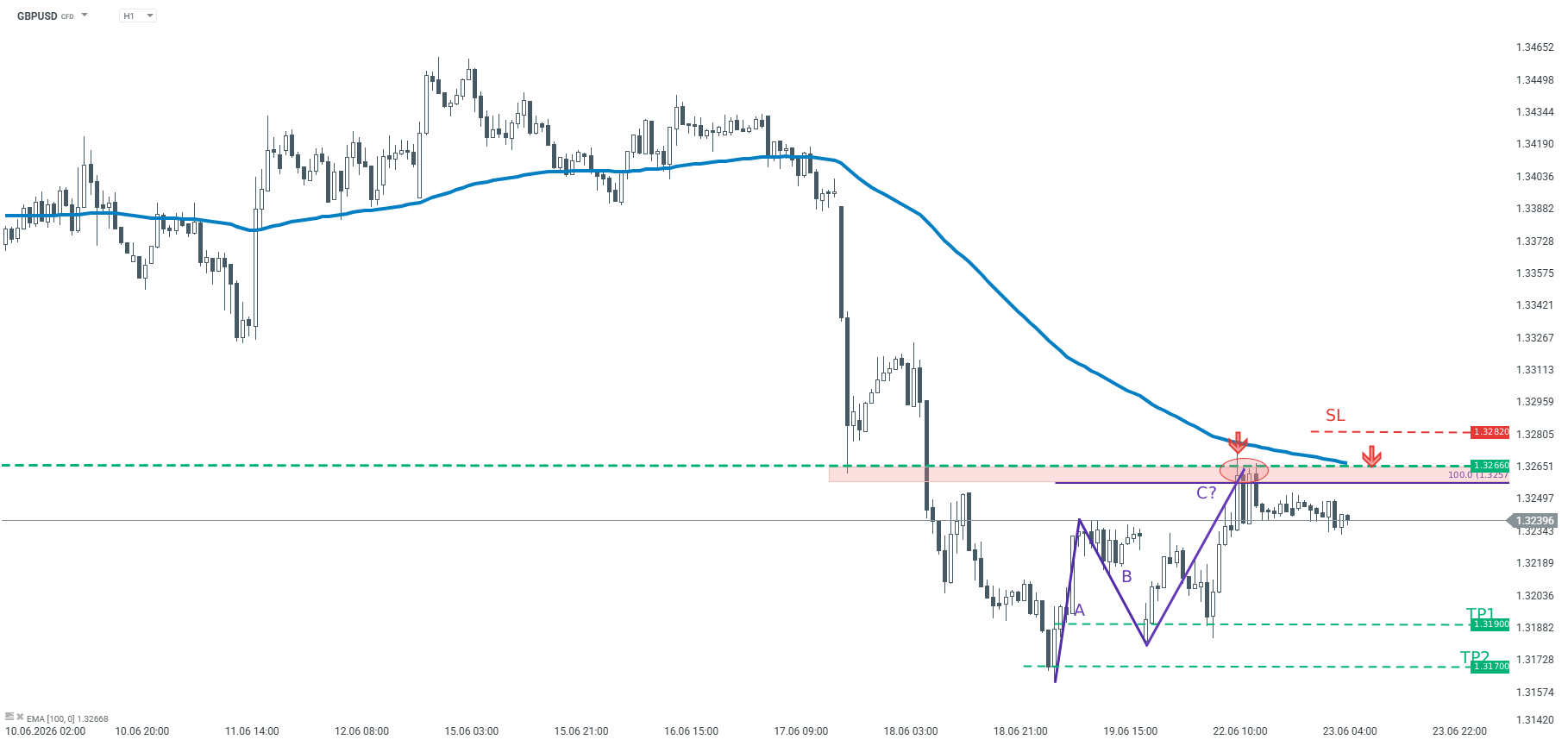

GBPUSD bounced off the resistance area near 1.3260 The pair is trading below 100-period moving average from H1 interval

Recommendation:

Trade: Short position on GBPUSD at market price Target: 1.3190, 1.3170 Stop: 1.3283

Opinion:

GBP/USD has been trading in a downward trend recently. Looking at the H1 interval, we can see that the recent upward correction move was stopped at key resistance. The area near 1.3260 is a result of previous local low, as well as 100.0% Fibonacci Expansion measurement, which means that the A, and B are the same size. According to the Elliot Wawe Theory, it may be the end of the local ABC correction, which supports the downward scenario.

