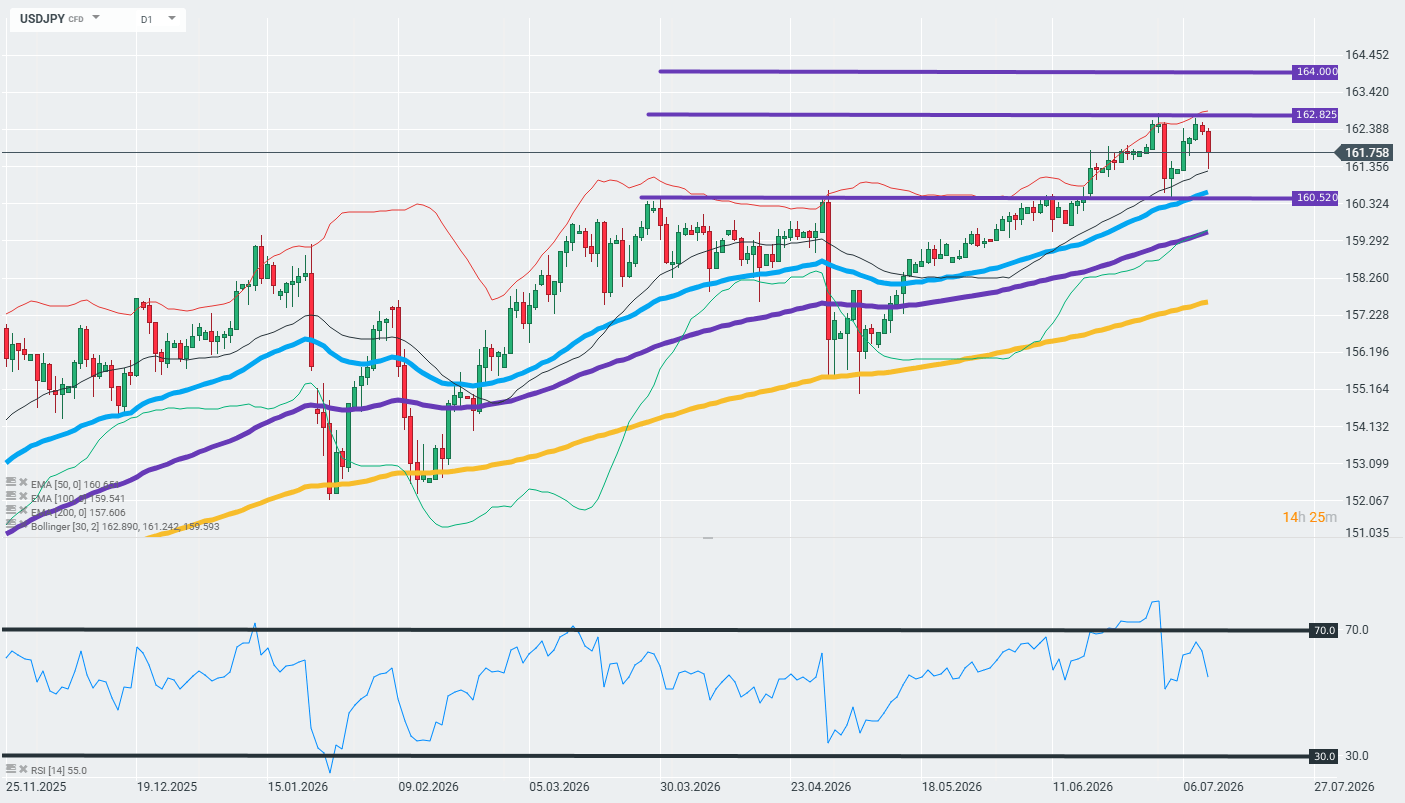

Technical analysis of the USD/JPY chart

The USD/JPY daily chart shows a clear, long-term uptrend that has been in place since November 2025, with the price consistently holding above all three EMAs (50, 100, 200), which confirms the strength of the trend.

Short-term resistance: 162.825 — the high from recent sessions, from which the price has just rebounded lower following the news about the GPIF

Long-term resistance: 164,000 — the next target level should the trend continue

Key support: 160.520 — former resistance from March–April 2026, now acting as structural support, coinciding with the 50-period EMA (160.65)

The market reaction to Katayama’s comments shows a typical ‘sell the rumour’ pattern following a strong rally — the price is testing the resistance level at 162.825 and is being rejected back towards the support level at the EMA50/160.520, but this has not yet broken the main uptrend (higher lows since November).

