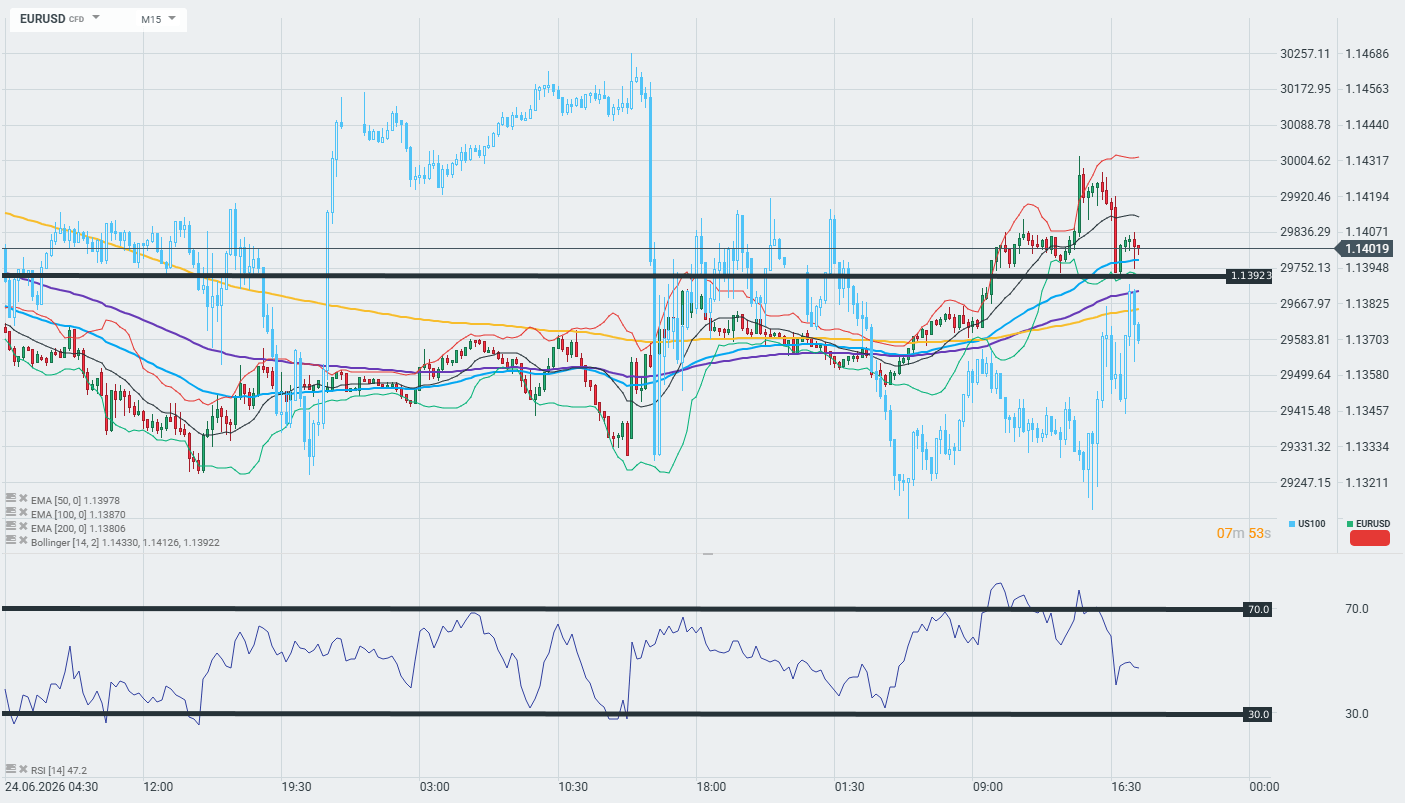

s now losing buying momentum. In the second half of the session, the momentum has clearly shifted to the sellers. The US100, on the other hand, reflects relative strength—the index has gradually lost its downward momentum and is stabilizing in the second half of the day, ignoring some of the negative market signals.

The main topic of the day in the tech world is the potential delay of OpenAI’s IPO — reports in the NYT about the debut being pushed back to next year (in part due to SpaceX’s poor performance following its IPO) have hit the entire semiconductor sector hard. Micron, AMD, and Intel are down about 2% each, while Oracle is down more than 1%. The ripple effect was particularly evident in Asia: SoftBank, a key investor in OpenAI, plummeted by more than 12% , the Nikkei 225 lost 4.15% , and South Korea’s Kospi plunged by 5.81% .