In addition, GBPUSD dropped below 100 – period moving average which further confirms bearish sentiment. We recommend going short GBPUSD at market price with two targets: 1.3190 and 1.3170 We also recommend placing a stop loss at 1.3283.

GBP/USD edges up above 1.3200 as Prime Minister Keir Starmer announces his resignation.

The decision was widely expected with his leadership in question, following a severe defeat in local elections in May.

Andy Burnham, the Mayor of Manchester, emerges as the best-positioned candidate to replace Starmer.

The British Pound (GBP) nudged up above 1.3200 against the US Dollar (USD) on Monday and maintains a mild positive tone, despite news that Sir Keir Starmer resigned as Prime Minister of the United Kingdom and Leader of the Labour Party.

Starmer appeared outside 10 Downing Street earlier on Monday to announce his resignation, adding that he will remain in charge until the party decides on a new leader and pledging support to whoever is the next PM.

The decision was widely expected by the market, as his position as prime minister was seriously called into question after a severe defeat in the local elections in England, Scotland and Wales that delivered a sound victory to Nigel Farage’s Reform UK populist party.

Starmer’s weakness increased last week as the Manchester Mayor, Andy Burnham, the best-positioned Labour leader to replace him, won a seat in parliament, the requirement to become the next prime minister. Later on the day, Burnham is expected to be at Westminster today to be sworn in as MP for Makerfield.

EUR/GBP edges higher to near 0.8670 in Monday’s early European session.

UK PM Starmer was considering his political future after rival Andy Burnham’s decisive election victory in parliament.

UK Retail Sales climbed 3.2% YOY in May, beating expectations.

The EUR/GBP cross gathers strength to around 0.8670 during the early European trading hours on Monday. The British Pound (GBP) weakens against the Euro (EUR) due to political uncertainty in the United Kingdom (UK). European Central Bank (ECB) President Christine Lagarde is scheduled to speak later in the day. The preliminary readings of Purchasing Managers Index (PMI) from Germany, the Eurozone, and the UK will be highlighted later on Tuesday.

UK Prime Minister Sir Keir Starmer is expected to resign to make way for a new leader. It came as cabinet ally Peter Kyle said the UK leader was considering “political realities” after Andy Burnham’s victory in the Makerfield by-election last week cleared a path for him to challenge for the Labour leadership.

“Markets will be focused on Burnham’s views on fiscal policy and whether there will be any relaxation of the current fiscal rules,” said Commonwealth Bank of Australia strategists, including Kristina Clifton. “A loosening in fiscal rules would likely be poorly received by the UK bond market” and weigh on the pound, they said.

Nonetheless, hotter-than-expected UK Retail Sales data might cap the downside for the GBP. UK Retail sales rose 3.2% year-on-year in May, versus 0.1% prior, the Office for National Statistics (ONS) showed on Friday. This figure beat market expectations of a 1.9% annual increase. On a monthly basis, Retail sales increased 1.2% in May, following a revised 1% decline in April.

GBP/USD trades lower to near 1.3220 on renewed UK political uncertainty.

US President Trump says UK PM Starmer could resign on failing to fix immigration and energy issues.

The Fed is expected to deliver at least two interest rate hikes this year.

The GBP/USD pair recovers some of its early losses, but is still 0.1% down to near 1.3220 during the early European trading session on Monday. The pair remains under pressure amid renewed United Kingdom (UK) political uncertainty after comments from United States (US) President Donald Trump that Prime Minister (PM) Keir Starmer could resign on failing to fix immigration and energy issues.