Is the movement sustainable?

The answer is: probably not in the short term, unless the GPIF takes a formal decision to change its strategic allocation. Fundamental differences in interest rates between the US and Japan, geopolitical tensions surrounding Iran and Japan’s growing fiscal deficit are structural factors that continue to weigh on the yen, regardless of government statements. Until we see concrete steps — a genuine revision of the GPIF’s allocation, a more hawkish BOJ or progress in fiscal consolidation — Friday’s strengthening can be viewed as a technical correction within the USD/JPY uptrend, rather than a reversal of that trend. However, should a genuine change occur, the directional move could unfold very rapidly, given that investors have long been accustomed to the JPY’s tactical weakness against the USD.

The Indonesian rupiah hovered near IDR 18,050 per dollar on Friday, remaining under pressure as weak domestic fundamentals outweighed support from a softer greenback. The dollar index extended recent losses after reports that the U.S. and Iran would continue peace negotiations, easing safe-haven demand. Locally, sentiment remained fragile, with May retail sales posting the steepest annual drop in three years as higher non-subsidized fuel prices squeezed spending. Meanwhile, consumer confidence fell for a third straight month in June amid concerns over income, jobs, and future consumption. For the week, the currency was set for a third consecutive decline, down about 0.7% so far, reflecting fears that Indonesia could be downgraded to frontier-market status next year. Still, losses were partly cushioned by stabilizing oil prices, a modest rise in forex reserves, and government measures to bolster food supplies and prepare for El Niño, tempering worries over food inflation.

The US Dollar Index falls for the third straight trading day, extending the decline to near the three-week low at 100.60.

The US signals that it is still committed to the MoU with Iran, and technical talks are still on.

Fed Chair Warsh unveils key members of five task forces.

The US Dollar (USD) extends its losing streak for the third trading day on Friday amid signs of de-escalation in the ongoing clash between the United States (US) and Iran.

In the Asian session, the US Dollar Index (DXY), which tracks the Greenback’s value against six major currencies, trades 0.3% lower to near 100.60, revisiting the three-week low.

US Dollar Price Today

The table below shows the percentage change of US Dollar (USD) against listed major currencies today. US Dollar was the weakest against the Japanese Yen.

USD

EUR

GBP

JPY

CAD

AUD

NZD

CHF

USD

-0.22%

-0.27%

-0.57%

-0.19%

-0.31%

-0.55%

-0.40%

EUR

0.22%

-0.05%

-0.35%

0.05%

-0.12%

-0.34%

-0.18%

GBP

0.27%

0.05%

-0.33%

0.08%

-0.08%

-0.28%

-0.14%

JPY

0.57%

0.35%

0.33%

0.40%

0.27%

0.01%

0.17%

CAD

0.19%

-0.05%

-0.08%

-0.40%

-0.14%

-0.37%

-0.21%

AUD

0.31%

0.12%

0.08%

-0.27%

0.14%

-0.24%

-0.11%

NZD

0.55%

0.34%

0.28%

-0.01%

0.37%

0.24%

0.14%

CHF

0.40%

0.18%

0.14%

-0.17%

0.21%

0.11%

-0.14%

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the US Dollar from the left column and move along the horizontal line to the Japanese Yen, the percentage change displayed in the box will represent USD (base)/JPY (quote).

Earlier in the day, reports from the Times of Israel stated that a US official signaled that Washington is still committed to the memorandum of understanding (MoU) with Iran and technical talks are still on despite US President Donald Trump declaring that the MoU is over and the exchange of attacks between the two.

On Wednesday, US President Trump also said that Iran called for making a deal, but “I just don’t know if they’re worthy of making a deal”, CNBC reported.

Signs of US-Iran war de-escalation diminish the safe-haven appeal of the US Dollar. However, higher oil prices due to renewed energy supply disruption fears have de-anchored inflation projections, which are likely to limit the US Dollar’s downside.

Technically, higher inflation expectations discourage Federal Reserve (Fed) officials from lowering interest rates.

On the monetary policy front, Fed Chair Kevin Warsh has unveiled members of five task forces, as promised in the June policy announcement, which will be focused on communications, the balance sheet policy, improving the quality and timeliness of economic data, productivity and jobs and developing inflation frameworks.

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.