JPMorgan warns outright that the IPO delay “could slow the pace of spending on AI infrastructure.” On the other hand, however, postponing the launch date will keep market expectations alive, which, paradoxically, could have a positive effect on market returns given the narrative being built and the promises of increasingly advanced AI development.

The main risk factor on the geopolitical front, however, is the U.S.-Iran situation. Trump reported on Truth Social that Iran had launched at least four kamikaze drones at ships in the Strait of Hormuz. One struck the deck of a large container ship—the vessel sustained damage but continued its voyage. The other three drones were shot down. Trump called the incident a “stupid violation of the ceasefire agreement.” The Strait of Hormuz is a key route for about 20% of global oil supplies—any escalation in this region immediately catches the attention of commodity markets.

At the same time, Fed’s Kashkari spoke out on inflation—according to him, the labor market is not currently a source of inflation. Price pressures are being driven by the supply side, and one of the factors he mentioned is… the expansion of AI infrastructure. Kashkari of the Fed said that the development of artificial intelligence likely means the Fed will have to raise interest rates.

hursday’s and Friday’s trading sessions saw a sharp rebound in the EUR/USD pair, which is now attempting to consolidate above 1.14 after a series of strong bullish daily candles in recent weeks pushed the dollar to levels not seen since May 2025. Meanwhile, UBS analysts take the opposite view—arguing that the current weakness of the USD is a temporary phenomenon, not a structural one.

UBS vs. the Market — A Discrepancy in Narratives

UBS lowered its forecast for the EUR/USD exchange rate at the end of 2026 to 1.12 from the previous 1.14 , signaling that the bank expects the current trend to reverse. This view is based on a reassessment of U.S. interest rate expectations—the market is beginning to price in the possibility that the Fed may maintain a restrictive monetary policy for longer than previously anticipated. UBS notes that the DXY index has the potential to test the 102 level, which was last seen in May 2025. Although long positions in the dollar have increased, the bank assesses that they are far from the extreme levels seen in 2024—which means there is still room for further USD buying.

Fed vs. ECB — The Divergence Persists

The key driver for the EUR/USD pair remains the divergence in monetary policy on both sides of the Atlantic.

The Fed —despite some market expectations of rate cuts—maintains a hawkish stance, emphasizing the resilience of the U.S. economy and labor market.

The ECB , in turn, is continuing its easing cycle, and further rate cuts are almost fully priced in by the market for the second half of the year. This asymmetry naturally favors the dollar over the euro in the medium term. Today’s rebound in EUR/USD can therefore be interpreted as a technical correction following an extremely rapid move, rather than a change in the pair’s fundamental outlook.

Technical Context and Carry Trade

It is worth noting that, in the same analysis, UBS points to the Swiss franc as a currency that may weaken in the short term due to its growing role as a carry trade funding currency—which indirectly supports risk appetite and may temporarily curb the dollar’s strength. The Australian dollar’s target was lowered to 0.68 from 0.74 , reflecting the global context: weaker macroeconomic data outside the U.S. and narrowing interest rate differentials are boosting the greenback against commodity and emerging-market currencies.