“Keir Starmer will resign as Prime Minister of The United Kingdom. He failed badly on two very important subjects- IMMIGRATION AND ENERGY (OPEN NORTH SEA OIL!). I wish him well!,” US President Trump wrote in a post on Truth Social.

Meanwhile, calls from Labour lawmakers against PM Starmer continuing UK leadership have also accelerated, following Andy Burnham’s strong win in the Makerfield constituency in north-west England.

A Reuters report has shown that UK PM Starmer could decide as early as Monday whether to remain in office and fight a leadership contest or begin the process of stepping down.

Also, an upbeat US Dollar (US) due to increased expectations that the Federal Reserve (Fed) could deliver two interest rate hikes this year is also keeping Cable under pressure. According to the CME FedWatch tool, the odds of the Fed delivering at least two interest rate hikes this year is 58.5%, a sharp increase from 17.1% seen a week ago.

Hawkish Fed bets have strengthened following the first monetary policy announcement on Wednesday under new Chairman Kevin Warsh.

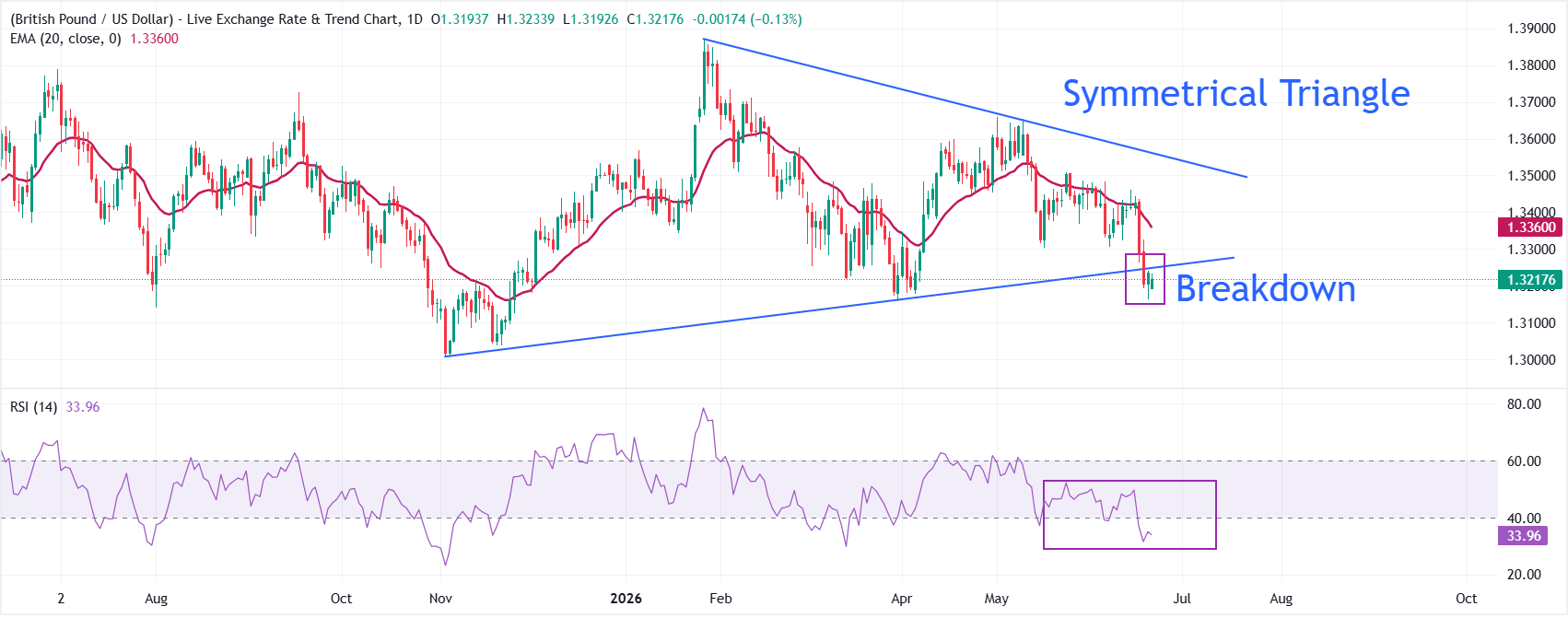

GBP/USD technical analysis

Bias: GBP/USD trades lower at around 1.3218 at press time. The pair maintains a bearish near-term tone as it holds below the 20-period Exponential Moving Average (EMA) at 1.3360. Also, a breakdown of the Symmetrical Triangle strengthens the bearish bias. The Relative Strength Index (RSI) near 34 hovers just above oversold territory, hinting at a dominant downside momentum.

Resistance: On the topside, initial resistance is seen at the broken rising trend-line region near 1.3250, followed by the 20-period EMA at 1.3360.

Support: On the downside, the pair could slide towards the November 25 low at 1.3096 if it resumes its decline below the June 19 low at 1.3163. The pair could extend its decline towards the psychological support at 1.3000 once it falls below 1.3096.

The British pound is regaining momentum at the end of the week, driven by a stronger-than-expected batch of UK economic data.

This surprise surge in retail sales successfully halted sterling’s broad decline against most G10 currencies. Leading the recovery is the GBP/CHF pair, which broke cleanly above key moving averages to cement the pound’s robust positioning across Europe this Friday.

GBPCHF is exhibiting a bullish outlook, rebounding firmly to 1.0651 after finding support near the 38.2% Fibonacci level. The pair trades cleanly above its 10, 30, and 100-day EMAs, saving the upward trend. With the RSI at 56.7, there is plenty of room for further gains toward recent local highs. Source: xStation5

What’s Driving GBPCHF Today?

Sales Surprise on the Upside: Driven by the joint-third warmest May on record and retail promotions, UK retail sales volumes jumped 1.2% in May 2026, bouncing back from a 1.0% decline in April. This growth significantly outperformed economists’ forecasts, with annual sales rising 3.2%. Department and online stores performed particularly well, boosting the online sales share to 28.8%, though overall volumes still remain 0.4% below their pre-pandemic February 2020 levels.

Fragile Trend Sustainability: Over the three months to May 2026, sales volumes edged up 0.4%, supported by strong demand for tech products and outdoor items. However, long-term consumer confidence remains fragile. Shoppers are showing caution regarding big-ticket purchases due to cost-of-living pressures and geopolitical uncertainty surrounding the conflict in Iran. Major supermarket groups like Tesco and Morrisons have already noted a distinct slowdown in sales growth since this conflict began.

Burnham’s Turning Point: Greater Manchester Mayor Andy Burnham’s decisive parliamentary victory in Makerfield has cleared the way for a potential challenge against the deeply unpopular Prime Minister Keir Starmer, threatening fresh political instability in the UK. Positioned as a prime minister-in-waiting and heavily favored by party members, Burnham’s win severely weakens Starmer—who already faces resignation calls from a quarter of his lawmakers—and sets the stage for a high-stakes battle over the future direction of the Labour government.

EUR/GBP retreated to the mid-range of the 0.8600s after rejection at one-month highs near 0.8685.

UK Retail Sales increased well beyond expectations in May.

Public Sector Net Borrowing has also risen against expectations, which might dent the Pound’s recovery.

The Euro (EUR) is pulling back against a stronger British Pound (GBP) on Friday, with the EUR/GBP pair trading at the 0.8665 area following rejection at one-month highs near 0.8685. UK Retail Sales figures released beat expectations in May, but the increase in government borrowing might have offset the positive impact on the GBP.

Retail consumption increased by 1.2% in the UK in May, according to data released by the Office for National Statistics, more than twice the 0.5% expected and following a 1% decline in April. Excluding fuel purchases, sales of all other products also increased by 1.2% after a 0.1% contraction in the previous month.