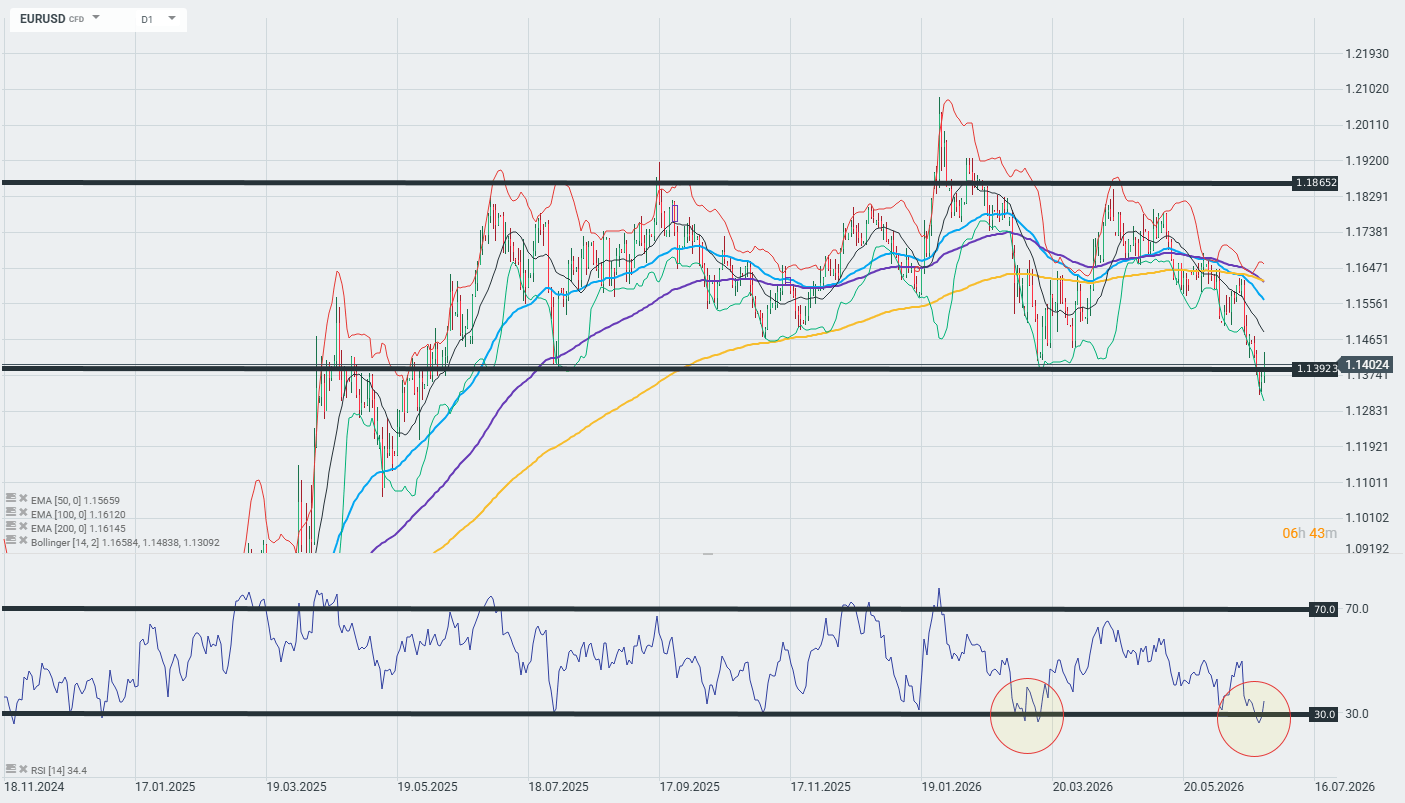

Technical Analysis: EURUSD D1

The pair is currently testing a key level at 1.1392—a break below or above this level could determine the pair’s trajectory for the coming sessions. On the upside, resistance comes from the 50/100/200 EMAs clustered around 1.1560–1.1615. The RSI, at 34.4, is approaching the oversold zone (30)—similar to February 2026—which could trigger a short-term technical rebound. Nevertheless, as long as the pair does not close the day clearly above 1.1392, technical analysis favors a continuation of the downtrend. It is worth noting, however, that the pair has been highly volatile in recent days, so price movements may remain chaotic in the near term.

The GBP/USD rate is rebounding slightly as the dollar (specifically the dollar index, USDIDX) corrects across the broader market after breaking out to a 13-month high. Technically, however, we are far from breaking the downward trend on GBPUSD. Even after the recent bounce, the price has been moving below the 10-day exponential moving average (EMA10; yellow) for 9 days. Furthermore, the cascade of the remaining EMAs (longer over shorter: EMA100 over EMA30, and EMA30 over EMA10) signals a clear downtrend, the reversal of which would require a series of bullish turnarounds. The chances of a strictly pro-pound turnaround remain slim. The British currency is primarily weighed down by a period of political uncertainty and the ongoing leadership transition within the ruling Labour Party following Prime Minister Starmer’s resignation.

The Guardian reported that according to preliminary internal party plans, Burnham could assume the office of Prime Minister as early as July 17. However, the anticipation—especially regarding the appointments of key cabinet members such as the Chancellor—should continue to test the pound. On the dollar side, we see a persistently hawkish Fed narrative, an increase in core PCE inflation to 3.4%, and a Q1 2026 GDP revision from 1.6% to 2.1%. The backdrop of a gathering momentum in the US economy alongside elevated inflation contrasts sharply with stagflationary tendencies in the UK. This divergence should extend the current trend on GBPUSD and the UK/US 10-year bond yield spread, until potential wage effects emerge from the recent UK energy shock, which could force the Bank of England into a more hawkish monetary policy stance. However, UK policy is already restrictive, which limits the potential for a sharp pivot.