At the same time, National Statistics also revealed that Public Sector Net Borrowing rose to GBP 23.29 billion in May, from GBP 23.03 billion in April, against expectations of a decline to GBP 18.5 billion. These figures might increase concerns about the UK’s fiscal deficit and dent the Pound’s recovery.

German producer prices slow down in May

In the Eurozone, German Producer Prices Index (PPI) data showed that factory-gate inflation accelerated to 2.2% year-on-year in May, up from 1.7% in April, but below the 2.5% rate expected. The Monthly PPI eased to 0.3% from 1.2% in the previous month.

On Thursday, the Bank of England (BoE) met market expectations and left interest rates on hold at 3.75, with two policymakers calling for a quarter-point rate hike. The central bank also lowered its inflation forecasts for the rest of the year, but warned that the impact of the energy shock on the UK economy remains uncertain.

Also on Thursday, the Labour Mayor of Manchester, Andrew Burnham, won the election in Makerfield, securing the parliamentary seat needed to challenge the Prime Minister, Keir Starmer. The compact on the Pound, however, has been marginal so far.

GBP/USD prolongs its downtrend for the third straight day amid a combination of negative factors.

The UK political turmoil undermines the GBP amid reduced bets for aggressive rate hikes by the BoE.

The Fed’s hawkish tilt and the Iran uncertainty boost the USD, further exerting pressure on the pair.

The GBP/USD pair attracts some follow-through selling for the third straight day and weakens further below the 1.3200 mark, hitting a fresh low since April during the Asian session on Friday. Spot prices remain on track to register heavy weekly losses, and the fundamental backdrop suggests that the path of least resistance remains to the downside.

The British Pound (GBP) continues with its relative underperformance in the wake of lingering domestic political risks, which, along with a bullish US Dollar (USD), validates the near-term negative outlook for the GBP/USD pair. Greater Manchester Mayor Andy Burnham cleared a path to attempt to oust British Prime Minister Keir Starmer after winning a parliamentary seat in northern England on Friday. In his victory speech, Burnham said the result could be a “turning point” for British politics and told his party that this was a final chance to change direction.

Meanwhile, traders have scaled back expectations for more aggressive interest rate hikes by the Bank of England (BoE) following the release of softer inflation figures earlier this week. Furthermore, the US-Iran peace deal eased concerns about the energy shock, endorsing the view that the BoE will hold interest rates steady. This is seen as another factor undermining the GBP. The USD, on the other hand, stands firm near its highest level since late March amid the US Federal Reserve’s (Fed) more hawkish tilt, signaling the possibility of at least one rate hike by the year-end.

On the geopolitical front, US Vice President JD Vance canceled his planned trip for talks with Iran in Switzerland, saying that the meeting wasn’t yet finalized. Adding to this, Israeli air strikes in Lebanon threaten to unravel the US-Iran deal. This further benefits the safe-haven USD and backs the case for an extension of the GBP/USD pair’s steep downfall from the weekly swing high, near the 1.3460 region. This, in turn, suggests that any attempted recovery could be seen as a selling opportunity as traders now look to UK monthly Retail Sales data for a fresh impetus.

Pound Sterling Price This week

The table below shows the percentage change of British Pound (GBP) against listed major currencies this week. British Pound was the strongest against the New Zealand Dollar.

USD

EUR

GBP

JPY

CAD

AUD

NZD

CHF

USD

1.17%

1.70%

0.74%

1.14%

0.66%

1.61%

1.32%

EUR

-1.17%

0.50%

-0.42%

-0.03%

-0.53%

0.43%

0.14%

GBP

-1.70%

-0.50%

-1.09%

-0.52%

-1.03%

-0.07%

-0.35%

JPY

-0.74%

0.42%

1.09%

0.39%

-0.10%

0.89%

0.56%

CAD

-1.14%

0.03%

0.52%

-0.39%

-0.52%

0.50%

0.16%

AUD

-0.66%

0.53%

1.03%

0.10%

0.52%

0.96%

0.69%

NZD

-1.61%

-0.43%

0.07%

-0.89%

-0.50%

-0.96%

-0.28%

CHF

-1.32%

-0.14%

0.35%

-0.56%

-0.16%

-0.69%

0.28%

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the British Pound from the left column and move along the horizontal line to the US Dollar, the percentage change displayed in the box will represent GBP (base)/USD (quote).