Methodology

This recommendation was prepared based on a technical analysis of the GBPUSD chart and a fundamental analysis of the economies in question (monetary policy in the United Kingdom and the United States). The directional bias of the recommendation was determined using moving averages and market expectations regarding central bank policies. Take Profit and Stop Loss levels were established using Fibonacci retracements and price action:

TP1 and TP2 are located at the nearest support levels from November 2025.

SL is placed halfway between the EMA10 and EMA30, as well as between the 23.6% and 38.2% Fibo levels.

GBP/USD attracts some buyers for the second straight day amid a mildly softer US Dollar.

The UK political crisis holds back GBP bulls from placing fresh bets and caps spot prices.

The bearish technical setup suggests that a further move up is more likely to be sold into.

The GBP/USD pair sticks to its positive bias for the second straight day, though it lacks bullish conviction and trades just above the 1.3200 mark during the early European session on Friday. The US Dollar (USD) remains depressed below its highest level since May 2025, touched on Thursday, and acts as a tailwind for spot prices.

However, the UK political crisis holds back traders from placing aggressive bullish bets around the British Pound (GBP) and caps the upside for the GBP/USD pair. Furthermore, a bearish technical setup warrants caution before positioning for any meaningful recovery from the 1.3140 area, or the lowest since November, set on Wednesday.

Against the backdrop of the recent repeated failures near the 200-period Simple Moving Average (SMA) on the 4-hour chart, this week’s break below the 1.3300 mark was seen as a key trigger for the GBP/USD bears. Moreover, the Relative Strength Index (RSI) is at 47, suggesting consolidative conditions rather than clear trend strength.

However, the Moving Average Convergence Divergence (MACD) indicator shows the MACD line modestly above the signal line and hovering around zero. This hints at tentative bullish momentum that is not yet strong enough to challenge the GBP/USD pair’s dominant downtrend witnessed over the past two months or so.

On the topside, initial resistance is located at the 200-period SMA at 1.3384, and spot prices would need a sustained break above this level to ease the broader bearish bias and open the way for a more constructive recovery phase. On the downside, intraday setbacks are likely to be driven more by price action than by clearly defined structural supports.

Meanwhile, traders will be watching the recent lows around the mid-1.3100s as a provisional near-term floor for the GBP/USD pair until fresh technical levels emerge.

(The technical analysis of this story was written with the help of an AI tool.)

GBP/USD 4-hour chart

US Dollar Price Today

The table below shows the percentage change of US Dollar (USD) against listed major currencies today. US Dollar was the strongest against the Australian Dollar.

USD

EUR

GBP

JPY

CAD

AUD

NZD

CHF

USD

-0.14%

-0.07%

-0.10%

-0.04%

0.29%

0.04%

-0.22%

EUR

0.14%

0.07%

0.06%

0.13%

0.44%

0.16%

-0.07%

GBP

0.07%

-0.07%

0.00%

0.06%

0.38%

0.12%

-0.13%

JPY

0.10%

-0.06%

0.00%

0.06%

0.39%

0.11%

-0.12%

CAD

0.04%

-0.13%

-0.06%

-0.06%

0.33%

0.05%

-0.20%

AUD

-0.29%

-0.44%

-0.38%

-0.39%

-0.33%

-0.26%

-0.52%

NZD

-0.04%

-0.16%

-0.12%

-0.11%

-0.05%

0.26%

-0.24%

CHF

0.22%

0.07%

0.13%

0.12%

0.20%

0.52%

0.24%

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the US Dollar from the left column and move along the horizontal line to the Japanese Yen, the percentage change displayed in the box will represent USD (base)/JPY (quote).

EUR/USD struggles to lure buyers on Friday as Hormuz risks support the safe-haven USD.

Receding Fed rate hike bets keep a lid on the USD appreciation and limit losses for the pair.

The bearish technical setup suggests that the path of least resistance is to the downside.

The EUR/USD pair struggles to capitalize on the previous day’s modest recovery gains and oscillates in a narrow band during the Asian session on Friday. Spot prices, however, hold above mid-1.1300s and the lowest level since May 2025, set on Thursday, warranting some caution for bearish traders.

Reports that Iran’s Islamic Revolutionary Guard Corps (IRGC) attacked a Singapore-flagged cargo ship in the Strait of Hormuz reignite worries about the sustainability of an interim US-Iran peace deal and support the safe-haven US Dollar (USD). This, in turn, is seen as a key factor acting as a headwind for the EUR/USD pair.

Meanwhile, traders trimmed their bets for interest rate hikes by the US Federal Reserve (Fed) this year amid expectations that inflation likely peaked last month or is close to doing so in the face of the recent fall in Crude Oil prices. This caps the upside for the USD and helps limit any further downside for the EUR/USD pair.

The recent repeated failures to find acceptance above the 100-period Simple Moving Average (SMA) on the 4-hour chart and the EUR/USD pair’s inability to gain any meaningful traction favor bears. Moreover, the Relative Strength Index (RSI) near 42 hints at a gradual recovery from oversold conditions rather than a bullish shift.

Meanwhile, the Moving Average Convergence Divergence (MACD) has now turned modestly positive, though the EUR/USD pair remains structurally pressured in the near-term. This, in turn, suggests that any meaningful recovery attempt might still be seen as a selling opportunity and runs the risk of fizzling out rather quickly.

Immediate resistance is located at the 1.1440 region, and a break above could lift the EUR/USD pair back to the 100-period SMA at 1.1514. A move beyond this hurdle is needed to ease the current bearish tone and open the way for a more meaningful correction higher. Until then, the pair seems vulnerable to test fresh lows.

(The technical analysis of this story was written with the help of an AI tool.)

EUR/USD 4-hour chart

US Dollar Price Today

The table below shows the percentage change of US Dollar (USD) against listed major currencies today. US Dollar was the strongest against the Australian Dollar.

USD

EUR

GBP

JPY

CAD

AUD

NZD

CHF

USD

-0.02%

-0.05%

-0.10%

-0.06%

0.25%

0.14%

-0.08%

EUR

0.02%

-0.05%

-0.06%

-0.02%

0.27%

0.12%

-0.06%

GBP

0.05%

0.05%

0.00%

0.00%

0.32%

0.19%

-0.02%

JPY

0.10%

0.06%

0.00%

0.02%

0.33%

0.19%

-0.01%

CAD

0.06%

0.02%

0.00%

-0.02%

0.31%

0.16%

-0.05%

AUD

-0.25%

-0.27%

-0.32%

-0.33%

-0.31%

-0.13%

-0.35%

NZD

-0.14%

-0.12%

-0.19%

-0.19%

-0.16%

0.13%

-0.20%

CHF

0.08%

0.06%

0.02%

0.00%

0.05%

0.35%

0.20%

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the US Dollar from the left column and move along the horizontal line to the Japanese Yen, the percentage change displayed in the box will represent USD (base)/JPY (quote).

EUR/JPY is bearish, trading below its nine-period and 50-period EMAs.

The 14-day Relative Strength Index at 38 signals continuing downside momentum, not an oversold reversal.

Spot above 183.81 VWAP means buyers control the EUR/JPY cross in intraday trading.

EUR/JPY inches lower after registering minor gains in the previous day, trading around 183.90 during the Asian hours on Friday. The currency cross maintains a bearish near-term bias as it holds below both the nine-period and 50-period Exponential Moving Averages (EMAs) at 184.38 and 184.91, respectively.

The EUR/JPY cross is remaining within the symmetrical triangle, suggesting market indecision and an impending breakout as energy builds, while the 14-day Relative Strength Index (RSI) has eased toward 38, hinting at lingering downside pressure rather than a decisive oversold reversal.

However, the session Volume-Weighted Average Price (VWAP) represents the true average price paid for a stock or asset throughout the day, weighted by volume. Because the spot price is higher than the VWAP of 183.81, it means buyers are firmly in control and are willing to pay a premium to acquire the EUR/JPY cross.

In context with the symmetrical triangle, volatility is shrinking. Think of it like a compressed spring; the market is resting and storing energy for a major breakout. Because the price is trapped between two converging trendlines, momentum indicators like VWAP lose their directional edge until a breakout occurs.

The initial support is aligned at the lower boundary of the symmetrical triangle around 183.40. Further declines would expose the four-month low of 181.87, recorded on March 16, followed by the six-month low of 180.81.

On the upside, primary resistance is seen at the nine-period EMA at 184.38, followed by the 50-period EMA at 184.91; a sustained break above these levels would soften the bearish tone and expose the upper boundary of the symmetrical triangle around 186.00. Further advances would support the EUR/JPY cross to test the all-time high of 187.95.

EUR/JPY: Daily Chart

Euro Price Today

The table below shows the percentage change of Euro (EUR) against listed major currencies today. Euro was the weakest against the Swiss Franc.