The United Kingdom (UK) headline Consumer Price Index (CPI) climbed 2.8% over the year in May, compared to a rise of 2.8% in April, the data released by the Office for National Statistics (ONS) showed on Wednesday. The UK inflation reading was well above the Bank of England’s (BoE) 2% inflation target.

The core CPI (excluding volatile food and energy items) rose 2.6% year-over-year (YoY) in the same period, compared to April’s 2.5% print and came in softer than the forecast of 2.7%.

Meanwhile, the monthly UK CPI arrived at 0.2% in May versus a rise of 0.7% reported in April, below the market consensus of 0.4%.

The British Pound (GBP) attracts some sellers in an immediate reaction to the UK inflation report. At the time of writing, the GBP/USD pair is trading 0.05% lower on the day to trade at 1.3420.

Pound Sterling Price Today

The table below shows the percentage change of British Pound (GBP) against listed major currencies today. British Pound was the weakest against the Swiss Franc.

USD

EUR

GBP

JPY

CAD

AUD

NZD

CHF

USD

-0.04%

0.02%

-0.08%

0.03%

0.12%

0.19%

-0.22%

EUR

0.04%

0.06%

-0.02%

0.06%

0.15%

0.26%

-0.17%

GBP

-0.02%

-0.06%

-0.09%

0.03%

0.13%

0.19%

-0.20%

JPY

0.08%

0.02%

0.09%

0.10%

0.19%

0.22%

-0.10%

CAD

-0.03%

-0.06%

-0.03%

-0.10%

0.09%

0.16%

-0.21%

AUD

-0.12%

-0.15%

-0.13%

-0.19%

-0.09%

0.09%

-0.29%

NZD

-0.19%

-0.26%

-0.19%

-0.22%

-0.16%

-0.09%

-0.38%

CHF

0.22%

0.17%

0.20%

0.10%

0.21%

0.29%

0.38%

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the British Pound from the left column and move along the horizontal line to the US Dollar, the percentage change displayed in the box will represent GBP (base)/USD (quote).

What do United Kingdom CPI inflation data mean for the British Pound?

The UK CPI is a measure of consumer price inflation, the rate at which the prices of goods and services bought by households rise or fall. This figure is one of the most important economic indicators for the GBP because it measures inflation and plays a key role in the Bank of England’s (BoE) monetary policy decisions.

Hotter-than-expected CPI Inflation suggests stronger price pressures in the economy. Traders may expect the BoE to keep interest rates higher-for-longer or consider additional rate hikes.

On the other hand, softer-than-expected outcomes may indicate easing price pressures in the UK economy. Markets could increase their bets on future BoE rate cuts.

Technical Analysis: GBP/USD maintains a neutral outlook in the near-term

In the daily chart, GBP/USD holds just above the Bollinger middle band, while still capped by the 100-day simple moving average (SMA). This configuration suggests a neutral near-term bias, with price consolidating inside the Bollinger envelope rather than trending. The Relative Strength Index (RSI) at roughly 50 hints at balanced momentum, leaving the pair dependent on a break outside this nearby band-and-MA corridor to define the next directional move.

On the topside, initial resistance emerges at the 100-day SMA around 1.3460, with the Bollinger upper band near 1.3498 forming a secondary barrier if buyers extend the recovery. On the downside, immediate support is seen at the Bollinger middle band around 1.3420, ahead of a deeper cushion at the Bollinger lower band close to 1.3345, where a break would expose a broader corrective phase.

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.