USD

EUR

GBP

JPY

CAD

AUD

NZD

CHF

USD

-0.03%

-0.05%

-0.11%

-0.06%

0.33%

0.14%

-0.17%

EUR

0.03%

-0.03%

-0.06%

-0.01%

0.36%

0.14%

-0.13%

GBP

0.05%

0.03%

-0.04%

-0.01%

0.39%

0.19%

-0.11%

JPY

0.11%

0.06%

0.04%

0.05%

0.43%

0.22%

-0.06%

CAD

0.06%

0.00%

0.00%

-0.05%

0.39%

0.16%

-0.13%

AUD

-0.33%

-0.36%

-0.39%

-0.43%

-0.39%

-0.20%

-0.48%

NZD

-0.14%

-0.14%

-0.19%

-0.22%

-0.16%

0.20%

-0.29%

CHF

0.17%

0.13%

0.11%

0.06%

0.13%

0.48%

0.29%

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the Euro from the left column and move along the horizontal line to the US Dollar, the percentage change displayed in the box will represent EUR (base)/USD (quote).

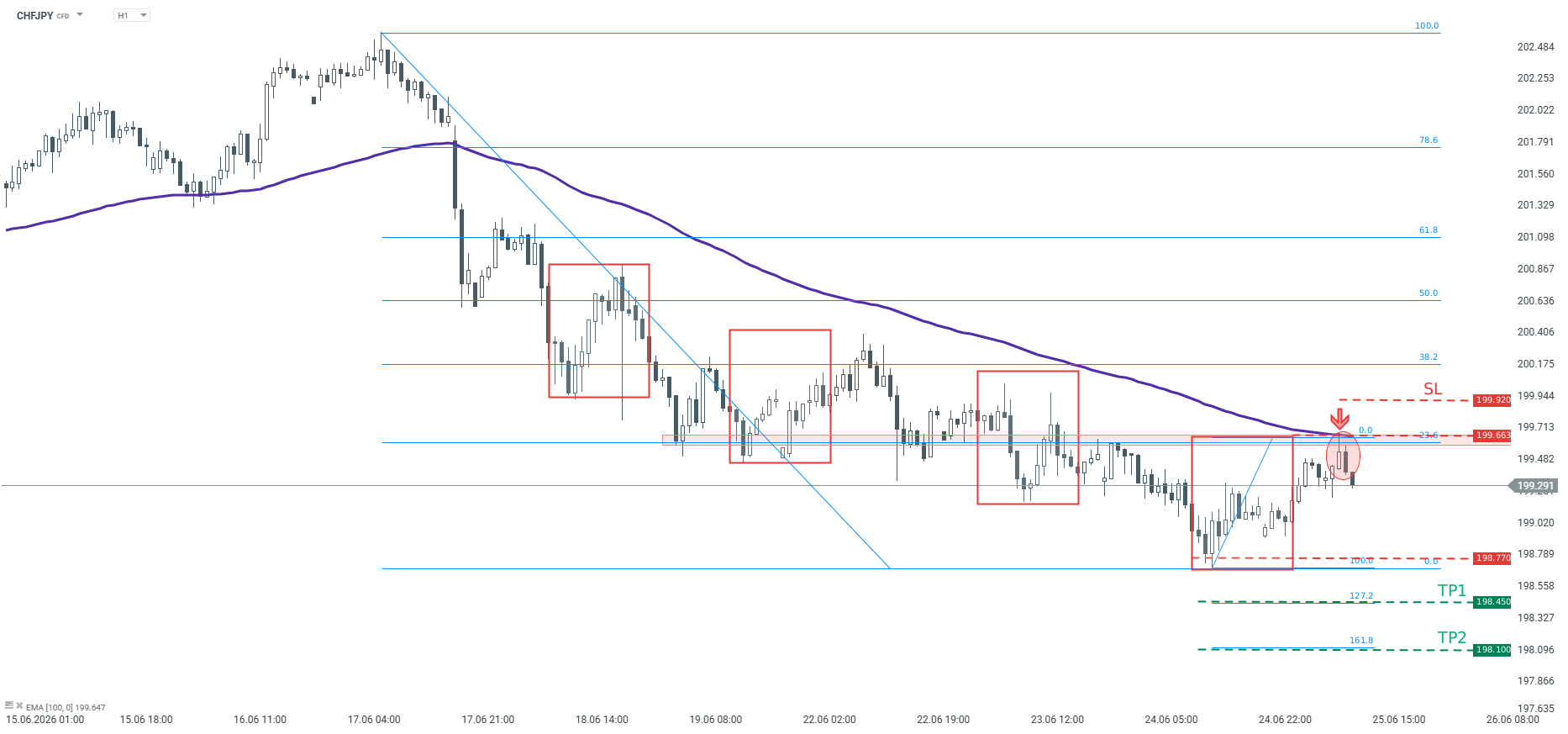

CHFJPY reversed from the key resistance level at 199.66

The pair has been trading in a downtrend since June 17

Trade RecommendationTrade:

Open a short position on CHFJPY at the current market price.

Target 1: 198.45

Target 2: 198.10

Stop Loss: 199.92

Analysis

CHFJPY has remained in a downtrend in recent sessions. On the H1 chart , the pair staged a local bullish correction, but buyers failed to break above the key 199.66 resistance , which is defined by the upper boundary of the 1:1 Overbalance structure and the 100-period moving average . According to the Overbalance methodology , as long as the price remains below this resistance level, the prevailing market sentiment stays bearish. With this in mind, further downside in CHFJPY appears likely. We recommend opening a short position at the current market price, targeting 198.45 and 198.10 , with a stop loss at 199.92 .

n labour market proved more resilient than expected, with the unemployment rate falling to 4.4% from a five-year high of 4.5% , while employment increased by 40.3k , comfortably beating expectations for a gain of around 30k . At the same time, household spending surprised to the upside, rising 1.3% in May versus market expectations of just 0.5% . For investors, the key takeaway is that the combination of a strong labour market, resilient consumers and still-elevated inflation complicates the case for an early policy easing by the Reserve Bank of Australia (RBA). Money markets continue to price roughly an 80% probability that the RBA will leave interest rates unchanged in August , but the latest data has strengthened the arguments in favour of another rate hike. For the Australian dollar, this provides potential support from a relatively hawkish central bank, although the medium-term direction of the AUD will depend on upcoming inflation and labour market data.

Labour market: Headline numbers beat expectations

The latest figures from the Australian Bureau of Statistics (ABS) showed that the unemployment rate declined to 4.4% , after previously rising to 4.5% , its highest level in five years. This was an important surprise, as economists had expected unemployment to remain unchanged at 4.5%. Employment increased by 40.3k , significantly outperforming market forecasts. At the same time, around 18.3k people lost their jobs, leaving the overall balance of the labour market firmly positive. The ABS also noted that the backlog of people waiting to start new jobs eased during May, helping boost employment and reduce unemployment. One weaker aspect of the report was a 1.1% decline in hours worked . According to the ABS, this was largely due to Australians catching up on leave that had not been taken during April. At first glance, the report appears very strong: unemployment is falling, employment is rising, and consumers are spending more. These are typically supportive conditions for both the Australian dollar and government bond yields. However, the decline in hours worked and sluggish employment growth over recent quarters suggest the labour market may not be as strong beneath the surface as the headline figures imply. The economy could be approaching a turning point, but it has not reached one yet. For the RBA, the latest data still do not provide sufficient evidence that economic conditions are cooling sustainably.

RBA faces a difficult balancing act

The Reserve Bank of Australia has a dual mandate: maintaining inflation within its 2–3% target range while supporting full employment. The latest economic releases suggest that the Australian economy remains too resilient for the central bank to comfortably shift toward a more dovish stance. The next set of inflation and labour market data for June will therefore be crucial, as it will represent the final major batch of macroeconomic information before the RBA’s August policy meeting. The RBA recently left its cash rate unchanged at 4.35% , following three consecutive 25-basis-point rate hikes in 2026. Since the beginning of the year, the official cash rate has increased from 3.60% to 4.35% . For financial markets, the August meeting remains finely balanced. Money markets still assign roughly an 80% probability to a pause , but stronger employment data and the rebound in household spending make such a decision less straightforward.

Inflation remains the key risk

Australia’s headline CPI inflation eased to 4.0% YoY in May , down from 4.2% in April. At first glance, this appears to be encouraging news for the RBA. However, much of the improvement was driven by the Australian government’s temporary reduction in fuel excise taxes. Automotive fuel prices declined 11.9% in May , following a 7.0% decline in April. More importantly, the trimmed mean inflation rate —the RBA’s preferred measure of underlying inflation—rose to 3.6% from 3.4% , indicating that underlying price pressures remain persistent after excluding the most volatile components. For traders, this is the critical part of the inflation story. Unless core inflation begins to decline more convincingly, the RBA may have little choice but to maintain its hawkish rhetoric or even consider another rate increase.

Household spending rebounds

Another important feature of the latest data release was the 1.3% increase in household spending during May . This marked a sharp recovery following declines of 1.1% in April and 1.7% in March . The figure significantly exceeded expectations of a 0.5% increase , suggesting Australian consumers remain surprisingly resilient despite elevated living costs, higher energy bills and rising mortgage repayments. Part of the increase reflected the normalisation of airline ticket refunds following disruptions related to the Middle East conflict. Nevertheless, the broader picture remains unchanged: household spending has yet to show signs of a meaningful slowdown. For the RBA, this creates another challenge. A resilient labour market continues to support household incomes, helping sustain consumption and making it more difficult to return inflation to target.

Mortgage holders remain under pressure

Since the beginning of 2026, the RBA’s cash rate has increased from 3.60% to 4.35% . Three consecutive quarter-point rate hikes have added approximately AUD 342 to the average monthly repayment on a typical AUD 736,000 mortgage. On an annual basis, this translates into roughly AUD 4,128 in additional borrowing costs. Should the RBA deliver a fourth rate increase, Compare the Market estimates average monthly repayments would rise by a further AUD 114 . Combined with the previous hikes, annual mortgage servicing costs would increase by around AUD 5,472 . This is particularly important for investors because household finances remain one of the key transmission channels of monetary policy in Australia. The paradox is that despite mounting pressure on borrowers, consumer spending has yet to weaken materially. This increases the likelihood that the RBA continues to view the economy as too resilient.

Labour shortages remain widespread

Despite record migration levels, Australian businesses continue to report significant labour shortages. According to ABS data, job vacancies remain 45% above pre-pandemic levels and have stayed above 325,000 vacancies for five consecutive years. The most acute shortages remain in healthcare and social assistance , where vacancies are 90% higher than before the pandemic. Manufacturing vacancies are 78% higher , electricity, gas, water and waste services are 76% above pre-pandemic levels, while mining vacancies remain 58% higher . This matters because persistent labour shortages tend to keep wage pressures elevated. As long as businesses continue competing for workers, wage inflation could remain stronger than desired even if overall economic growth slows. For the RBA, this means the labour market may stay too tight for underlying inflation to return quickly to target. For investors, it raises the probability that monetary policy will remain restrictive for longer.

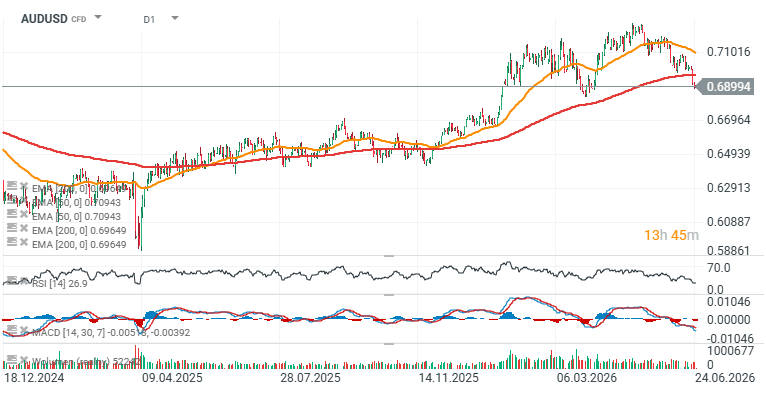

Implications for the Australian dollar – AUD/USD chart

The latest labour market report is broadly supportive for the Australian dollar because it reinforces the case for higher interest rates for longer. Stronger employment, lower unemployment and resilient consumer spending all reduce the scope for the RBA to pivot toward easier monetary policy. For currency pairs such as AUD/USD , AUD/JPY and EUR/AUD , the key question is whether markets begin shifting expectations from a rate pause toward another hike. If rate hike probabilities continue to increase, the Australian dollar could receive additional support through the interest rate channel. At the same time, the Australian dollar remains highly sensitive to global risk sentiment, commodity prices and developments in China. Consequently, stronger domestic macroeconomic data alone may not be sufficient to generate a sustained uptrend if global conditions become less supportive for cyclical currencies. The main conclusion for investors is straightforward: the latest labour market report has reduced expectations of an early dovish shift by the RBA while significantly increasing the importance of the next inflation release.

Looking at the AUD/USD chart, the pair has fallen below the 200-period EMA (red line), which has generally acted as a springboard for rebounds since April 2025. The key question now is whether this latest decline marks the beginning of a more durable trend reversal or simply a deeper correction similar to previous pullbacks. The nearest major support is located around 0.67 , corresponding to the March swing lows, while the 200-period EMA near 0.70 now represents the primary resistance level.

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.